This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is where PCIDSS (Payment Card Industry Data Security Standard) compliance becomes essential for Australian businesses. In todays article, we are going to learn how PCIDSS compliance protects businesses from data breaches. Protecting cardholder data: Encrypting sensitive data during transmission.

As a merchant, to understand tokenization for your own benefit, it’s critical to understand: What tokenization is, why it’s important for payments, and how it compares to encryption. How tokenization applies to being PCI compliant and meeting the 12 PCIDSS requirements.

You can also check out the PCI at a glance infographic for a quick overview. For simplicity, I will just refer to PCIDSS standards as PCI for the rest of this article. What is PCI again? In the past, Ive written about how to achieve and maintain PCI compliance. Timeline PCI version 4.0

Ensure the gateway offers PCIDSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. The payment gateway collects and encrypts sensitive customer payment details and then securely sends them to the payment processor. Learn More What is a Payment Gateway?

It occurs in a matter of seconds but consists of multiple stages, from authorization to settlement. Stage 1: AuthorizationAuthorization is the initial step where the transaction is approved or declined. Card Network Communicates with Issuer : The card network forwards the request to the issuing bank for authorization.

This routing allows the processor to request authorization for the transaction from the issuing bank, which then approves or denies it based on factors like available funds and fraud checks. Routing : The payment processor routes the transaction request to the appropriate issuing bank for authorization.

It works in tandem with the customers bank or credit card provider to verify and authorize the transaction. It forwards the customers payment details to the issuing bank, gets transaction authorization, and collects the funds on behalf of the eCommerce business. But with more control comes great responsibility.

Payment gateway – The service that encrypts and securely sends payment details from the customer to the payment processor and back to the merchant. It authorizes or declines payments based on available funds and fraud checks. This means they authorize and complete transactions faster than manual processing procedures.

Look for features like transaction monitoring, biometric logins, and encrypted data. External This content is provided by an external author without editing by Finextra. It expresses the views and opinions of the author. It expresses the views and opinions of the author. It expresses the views and opinions of the author.

Why Traditional Defences Fall Short Historically, businesses have relied on layered security controls like encryption, firewalls, and access policies to protect payment information. Standards like PCIDSS don’t currently mandate tokenisation for bank details, but forward-thinking organisations aren’t waiting for legislation to catch up.

The gateway acts as the intermediary that collects, encrypts, and transmits transaction data to the payment processor. Transaction settlement: After a payment is authorized, the merchant account facilitates the settlement process. Data encryption: Data is encrypted and sent to the payment processor.

Authorization The credit card details captured by your POS or online payment gateway will be sent to your payment processor. It also ensures that data security best practices, particularly PCIDSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data.

The customer will input the required payment information on the page and then click Pay to authorize the transaction. Payment verification Once the payment processor receives the now-encrypted payment information, it will be sent to the issuing bank for verification. However, credit and debit cards are more convenient.

Data is Encrypted & Tokenized Immediately after submission, the payment gateway encrypts the card data and replaces it with a token—a random, one-time-use ID. This tokenization keeps the sensitive card information off your servers, reducing the risk of a data breach and easing PCIDSS compliance.

Payment security A reliable Sage 100 payment processing solution will protect customer payment information by implementing robust security protocols and ensuring full compliance with Payment Card Industry Data Security Standards (PCI-DSS).

Access to that external data is also strictly controlled, and even people with authorized access must verify their identity via two-factor authentication and other means. This is to ensure customers can easily find the button when evaluating payment options on your site.

Meanwhile, a payment gateway is the technology that authorizes and processes payments between a buyer and seller by securely transmitting payment data. Meanwhile, a payment gateway is the technology that authorizes and processes payments between a buyer and seller by securely transmitting payment data. How do they work together?

Compliance with industry standards: Compliance with Payment Card Industry Data Security Standards (PCI-DSS) is another significant benefit of integrating a payment gateway into Acumatica. Opt for a PCI-compliant gateway with encryption, tokenization, and fraud detection tools to protect customer data and prevent chargebacks.

A payment gateway solution is a service that authorizes credit card payments and processes them on behalf of the merchant. A Payment Gateway for a mobile app is a service that authorizes credit card payments and processes them on behalf of merchants. Q: What are the security considerations while choosing a Payment Gateway?

NetSuite automates key aspects of the payment process, including authorization, capture, and settlement, reducing manual effort and minimizing errors. Additionally, it includes security features such as tokenization, encryption, and fraud prevention tools to ensure compliance with Payment Card Industry Data Security Standards (PCIDSS).

Increased security and compliance: Reputable Salesforce payment integrations are designed with strong security protocols and compliance with Payment Card Industry Data Security Standards (PCIDSS). Youll also want to ensure that role-based permissions are configured correctly so only authorized users can access or manage payment data.

When a customer initiates a payment, the gateway securely transmits the information to the payment processor and the issuing bank for authorization. Overall, the payment gateway acts as a secure bridge that encrypts sensitive data, such as credit card details, to ensure the transaction is processed safely and efficiently.

These fees cover the cost of securely transmitting payment data, encrypting sensitive data, and authorizing transactions in real-time. Gateway fees: Gateway fees are the fees merchants pay to use a payment gateway, which acts as a bridge between their website or point-of-sale (POS) system and the payment processor.

