This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing creditrisk. This vital task is complicated even in normal times due to the multitude of financial risk factors in play at any given time. percent employ it for credit underwriting.

Bloomberg customers will now be able to use the news site's terminal to look at Credit Benchmark 's creditrisk data, which comes from risk views of the world's largest financial institutions, according to a press release. They can also assess ongoing credit quality.

Which works better for modeling creditrisk: traditional scorecards or artificial intelligence and machine learning? Take, for example, our new credit decisioning solution, FICO Origination Manager Essentials – Small Business. It’s designed to help lenders make faster origination decisions without increasing risk.

Sovcombank, a universal bank with more than 2 million customers, is using the score to “gamify” the credit application process. The EFL creditrisk score is created through a dynamic behavioral design and psychometric assessment that analyzes character traits with a proven relationship to creditrisk.

Today in B2B, Bloomberg broadens its creditrisk data pool, and two ERP solutions secure B2B payments integrations. Bloomberg To Incorporate CreditRisk Data. The release stated firms have more often been looking for data to validate their own internal counterparty and creditriskassessment.

Lenders rely on credit scoring to assess consumers’ risk, and credit scoring relies on credit data. But what if an applicant is new to credit? EFL offers financial institutions a different way to assess creditworthiness and promote financial inclusion: by understanding personality.

Managing creditrisk used to be a reactive process. Waiting until account holders fall behind to take action not only meant that customers’ credit scores would take a hit before their banks were alerted to a problem, but also that banks would lose the revenue from the scheduled payment.

British FinTech, Lemon, which specialises in SaaS finance for SMB’s has announced a strategic partnership with WiserFunding, a leader in alternative data for creditriskassessment.

In fintech, Agentic AI could enhance fraud prevention, risk management, trading, and customer engagement by autonomously analysing financial data, detecting anomalies, and executing decisions in real time. Theres a risk that AI could inadvertently expose data through cyberattacks, algorithmic vulnerabilities, or insufficient safeguards.

With all the hype around artificial intelligence, many of our customers are asking for some proof that AI can get them better results in areas where other kinds of analytics are already in use, such as creditriskassessment. My colleague Scott Zoldi blogged recently about how we use AI to build creditrisk models.

, AI helps companies manage risks better, it's like a big shift. It is changing how businesses deal with Enterprise Risk Management (ERM), and AI algorithms can always watch for risks. AI can look at lots of data, find patterns, and predict risks. AI also does tasks automatically and saves time for risk managers.

By merging credit spread data with essential corporate information, Agentic AI Company Research by martini.ai provides decision-makers including those in private credit with data-rich intelligence that highlights key trends, risks and opportunities. Rajiv Bhat, CEO of martini.ai With Agentic AI Company Research, martini.ai

In the dynamic world of financial services, the need for rapid and precise credit decisions has never been more crucial. This demand is driving a transformative shift towards leveraging Artificial Intelligence (AI) and automation to redefine credit and riskassessment strategies.

Generative artificial intelligence (AI), also known as gen AI, is expected to significantly impact risk management over the next five years, allowing financial institutions to automate tasks, accelerate processes and improve efficiencies. The tech can also draft model documentation and validation reports.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. This type of financial inclusion is good for the consumer and good for our business. by FICO.

(Photo by Dan Dimmock on Unsplash ) Ultimately, these tools enable enterprises offering trade credit to streamline collections and improve cash flow. Real-time insights into creditrisk and payment behaviors are turning AR into a strategic function that enhances efficiency, quality, and growth.

In this article, we’ll discuss what SaaS companies looking to become payment facilitators need to know about risk management strategies. PayFacs handle riskassessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks.

When it comes to using alternative data in creditriskassessments, the field has really opened up over the last few years. Here is useful information on how to assess alternative data and combine it with so-called traditional data to improve creditrisk models. Multiple Types of Alternative Data.

Inaccurate and slow creditriskassessment for [small- to medium-sized business (SMB)] commercial loan requests is one of the major reasons that over 50 [percent] of loans are currently declined by financial institutions (FIs),” said Roger Vincent, chief innovation officer at Trade Ledger.

With all the benefits of artificial intelligence, many of our customers are wanting to leverage machine learning to improve other types of analytic models already in use, such as creditriskassessment. My colleague Scott Zoldi blogged a few years ago about how we use AI to build creditrisk models. default rate.

This collaboration aims to introduce AI-led creditrisk management to KBZ Bank, enhancing its ability to assess creditworthiness across retail and SME products with greater accuracy and efficiency. said Sanjay Uppal, Founder and CEO of FinbotsAI.

ƒFord Motor Credit Co. 25) that it will implement machine learning credit approval models to determine if it will lend a consumer money as it goes after a segment of the market that doesn’t have a solid credit history. They are typically a good creditrisk and are expected to command $1.4

Having worked in creditrisk for most of my career during the revolution in analytics, it continues to concern me that the collections and recoveries (C&R) divisions of banks seem to be left behind. Innovations in creditrisk analytics that have been widely adopted in other risk areas rarely get used at the C&R level.

