This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thai regulators approved the first cross-border payment solution using stablecoins in October, while the Philippine central bank launched a peso stablecoin pilot earlier this year. During the event, participants, including non-Thai attendees, were able to convert dollar stablecoins to baht stablecoins without foreign exchange fees.

Singapore has released its updated Terrorism Financing National Risk Assessment (TF NRA) and National Strategy for Countering the Financing of Terrorism (CFT) to address terrorism threats. The assessment also notes the rising concern of far-right extremism, although it has not significantly impacted Southeast Asia.

The Many Types of Payment Processing Fees Below is a breakdown of the lesser-known or hidden fees that can show up on your monthly statements: Interchange Fees What It Is: The fee paid to the card-issuing bank every time a customer buys something with a credit or debit card. Cost Range: Usually 1.5%3.5% on top of interchange fees.

It helps assess and mitigate security risks systematically by identifying vulnerabilities and implementing controls to address them before they materialize. Assess the environment by identifying where and how cardholder data is stored, processed, or transmitted within your business operations. of PCI DSS. of PCI DSS. of PCI DSS.

Interchange and assessment fees are set by card networks and are non-negotiable. Acquiring bank – The merchants bank that receives and disburses the funds. They facilitate transactions by connecting merchants, credit card processors, and banks while establishing rules, regulations, and fees for processing payments.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The evolution of open banking into open finance, examining regional regulatory approaches and adoption trends. Why is it important?

It highlights new corporate responsibilities, significant penalties for non-compliance, and the businesses need to implement strong fraud prevention measures to protect their financial and reputational standing. Compliance requires proactive fraud risk assessment, the implementation of preventive procedures, and a culture of accountability.

As per a survey conducted by Dragonfly Financial Technologies at the beginning of the year 2024, 92% of banks planned to maintain or increase their technology investments in 2024. This includes regular risk assessments, controls, and monitoring mechanisms to address vulnerabilities and threats.

The merchant underwriting process is a critical step that payment processors and financial institutions use to assess the risk associated with onboarding new businesses. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

Singapore has released an Environmental Crimes Money Laundering National Risk Assessment (NRA), highlighting the primary threats and vulnerabilities associated with it. Banks and cross-border payment service providers are especially at risk of being exploited for laundering proceeds from these crimes due to their transnational operations.

It applies to any entity that processes, stores, or transmits credit card information making it especially relevant to banks and financial institutions. Non-compliance can lead to hefty fines, security vulnerabilities, and loss of customer trust. Continually assess and refine your systems to address evolving threats.

Interchange Fees These go directly to the customers bank (the card-issuing bank ). and non-negotiable. Card Brand Fees Also known as assessment fees, these are charged by Visa, Mastercard, American Express, and Discover. Also non-negotiable. Rates vary by card type (e.g., Usually a small percentage (e.g.,

Singapore has released its updated Money Laundering (ML) National Risk Assessment (NRA) , highlighting increased risks in the digital payment token (DPT) services sector. The updated assessment highlights increased risks due to economic and geopolitical shifts, as well as the rise in technology-enabled transactions.

The collaboration integrates Plaid’s open banking services with Capitalise’s Instant Offers to simplify and streamline small business funding. The partnership is designed to simplify business funding, leveraging Open Banking to offer pre-approvals to 150,000 small businesses. are embracing open banking technology.

Table of Contents What Are Dues and Assessment fees? What is the difference between a fee and an assessment? What is the Difference Between Acquirer Fees and Dues and Assessments? What is the Difference Between Assessments and Interchange Fees?

Because it is mandated by payment card brands and banks for all businesses handling payment card data. This puts them in a prime position to become targets for cybercriminals, making payment security compliance non-negotiable. They require an annual on-site assessment by a Qualified Security Assessor (QSA) and quarterly scans.

Because it is mandated by payment card brands and banks for all businesses handling payment card data. This puts them in a prime position to become targets for cybercriminals, making payment security compliance non-negotiable. They require an annual on-site assessment by a Qualified Security Assessor (QSA) and quarterly scans.

A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%. The company facilitates the transfer of information and funds between the customer’s bank and your business’ bank.

As per a survey conducted by Dragonfly Financial Technologies at the beginning of the year 2024, 92% of banks planned to maintain or increase their technology investments in 2024. This includes regular risk assessments, controls, and monitoring mechanisms to address vulnerabilities and threats.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. “By analysing big data and rapidly assessing risks, AI empowers financial companies to make well-informed decisions. .

A combination of superior risk assessment, fraud detection capabilities, and quick and accurate underwriting turnaround can transform a lender’s success rate with borrowers and reduce non-performing assets. The revenue growth and profitability of a lending business depend on several factors.

Acquiring bank This is the merchant bank that allows the business to receive money from card transactions and store these funds. The issuing bank This is the cardholders bank or the financial institution that issued their credit or debit card. Think: Visa, Mastercard, American Express, and Discover.

and can cover the costs associated with transferring funds between banks, fraud prevention, and compensating card networks, payment processors, and issuing banks. Assessment fees are imposed by credit card networks to cover the cost of operating their global networks. These fees typically range from 1.5%

Interchange, as set by Visa and Mastercard, is non-negotiable. Downgrades and Enhanced Data Categories: The Non-Malicious Problem Padded Interchange: The Malicious Problem Costs of Processing Appearing Competitive Is padded interchange the same as tiered pricing? The other two are assessments , which can also be padded, and markup.

