This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is where PCIDSS (Payment Card Industry Data Security Standard) compliance becomes essential for Australian businesses. In todays article, we are going to learn how PCIDSScompliance protects businesses from data breaches. The latest version PCIDSS v.4.0

That’s where PCIDSS, PSDS2, and AML come in. These compliance standards aren’t just check boxes; they are tools that protect your business and build confidence. Most importantly, you’ll see how the right digital payment solution can make compliance simpler and more effective. What is PCIDSS?

The Payment Card Industry Data Security Standard (PCI-DSS) is a set of global standards developed to safeguard cardholder data. Compliance ensures robust security practices to prevent breaches and protect sensitive payment card data. Staying up-to-date with PCI-DSScompliance should be a top priority.

Here is a link to the PCI official Quick Reference though be warned its still 38 pages long. Many businesses find PCIcompliance confusing and frustrating, and there are times when it feels like you need a degree in cybersecurity just to understand what the standard wants you to do. What is PCI again?

Organization that are certified by CREST goes thorough assessments of their methodologies, quality assurance processes, and data security measures, offering assurance to clients seeking reliable and trustworthy security services.

The merchant underwriting process is a critical step that payment processors and financial institutions use to assess the risk associated with onboarding new businesses. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

Companies can analyze BIN data to track transaction patterns, better understand customer demographics, and assess risk in different regions or among various card types. This information helps payment processors and merchants verify transactions, assess risk, and streamline payment workflows for secure and reliable transactions.

Ensure the gateway offers PCIDSScompliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. Security and compliance Receiving online payments makes your business an easy target for fraudsters and cybercriminals. Learn More What is a Payment Gateway?

But many business owners find PCIcompliance and SAQs confusing or overwhelming. The Self-Assessment Questionnaire (SAQ) is a series of yes or no questions about your security practices. The Self-Assessment Questionnaire (SAQ) is a series of yes or no questions about your security practices. What is the SAQ?

Interchange and assessment fees are set by card networks and are non-negotiable. Assessment fees Assessment fees go to the payment network or the credit card network. In the previous example, Mastercard retains the assessment fee from the overall credit card processing fee. This helps the processor recoup lost revenue.

It also ensures that data security best practices, particularly PCIDSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data. You must also be able to adapt the platform for automated compliance with regulations in your specific industry.

To choose the right solution, you need to look at various factors when evaluating potential providers, including supported payment types, transaction fees and pricing structures, payout speed, and PCIDSScompliance. Its also not an option to have them; you must ensure PCIcompliance.

This tokenization keeps the sensitive card information off your servers, reducing the risk of a data breach and easing PCIDSScompliance. Ensure High-Level Security and Compliance Payment data breaches destroy customer trust and can bankrupt small businesses. Never sign up without seeing a complete fee schedule.

When implementing a surcharging program, businesses follow local regulations, ensure legal compliance, determine surcharge percentages and communicate transparently. Assessment fees: Assessment fees are charges imposed by the card brands themselves. Compliance with legal regulations and card network guidelines is necessary.

In addition to the usual concerns around security and compliance, there’s also the issue of user experience. Features to Look for With Your Mobile Payment Gateway Integrations Assessing the features of prospective payment gateways for your mobile app will help you determine which payment gateway meets your needs.

These fees typically include interchange fees, which go to the card-issuing bank, assessment fees charged by the card networks, and payment processor fees for handling the transaction. The total cost varies based on factors like the type of card used, the transaction method, and the merchants industry.

Encryption and transfer of payment information The payment gateway that underpins your checkout page will now encrypt the customers payment details as stipulated by industry data security regulations like PCIDSS (Payment Card Industry Data Security Standard) before transferring the data to your payment processor.

Increased security and compliance: Reputable Salesforce payment integrations are designed with strong security protocols and compliance with Payment Card Industry Data Security Standards (PCIDSS). Continuous assessments of your payment integrations are necessary to ensure they run to their fullest capacity.

However, rapid growth brings challenges including scaling operations, ensuring regulatory compliance and maintaining robust IT infrastructure. These facilities offer flexible, scalable solutions with high availability, security and built-in regulatory compliance, eliminating the burden of managing an entire data centre.

To properly evaluate payment gateway providers, merchants should conduct thorough research, participate in demos and trials, assess vendor reputation, and review customer support options for each. During this time, you can assess the gateways features, user interface, and security measures.

An outsourced integrated payments support team could also assist business software users with their unique issues or questions about security and compliance. Outsourcing payment support can save costs, provide 24/7 assistance, and ensure compliance expertise.

Fraud detection and risk assessment: MCCs assist fraud detection and risk assessment operations by flagging suspicious transactions. Tax reporting and compliance: MCCs aid in tax reporting and compliance with regulatory bodies like Payment Card Industry Data Security Standards (PCIDSS) and Anti-Money Laundering (AML).

PCIcompliance and security Integrated payment gateways typically come with built-in security features such as full compliance with Payment Card Industry Data Security Standards (PCIDSS) , tokenization, and encrypted data transmission.

Understanding these differences is essential for addressing common challenges, such as manual errors, delayed invoices, and poor payment tracking, as they can strain customer relationships, limit payment flexibility, and lead to compliance issues.

Keep an eye out for hidden fees that may not be immediately apparent, like setup fees, monthly maintenance fees, PCIcompliance fees, or chargeback fees. This hands-on experience allows you to explore the platform’s interface, understand its features, and assess its compatibility with your business systems and daily operations.

