This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thai regulators approved the first cross-border payment solution using stablecoins in October, while the Philippine central bank launched a peso stablecoin pilot earlier this year. Pollak emphasized that stablecoins aim to modernize legacy financial systems rather than replace national currencies.

Unfortunately, an estimated 3 billion people worldwide fall outside the credit mainstream – they either don’t have a bank account or they have so little data at the credit bureau that lenders may skip over them, or classify them as very high risk. The post New Ways to Score Risk Can Improve FinancialInclusion appeared first on FICO.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The evolution of open banking into open finance, examining regional regulatory approaches and adoption trends. Why is it important?

Home Credit , a global non-bank consumer lender, has successfully reduced its credit risk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. For its achievement, Home Credit was awarded the 2019 FICO® Decisions Award for FinancialInclusion.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. We hear from industry experts on how embedded finance ensures the checkout experience is financiallyinclusive.

HSBC UK recently became the first major bank to enable international customers to leverage their international credit history to apply for a UK mortgage application. While this represents a significant step forward, should financialinclusivity have moved further ahead by now? Then we’ll make real progress.”

The scoring methodology was developed by EFL Global and marketed by FICO as part of our FICO FinancialInclusion Initiative , designed to open up credit markets around the world to a larger number of unbanked and underserved consumers. The post A New Way to Score Credit Risk – Psychometric Assessments appeared first on FICO.

These trends include ecosystem banking, generative artificial intelligence (GenAI), and embedded finance, a new report by PwC India and ASSOCHAM says. Generative AI driving banking and fintech trends in India Generative is one of India’s biggest fintech trends highlighted in the report.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. “By analysing big data and rapidly assessing risks, AI empowers financial companies to make well-informed decisions. .

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. Whether it be retailers, ride-hailing apps, super-apps, or other non-bank service providers, embedded finance appears to be making its way into every sub-sector.

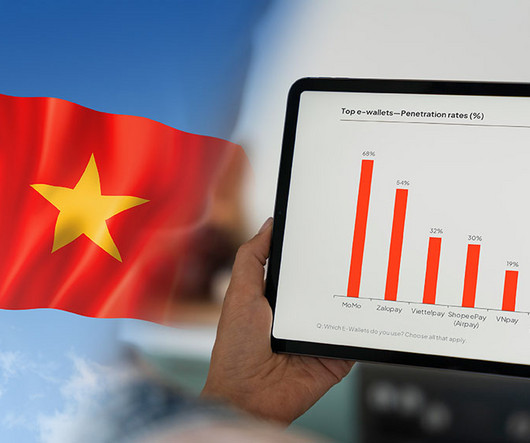

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

Al Ansari Exchange , the UAE-based remittance and foreign exchange company, and Ruya Islamic Community Bank (ruya), a digital-first Islamic community bank, are working together to enhance financialinclusivity and convenience for customers across the UAE.

Borrowers can now apply for loans, track progress, and make payments through digital platforms and mobile apps, eliminating the need for physical branches and banking hours. This accessibility benefits those in remote areas or with busy schedules, ensuring financial services are within everyone’s reach.

B Corp is a rigorous assessment that verifies companies have met high standards of social and environmental performance, transparency, and accountability: theres absolutely no room for mere box-ticking. “Today we have no real way to be sure that our favourite fintech is as ethical and good as it claims to be.

Bank Alfalah, one of Pakistan’s largest commercial banks has already invested in Qist Bazaar, leading the seed round. ” Strategic Backing from Industry Leaders Qist Bazaar has benefitted from an early equity partnership with Bank Alfalah, which led their seed round. billion in assets under management (AUM).

The event will explore cybersecurity careers within the banking, finance, and fintech sectors, particularly in response to the increasing frequency of cyber attacks. The session will be moderated by Urs Bolt, a Fintech and Banking Expert.

Money20/20 Asia made its debut in Bangkok on April 23, 2024, bringing together key players from across Asia’s financial landscape, including banks, payment providers, startups, retailers, fintech companies, and regulators. Additionally, they can access developer guides on API technology and security protocols.

These “credit invisibles” don’t have credit cards, bank accounts or credit history — so how can a lender assess their risk? The EFL score uses psychometrics and behavioral data to measure a person’s credit risk based on an applicant’s answers to a series of interactive questions and exercises administered via an online assessment.

These awards highlight companies and individuals whose fintech initiatives have contributed to advancing financial technology, promoting financialinclusion, and improving service delivery. Integrated with bank accounts and digital wallets in Pakistan, Hakeem provides customers with easy disbursement options.

