This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Selling products and services internationally means facing new challenges, especially regarding payment processing, regulatory requirements, currency exchanges, and fraudprevention. FraudPrevention and Security Cross-border transactions have higher fraud risks than domestic payments.

It highlights new corporate responsibilities, significant penalties for non-compliance, and the businesses need to implement strong fraudprevention measures to protect their financial and reputational standing. Firms must be required to have fraudprevention policies in place and demonstrate their effectiveness.

This article outlines how to structure your chargeback management team, define roles, implement processes, select the right software, and adhere to bestpractices. FraudPrevention Specialists Responsibilities: Monitor transactions for fraudulent activity and implement fraudprevention measures.

It shows that forward-thinking merchants using diverse, strategic payment solutions gain clear advantages in cost control, fraudprevention, and customer experience. 29% of businesses find fraudprevention extremely challenging—making it the most severe concern across all payment-related issues. Why is it important?

Bestpractices for strengthening controls To enhance the fight against money mule activity, firms should: Increase NFD reporting Firms must take a more consistent approach to reporting money mules, ensuring that all cases meeting the standard of proof are submitted.

As industries face increasing regulatory pressures, Seon Technologies will highlight the shared challenges of customer onboarding, fraudprevention and compliance, including how businesses navigate global KYC and AML regulations.

The digitization of public financial systems introduces new challenges for online payment fraudprevention. Because public financial systems involve essential funds and taxpayer dollars, dedicated government frauddetection systems are paramount to combat fraud—and ensure government accountability.

A secure payment processing provider for Sage 100 will also give merchants access to frauddetection and prevention tools, 3D Secure, chargeback management, and more. By protectin g payments in Sage 100, your company can reduce the risk of data breaches and fraud, ensuring a secure experience for all parties involved.

The solution: robust government frauddetection mechanisms for payment systems. Here’s what compliance managers and auditors need to know to strengthen internal fraudprevention and safeguard public funds. When fraud persists for over five years, the average loss increases to $800,000.

In a recent blog post , I discussed how FICO is fighting application fraud by leveraging artificial intelligence (AI) and machine learning in frauddetection, including an overview of supervised, unsupervised, and adaptive analytics techniques and the need to balance transparency (explainable AI) with predictiveness.

Key findings from the whitepaper highlight that: The speed and ease of global payment channels allow criminals to exploit system gaps across jurisdictions, complicating frauddetection. According to Gary Palmer, CEO and Founder of Payall, “APP fraud is a growing issue in cross-border payments.

Building and Structuring a Chargeback Team To manage chargebacks effectively, you’ll want to create a team that includes poeple skilled in finance, customer service, and fraudprevention. Fraud Specialist: The Guardian The fraud specialist identifies fraudulent transactions to reduce chargebacks.

This makes it imperative for businesses to stay ahead with robust frauddetection and prevention strategies. Acquiring banks have a vested interest in helping their merchant clients stop eCommerce fraud, as it directly impacts the financial stability and reputation of both parties.

Driven by a shared commitment to nurture talent, the partnership provides a framework for the two organizations to collaborate on attracting high skilled talent, advancement of local talent through the exchange of knowledge and bestpractices and development of joint initiatives to foster innovation and growth of the local fintech ecosystem.

Their comprehensive discussion sheds light on the significance of advanced AI and frauddetection technologies, and the importance of collaborative efforts to mitigate these risks. “Even people who are trained on deep fakes have a real difficulty determining what’s a real image from an image created using a deep fake.”

By the time financial institutions discover the fraud, recovery becomes nearly impossible. Why Traditional FraudDetection Fails Credit bureaus face fundamental limitations in identifying synthetic identities. Fair lending laws complicate prevention efforts. Members share data, bestpractices, and technology solutions.

Guest panelists included James Nurse, Managing Director at FINTRAIL; Hannah Becher, Lead of Fraud and AML Surveillance at Pleo; Matthew Tataryn, Director of Financial Crime Risk at Tide Platform; and Jeremy Doyle, Director of Growth, AML Solutions at SEON.

With fraud accounting for a significant portion of UK crime, understanding AIs role is critical for developing effective, future-ready defences. Payments leaders should focus on improving data quality, fostering cross-sector collaboration, and responsibly integrating AI into fraudprevention strategies.

This information also allows for the integration of AML checks, such as a match on a sanctions list or association with PEPs, to significantly alter the individual’s risk profile, thereby enhancing the overall effectiveness of frauddetection and prevention mechanisms.

Identity theft, data breaches, and chargeback fraud are some of the most common types of risks. This is why you need robust frauddetection mechanisms and ensure that they are up-to-date. It can also help to teach them about bestpractices they can follow to prevent fraudulent transactions.

According to the latest Payments 2022 Playbook: Building A High-Performing Payments Team For FraudDetection , a PYMNTS study in collaboration with Stripe, digital platforms continue to express discontent with their current fraud strategies, and false positives are compromising their brands, customer relationships, and bottom lines.

The rising sophistication of AI-generated deepfake images and videos poses an increasing risk to the payments industry, making advanced frauddetection more critical than ever. This engagement further positions ID-Pal as a thought leader in fraudprevention, particularly in combating AI-fraud.

It will focus on several key areas: Advanced FraudDetection and Prevention: Developing and implementing cutting-edge technologies to detect and prevent financial fraud. The center will provide a platform for the exchange of ideas and bestpractices between the public and private sectors.