Its role is to encrypt and securely transfer your customers payment data to your payment processor. All the data transfer between the digital wallet and your payment terminal are encrypted and the system also uses tokenization to ensure iron-clad data security. Your customer can give out a cashier check or a certified check.

PCI compliance and security Integrated payment gateways typically come with built-in security features such as full compliance with Payment Card Industry Data Security Standards (PCIDSS) , tokenization, and encrypted data transmission.

Your payment processor will provide the necessary payment portal software to authorize and transfer funds from customers accounts to your businesss account. A payment portal facilitates electronic transactions between merchants and their customers, providing a seamless way to pay and collect invoices quickly and securely.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

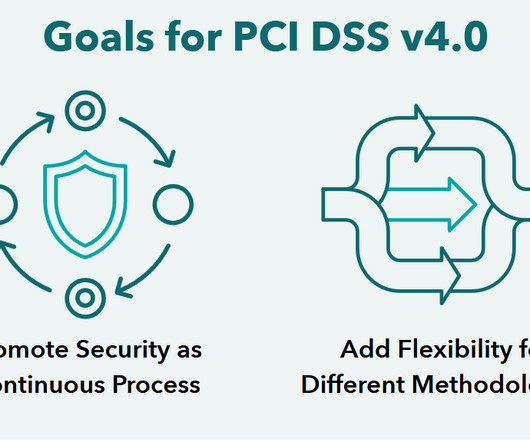

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0 c: Confirm that software applications comply with PCIDSS. - c: Confirm that software applications comply with PCIDSS. - In PCIDSS v4.0, In PCIDSS v4.0,

In our exploration of PCIDSS v4.0’s This is achieved through a multi-pronged approach: Data Encryption: Requirement 3 mandates the use of strong cryptographic controls such as encryption for stored cardholder data. Changes in Requirement 3 from PCIDSS v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0

When a passenger ‘taps on’, the NMI Gateway processes initial authorization and card tokenization, as well as subsequent authorization and settlement at ‘tap-off.’ ’ The NMI Gateway also handles deferred authorization for any transactions that fail or are declined.

Today, the framework introduced in the early 2000s outlines 12 PCI requirements that merchants must satisfy to process credit card transactions on the card networks. Nearly 20 years later, with more than 300 requirements and sub-requirements, PCIDSS continues evolving. Don't, however, let the term "merchants" fool you.

The customer’s issuing bank validates this token to authorize the transaction, ensuring the security of the customer’s real data while allowing transaction processes to occur. Once the information is entered, it’s immediately encrypted and sent to the tokenization system. How Does Payment Tokenization Work?

TL;DR PCI compliance is essential because it helps prevent data breaches, ultimately cultivating customer trust. There are 12 requirements under PCIDSS, divided into six major categories. What is PCI Compliance? PCIDSS stands for “Payment Card Industry Data Security Standards.”

In this guide we will discuss the following: What is Payment Tokenization How Payment Tokenization Works Payment Tokenization vs. Encryption SaaS Payment Tokenization Requirements Benefits of Payment Tokenization SaaS Payment Vulnerabilities Using Stax Connect and Payment Tokenization Lets get started.

PCIDSS compliance, a global framework, mandates specific requirements and best practices for maintaining credit card data security. Subscribe to regulatory updates or newsletters from relevant federal authorities, such as the PCI Security Standards Council (more on this later). Enter the PCIDSS compliance.

In a payment scenario, the PIN helps confirm that the person using the card is authorized to do so. This ensures that only the person who knows the PIN can authorize the payment. PIN Encryption : Once the customer enters the PIN, it is encrypted immediately to protect the information.

Enter the Payment Card Industry Data Security Standard (PCIDSS): a comprehensive framework that sets forth stringent rules and regulations to ensure the secure handling, processing, and transmission of cardholder information. As we approach the highly anticipated release of PCIDSS 4.0 a notable change is on the horizon.

A crucial aspect of risk management involves adhering to the Payment Card Industry Data Security Standard (PCIDSS) , which sets stringent guidelines for securing payment transactions and protecting cardholder information. Secure Network Configurations Configuring secure networks is fundamental to PCIDSS compliance.

The primary security standards that payment systems typically adhere to include: Payment Card Industry Data Security Standard (PCIDSS): PCIDSS sets forth requirements for securing payment card data, including encryption, access control, network monitoring, and regular security testing.

There are various methods of enforcing data security, such as data masking, encryption, authentication, and data tokenization. Confidentiality means that data should be accessible only to authorized users. Moreover, companies need to follow data privacy and compliance requirements to stay in business.

Integration with Payment Gateways: The terminal connects to multiple payment gateways, which are services that authorize and process payments. Secure Transactions: Online terminals incorporate security protocols like SSL encryption, tokenization, and Payment Card Industry Data Security Standards (PCIDSS) compliance.

The Payment Card Industry Data Security Standard (PCIDSS) plays a crucial role in protecting cardholder data for businesses that accept credit card payments. As a business owner or professional, it’s essential to understand the importance of PCI compliance and its requirements.

Be prepared to cooperate with law enforcement authorities and follow any instructions they provide during their investigation. Merchants should invest in secure payment processing systems, utilize encryption technologies, and comply with Payment Card Industry Data Security Standard (PCIDSS) requirements.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content