Artificial intelligence (AI) is transforming this landscape by introducing a more dynamic and comprehensive way of assessing creditworthiness. Unlike conventional models, AI-driven credit scoring does not depend solely on historical financial data. AI also enhances risk management for financial institutions.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. And then trust.

Data monetization in the banking sector has become increasingly prevalent in recent years, driven by evolving customer expectations, new data sharing rules and opportunities for new revenue streams. Data monetization refers to the process of using data to obtain quantifiable economic benefit. This enhances the overall customer experience.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

Fintech Thailand is poised for significant growth and development in areas including digital banking, open finance, and startup support. With cashless payment becoming ubiquitous, the Bank of Thailand (BOT) is now paving the way for open finance, aiming to enhance consumer access to financial services.

Digital financial platform, Ribbon , is gearing up for its next big move to help non-resident Indian diaspora in the UK, as it announces its partnership with Tribe Payments , the digital payments and infrastructure orchestrator that specialises in issuer and acquirer processing.

Tribe Payments , a leading digital payments and infrastructure orchestrator that specialises in issuer and acquirer processing, has partnered with digital financial platform, Ribbon , enabling the company’s launch first in Gibraltar and, most recently, in the UK.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

From bustling megacities to remote villages, digital finance is breaking down barriers, giving millions access to banking, credit, and investment opportunities for the first time. million Samrat Investments , also known as Samrat FinancialBanking, offers what it says is the world’s first customisable personal savings platform.

A New Way to Score Credit Risk – Psychometric Assessments. Explained author Campbell Scott , “The scoring methodology was developed by EFL Global and marketed by FICO as part of our FICO FinancialInclusion Initiative , designed to open up credit markets around the world to a larger number of unbanked and underserved consumers.

Aadhaar-enabled Payment Service (AePS) AePS, in India, enables individuals to conduct basic banking transactions like d eposits, withdrawals, balance inquiries, bill payments, etc. without requiring a traditional bank account or debit card. Unlike physical cash or bank deposits, CBDCs are purely electronic.

Our winners have innovated in lending, supply chain optimization, customer management, debt collection, fraud and financialinclusion. Leslie Parrish , analyst – retail banking at Aite. They come from all corners of the globe and many varied sectors of the economy. Sharon Kimathi , editor at FinTech Futures.

These products and services are safe, highly secure, and promote financialinclusion by allowing consumers including lowandmoderate income consumers who have historically not had full access to the financial system to conduct their everyday financial transactions. states and territories.

Open Banking in the Philippines and the Opportunities in the Data. Open Banking in the Philippines - the path ahead. Open Banking in the Philippines promises to give customers the control to share their data and allow third-party providers to access their data. How data sharing can improve credit risk decisioning. FICO Admin.

Last month at FinovateEurope, we introduced Swedish embedded banking and payments company Visualizy to our audiences. Founded in 2022, the company offers a multi-bank platform that helps businesses lower costs, reduce errors, and boost security in their financial and payment operations. open banking a major boost.”

Peer-to-peer lending platforms connect borrowers directly with individual lenders, cutting out traditional banking intermediaries. Online lending platforms leverage advanced algorithms to assess creditworthiness rapidly, enabling faster loan approvals. These data points provide a more comprehensive view of a businesss financial health.

In the past decade, the financial services sector has witnessed an exciting shift. Fintech companies and traditional banks are increasingly working together. Historically seen as competitors, fintechs and banks now find common ground to enhance services and reach broader audiences. Why Are Banks and Fintechs Collaborating?

True financialinclusion depends on bridging digital exclusion while allowing for natural market evolution. This dual focusa “digital inclusion bridge”is essential as the UK continues its transition to a more digital economy. of digitally excluded individuals lacking access to a bank account.

Microfinance institutions (MFIs) play a crucial role in driving financialinclusion by providing a suite of financial services tailored specifically for the underserved and unbanked populations in remote and rural areas. This end-to-end management helps improve collection efficiency and portfolio health.

In our extended conversation, Jumaniyazov helps us understand the size and scope of Islamic and Shariah-compliant finance, the unique needs of the customers in this growing market, and how enabling technologies are bringing innovation to Islamic financial services in areas such as banking to wealth management. In the U.K.,Islamic

The payments industry in 2024 saw rapid evolution, marked by the growing adoption of real-time payments, advances in AI-driven fraud detection, and significant progress in Central Bank Digital Currencies (CBDCs). One of AI’s most transformative roles is in fraud detection and prevention.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content