SEON recently brought together industry leaders from the online lending space to discuss the evolving landscape of fraudprevention and risk management. The Changing Face of Fraud In what many describe as an “unpredictable era,” lenders are collectively challenged to stay ahead of increasingly sophisticated fraudsters.

Additionally, leveraging advanced frauddetection tools and machine learning algorithms in real-time helps analyze transaction patterns and differentiate between legitimate and potentially fraudulent activities. One key practice involves prioritizing customer satisfaction through the delivery of exceptional customer service.

“In most cases, the quality and quantity of data used for training, testing, and refining an AI model, including those used for cybersecurity and frauddetection, directly impact its eventual precision and efficiency.” These observations are among ten takeaways from the report shared last week.

We know neobank risk teams must stay aware of evolving threats and take an active approach to closing those routes to fraud. This is why, in this article, we examine the five most common types of fraud in neobanking and how to protect against them – no matter how mature your approach to fraudprevention is.

Many are using digital banking services for the first time, though, meaning they may be unaware of personal security bestpractices. Lori Hodges, vice president of risk in North America for Visa, has said even fraudprevention professionals have let their guards down. Phishing attacks are some of the most common scams.

Common risk management strategies for PayFacs include proper merchant vetting and onboarding, transaction monitoring and fraudprevention, chargeback mitigation, KYC/AML compliance, and data breach prevention. Frauddetection and prevention. Early detection can help in the rapid mitigation of fraud.

In this case, both the cardholder and the merchant are victims of Fraud. Merchants should implement robust frauddetection tools, such as address verification systems (AVS) and card verification value (CVV) checks. Each card brand applies different chargeback thresholds. Chargeback ratios also differ per industry.

FIs must ensure that their analytics and business intelligence efforts are constantly recalibrated, with an eye on frauddetection, user friction and false positives. Fraud is not static, said Srinivasan.

TSYS’ ProPay has paired up with InfoTrax to help direct selling companies battle fraudsters by integrating ProPay’s Guardian CyberShield frauddetection and protection service into its DataTrax back-office software. It is also used to prevent account takeover, payment fraud, identity spoofing, malware and data breaches.

Evaluate transaction fees, chargeback policies, and currency conversion rates to prevent unexpected expenses and optimize revenue retention. Security & FraudPrevention Given the high-risk nature of online gaming, security is non-negotiable. Implement real-time frauddetection and chargeback management to enhance security.

Enhance Employee Awareness and Training: Provide comprehensive training to employees on fraudprevention, detection, and reporting. Promote a culture of ethics and integrity, emphasizing the consequences of fraud. Educate employees on common fraud schemes and red flags to watch out for in day-to-day operations.

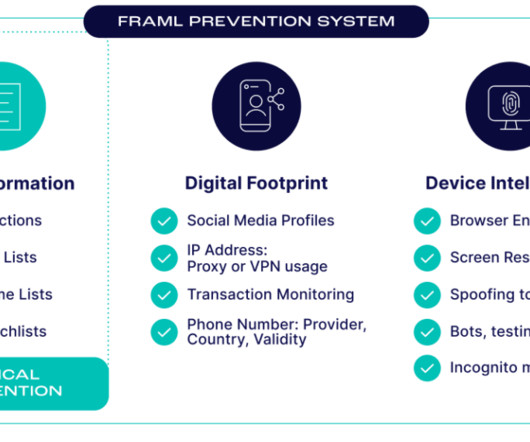

Advanced technologies, including artificial intelligence (AI), blackbox and whitebox machine learning (ML), digital footprinting and device intelligence, collectively transform the real-time frauddetection and prevention paradigm. Engage senior leadership in the governance and oversight of fraud risk management efforts.

The best PSP is the one that provides the right package of payment options for your customer base, adequate frauddetection & prevention tools, scalability, robust customer care services, and charges affordable processing fees.

Businesses are encouraged to familiarize themselves with the procedural steps of cash reconciliation, adopt bestpractices to enhance accuracy, and consider the benefits of automating the process to mitigate risks associated with manual reconciliation. Looking out for a Reconciliation Software?

Under NACHA’s operational guidelines, entities are expected to establish risk management practices proportional to the extent and nature of their ACH activities. As transaction volumes or the complexity of the ACH services increase, institutions or service providers must enhance their frauddetection and prevention mechanisms.

Derek has worked in machine learning and advanced analytics for 20+ years, and he is a specialist in the development and application of predictive analytics for application frauddetection. What do you see as the biggest challenges for machine learning to fight application fraud.

Real-time FraudDetection The healthcare industry is, unfortunately, susceptible to fraudulent activities, and AI provides a robust defense mechanism. Predictive Analytics for Resource Optimization AI's predictive analytics capabilities extend beyond frauddetection.

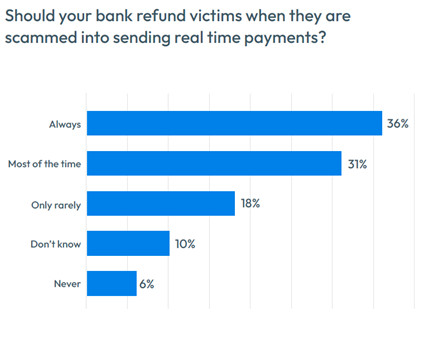

The challenge for banks is balancing the ease and convenience of RTP with fraudprevention for authorized push payment fraud (APP fraud) – without impacting customer experience. Better detection Overwhelmingly, customers want banks to improve their frauddetection capabilities to stop scams before they happen.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content