This system guarantees secure data transmission between banks and card networks like Visa, Mastercard, and Discover. Merchant service accounts and how they work Merchant service providers assess your credit history, business type, and expected transaction volume during application. POS systems and card readers.

The new regulations, if adopted after a comment period, would require banks and some other institutions to obtain and report the identities of parties engaging in certain digital transactions, including payments involving what are called "unhosted wallets" – effectively secret bank accounts that hold cryptocurrency.

Borrowers can now apply for loans, track progress, and make payments through digital platforms and mobile apps, eliminating the need for physical branches and banking hours. “One-click” loans become reality through instant credit assessments. For example, more accurate credit assessments lead to reduced default rates.

These trends include ecosystem banking, generative artificial intelligence (GenAI), and embedded finance, a new report by PwC India and ASSOCHAM says. Generative AI driving banking and fintech trends in India Generative is one of India’s biggest fintech trends highlighted in the report.

Now celebrating its 20th anniversary edition, the report predicts instant payments will account for 22% of all non-cash transaction volumes by 2028 globally. Non-cash transactions boom; APAC leading adoption Non-cash transaction volumes rose to 1,411 billion in 2023 and are on track to reach 1,650 billion in 2024.

Embedded finance is transforming industries by incorporating financial services directly into non-financial platforms. This integration allows businesses to offer banking-like services, enhancing customer experience and simplifying transactions. This shift is redefining traditional banking structures. What is Embedded Finance?

But open banking has struggled due to inconsistent API access from incumbent banks. As non-financial platforms increasingly offer financial services under their own names, she pointed out, this raises significant regulatory challenges. When PIS was introduced, it seemed like the future, she remarked.

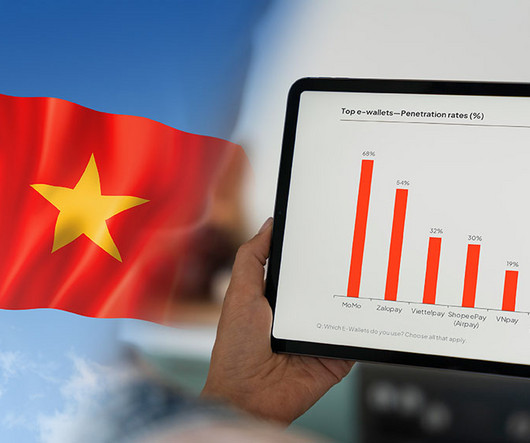

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

Home Credit , a global non-bank consumer lender, has successfully reduced its credit risk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. They are one of our most sophisticated clients in terms of advanced analytics.”. by FICO.

The Reserve Bank of India (RBI) has released the Draft Directi ves 2025 on Lending Against Gold Collateral, bringing a much-needed regulatory reset to a sector thats long operated in silos. Financial Implications: Non-compliance could result in financial penalties, provisioning burdens, or reputational damage.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. Whether it be retailers, ride-hailing apps, super-apps, or other non-bank service providers, embedded finance appears to be making its way into every sub-sector.

Arctic Intelligence (Australia) Headquartered in Sydney, Australia, Arctic Intelligence is a multi-award-winning regtech company specializing in financial crime risk assessment technologies. For larger enterprises and the consultants assisting them, Arctic Intelligence offers the Risk Assessment Platform. Transparently.AI

One major focus is on proactive prevention, where the IMC advocates for tighter regulations on corporate service providers and enhanced due diligence for non-financial sectors vulnerable to exploitation by money launderers. The IMC’s recommendations aim to adapt Singapore’s AML framework to counter increasingly sophisticated criminal methods.

Al Ansari Exchange , the UAE-based remittance and foreign exchange company, and Ruya Islamic Community Bank (ruya), a digital-first Islamic community bank, are working together to enhance financial inclusivity and convenience for customers across the UAE.

And when that happens, non-compliance can lead to many degrees of harm to any and all business owners. This includes applying security patches promptly, conducting regular vulnerability assessments, and maintaining secure coding practices throughout the development lifecycle.

Banks, fintechs, all other financial institutions and their supply chains must take the necessary steps to comply or risk paying a very heavy price both financially and reputationally. Banks and other companies which provide financial services in Europe already have plans in place for their IT security, but we need to go one step further.

These schemes are facilitated by the fact that many BNPL firms do not conduct formal credit checks, instead relying on internal algorithms to quickly assess new clients. The legislation established the CCOB and the Council for Consumer Credit Malaysia (CCC) to ensure fair treatment across financial services providers, including non-banks.

Credit card processing fees are comprised of several fees, such as: Interchange fees: Interchange fees are paid to the card-issuing bank and typically consist of a percentage of the total transaction amount plus a small, fixed charge. Assessment fees: Assessment fees are imposed by major credit card networks (Visa, Mastercard, etc.)

TL;DR Credit card interchange fees are the fees that merchants pay to banks and credit card companies every time they accept credit cards. Interchange fees themselves are non-negotiable and they’re charged whenever a merchant accepts credit card payments. Assessment fees Then, you’ve got assessment fees.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. First, we turn our attention to the growth of Banking-as-a-Service (BaaS). “Do they have a banking licence that means their customers’ money is protected up to a certain level?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content