They’re ideal for messy, unpredictable problems, like assessing complex customer interactions or navigating multi-system processes. For the middle office and compliance, agents will read reports (e.g.SAR or STR), alert, monitor, score, build graphs, assess counterparties, write reports, etc.

This is where the Payment Card Industry Data Security Standard (PCIDSS) comes into play, serving as a crucial framework for safeguarding sensitive information and protecting both businesses and consumers from the ever-present threat of cybercrime. This assessment will help determine the scope of the compliance efforts.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

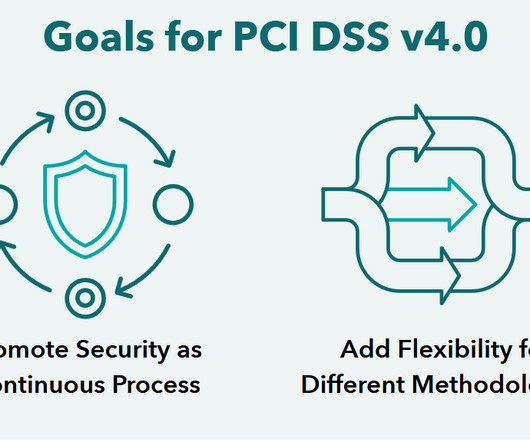

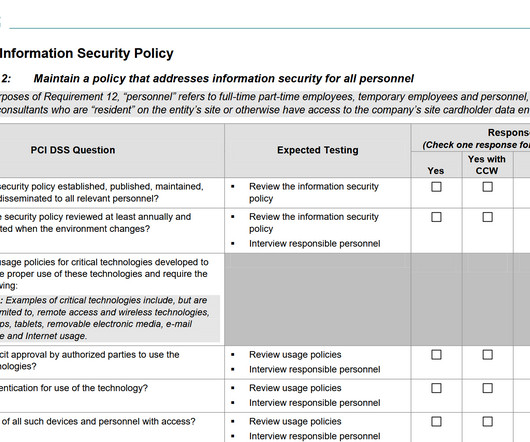

The Payment Card Industry Data Security Standard (PCIDSS) compliance 4.0 In this blog, we will understand PCIDSScompliance 4.0 What is PCIDSSCompliance for banks? What is PCIDSSCompliance for banks? The PCIDSS outlines 12 requirements mentioned below.

In this blog post, we’ll delve into the significance of PCIDSScompliance in healthcare and explore how it helps protect patient data and privacy. You may be wondering, what is the role of PCIDSS in healthcare if an organization is already HIPAA compliant? What is PCIDSS in the Healthcare Industry?

While Type 1 assesses the design of controls at a specific point in time, Type 2 evaluates the effectiveness of these controls over a period, usually upto twelve months. It must be noted that Vi was first received its SOC2 Type 1 attestation in 2022, which was also done by VISTA InfoSec.

The Payment Card Industry Data Security Standard (PCIDSS) is no exception. With the recent release of PCIDSS v4.0, Changes in Requirement 9 of PCIDSS v3.2.1 to PCIDSS v4.0: Requirement V.3.2.1(9.1) PCIDSS v4.0 PCIDSS v4.0 PCIDSS v4.0

The PCIDSS Checklist is a crucial first step in securing your business. It’s a tool that helps businesses ensure they’re meeting all the requirements of the Payment Card Industry Data Security Standard (PCIDSS). To get started on your journey towards PCIDSScompliance, we recommend visiting the PCIDSS v4.0

Requirement 10 of the PCIDSS covers logging and monitoring controls that allow organizations to detect unauthorized access attempts and track user activities. In the newly released PCIDSS 4.0, to PCIDSS 4.0. Whether you’re currently compliant under PCIDSS v3.2.1 In PCIDSS v4.0,

Welcome back to our ongoing series on the Payment Card Industry Data Security Standard (PCIDSS) requirements. This requirement is a critical component of the PCIDSS that has undergone significant changes from version 3.2.1 Conclusion: The transition from PCIDSS v3.2.1 to the latest version 4.0.

In our ongoing series of articles on the Payment Card Industry Data Security Standard (PCIDSS), we’ve been examining each requirement in detail. In this blog post, we will delve into the changes introduced in PCIDSS Requirement 8 from version 3.2.1 Conclusion: PCIDSS v4.0 password and token).

This is why PCIDSScompliance is critical. Compliance with PCI Data Security Standard regulations prevents shortcomings and vulnerabilities in payment processing, thereby reducing the risk of fraud, identity theft, and cyberattacks. The 12 PCIDSS requirements are meant to help companies achieve six main goals.

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0 c: Confirm that software applications comply with PCIDSS. - c: Confirm that software applications comply with PCIDSS. - In PCIDSS v4.0, In PCIDSS v4.0,

As director/MLRO of SENDS, a UK-licensed EMI, I see AI’s potential in fraud prevention, AML, and compliance. Sends leverages AI to mitigate risks, comply with FCA, PSD2, and PCIDSS, and enhance client experience with secure and innovative services.

The Payment Card Industry Data Security Standard ( PCIDSS ) aims to prevent financial fraud by securing payment card data. In this process, you’ll come across key terms like PCI SAQ (Self-Assessment Questionnaire), AOC (Attestation of Compliance), and PCI ROC (Report on Compliance).

In the world of digital transactions, businesses handling payment cards must demonstrate their data security measures through the Payment Card Industry Self-Assessment Questionnaire (PCI SAQ). Completing the SAQ is a key step in the PCIDSSassessment process, followed by an Attestation of Compliance (AoC) to confirm accuracy.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content