LexisNexis Risk Solution, a data and analytics company that helps loaners assess the risk of small business lending to borrowers, is teaming up with Cortera to add its trade credit analytics capabilities into the mix.

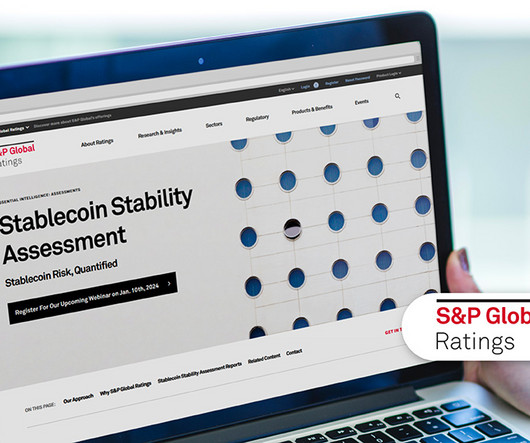

Credit rating agency S&P Global Ratings has unveiled its new stablecoin stability assessment service, designed to evaluate their capability in maintaining a stable value in comparison to traditional fiat currencies. The assessment methodology employed by S&P Global Ratings is thorough and multifaceted.

Credit scoring is widely used in South Africa to determine the risk of credit applicants — using this kind of objective, precise measure of risk lets banks, retailers and other organizations lend with more confidence, which in turn means more people get approved for credit. About the Empirica Score.

. Which works better for modeling creditrisk: traditional scorecards or artificial intelligence and machine learning? Take, for example, our new credit decisioning solution, FICO Origination Solution, Powered by FICO Platform. It’s designed to help lenders make faster origination decisions without increasing risk.

CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

16) said Lendingkart will offer its creditriskassessment technology to banks and other alt-lenders starting in 2017. According to Lendingkart Cofounder Harshvardhan Lunia, the company will look to expand its reach in the SME lending market over the next six months by having other banks use its creditrisk analytics software.

Managing fraud is a balancing act that starts with knowing your fraud risk appetite. Striking the right balance between top line growth, profitability, compliance, and protecting your bottom line against fraud loss means that establishing a fraud risk appetite is an imperative to success. Step 3 – Collaboration with Risk.

The company were asking me to advise them on the production of a ratings model, to help them rank their customers, old and new, for risk. For example, a firm might assess certain qualitative aspects of their clients, say “management capability”, and assign them a grade based on that.

“By analysing big data and rapidly assessingrisks, AI empowers financial companies to make well-informed decisions. However, a significant revolution lies ahead – the personalisation of services based on individual user assessments. “Finally, AI is reducing risk in the embedded insurance space.

Alternative lending companies are one of the strongest examples of how leveraging rich financial transaction data can be used to go beyond traditional creditriskassessments, says Finsync's Eddie Davis.

But it occurred to them that their solution was useful outside of HR — and that many of the things that made someone a good hire of over time could also make them a good creditrisk over time, if the artificial intelligence (AI) model they were using to screen with were modified to that task.

Ltd : Developed an ‘e-KYC’ solution to digitally onboard customers, using advanced technologies like artificial intelligence, machine learning, thumbprint and facial recognition for a streamlined digital KYC platform Soft Net Technology : Proposed a centralised loan application platform in response to pre- and post-Covid challenges.

Lenders are looking for new ways to connect with the estimated 3 billion people worldwide who fall outside the credit mainstream. These “credit invisibles” don’t have credit cards, bank accounts or credit history — so how can a lender assess their risk? those with a credit history.

And if that consumer is looking to secure any type of credit, the party on the other end of the transaction will use the FICO Score to critically inform an important decision: should my organization assume business risk by transacting with this person? A score that quantifies cyber risk.

By leveraging line-by-line transaction data, Recap’s creditrisk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

Even more significantly, our research shows that FIs are using AI with greater focus than they have in the past, with two areas emerging as key applications: payments fraud and creditrisk. Supervised systems like BRMS are simply not capable of responding to the dynamic, constantly shifting nature of these risks.

The use of scores that rate a firm’s cybersecurity risk — such as the FICO® Enterprise Security Score — is picking up momentum. As more entities rely on these scores and ratings, their governing bodies and relevant regulatory agencies will care more about how these tools are used to drive decisions to mitigate risk.

Analysis of FICO® Resilience Index data by Tom Parrent, former chief risk officer for Genworth Financial, shows that from 2010 to 2015, nearly 600,000 additional mortgages could have been originated to consumers with FICO® Scores between 680 and 699, had the FICO® Resilience Index been available to lenders at the time.

What were some of the most interesting risk analytics topics last year? Judging from the views on the FICO Blog, risk professionals are keenly interested in new ways to approach risk analytics. Here were the top 5 posts of 2017 in the Risk & Compliance category: US Average FICO Score Hits 700: A Milestone for Consumers.

How can lenders best measure and manage creditrisk, given the disruptive patterns in consumer behaviour over the last 18 months? Last week a FICO team met with chief risk officers from some of the biggest UK banks to discuss these and other challenges, at our UK CRO Summit. Managing Risk Models in a Crisis.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content