This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

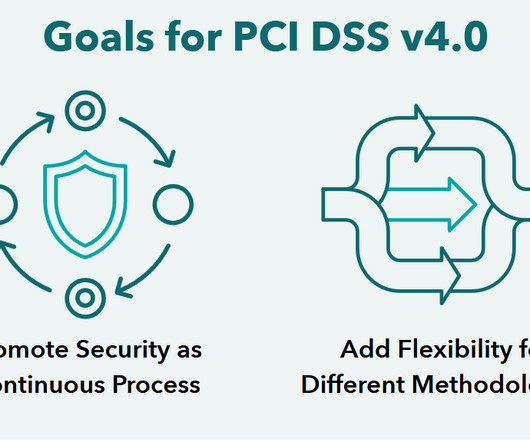

You can also check out the PCI at a glance infographic for a quick overview. For simplicity, I will just refer to PCIDSS standards as PCI for the rest of this article. What is PCI again? In the past, Ive written about how to achieve and maintain PCI compliance. Timeline PCI version 4.0

Two key technologies, Encryption and Tokenization, are at the forefront of safeguarding sensitive information. This blog will explore the fundamentals of encryption and tokenization, their differences, use cases in the banking and payment industries, as well as their benefits and limitations. What Is Encryption?

In this blog post, well help you understand the factors and features you need to consider to find the right payment gateway to suit your unique business needs. Ensure the gateway offers PCIDSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions.

In this blog, you’ll find a clear comparison of both solutions and a step-by-step approach to help you choose the right one for your business model. Look for features like transaction monitoring, biometric logins, and encrypted data. They sound similar, but they serve different purposes. Make sure your wallet follows KYC and AML rules.

Security compliance: ensure that all financial information is securely transmitted using tokenization and strong encryption across the transaction, and that the provider is in full compliance with security standards like PCIDSS. Your testing should check for security compliance, technical performance, and mobile responsiveness.

Set up automated alerts or subscribe to your gateway’s changelog or dev blog to stay informed about upcoming changes. A chosen Payment Gateway should comply with up-to-date security standards, like PCIDSS (Payment Card Industry Data Security Standard), data encryption, and tokenization, and have effective fraud prevention measures.

Its role is to encrypt and securely transfer your customers payment data to your payment processor. All the data transfer between the digital wallet and your payment terminal are encrypted and the system also uses tokenization to ensure iron-clad data security.

In our last discussion, we explored the evolution of Requirement 1 in the transition from PCIDSS v3.2.1 As we continue our exploration of the updated PCIDSS v4.0, With the impending retirement of PCIDSS v3.2.1 Modification to Requirement 2 from PCIDSS v3.2.1 to PCIDSS v4.0:

This is where the Payment Card Industry Data Security Standard (PCIDSS) comes into play, serving as a crucial framework for safeguarding sensitive information and protecting both businesses and consumers from the ever-present threat of cybercrime. Develop and document security policies and procedures tailored to business operations.

The Payment Card Industry Data Security Standard (PCIDSS) compliance 4.0 In this blog, we will understand PCIDSS compliance 4.0 What is PCIDSS Compliance for banks? What is PCIDSS Compliance for banks? The PCIDSS outlines 12 requirements mentioned below.

Welcome back to our ongoing series on the Payment Card Industry Data Security Standard (PCIDSS). Networks that store, process, or transmit cardholder data naturally fall within the PCIDSS scope and must be assessed accordingly. PCIDSS v3.2.1 PCIDSS v4.0

In the world of digital transactions, businesses handling payment cards must demonstrate their data security measures through the Payment Card Industry Self-Assessment Questionnaire (PCI SAQ). Completing the SAQ is a key step in the PCIDSS assessment process, followed by an Attestation of Compliance (AoC) to confirm accuracy.

One of the key factors making it possible is the industry’s joint efforts to enhance card transactions security, reflected in PCIDSS. In this article, we’re going to deep dive into PCIDSS meaning, history, requirements, procedures, and costs. What is PCIDSS? This way, PCIDSS 2.0

PCIDSS compliance, a global framework, mandates specific requirements and best practices for maintaining credit card data security. Enter the PCIDSS compliance. The PCI Security Standards Council (PCI SSC) has robust measures to protect cardholder information and prevent unauthorized access, fraud, and data breaches.

Enter the Payment Card Industry Data Security Standard (PCIDSS): a comprehensive framework that sets forth stringent rules and regulations to ensure the secure handling, processing, and transmission of cardholder information. As we approach the highly anticipated release of PCIDSS 4.0 a notable change is on the horizon.

The Payment Card Industry Data Security Standard (PCIDSS) plays a crucial role in protecting cardholder data for businesses that accept credit card payments. As a business owner or professional, it’s essential to understand the importance of PCI compliance and its requirements.

In this blog, we’ll break down their differences, how they interact, and which might be the best fit for your type of business. Key Functions of a Payment Gateway: Encrypts and securely transmits payment data. The payment gateway encrypts the information and forwards it to the payment processor. What is a Payment Gateway?

Acting as a virtual bridge, it encrypts sensitive data, such as credit card details, and ensures its secure transmission for authorization and processing. The next step is to assess the vendor’s approach to data protection, encryption, and fraud prevention by ensuring they comply with the necessary security standards, such as PCIDSS.

Security Recurly is PCI-DSS Level 1 compliant, the highest level of PCI-DSS compliance achievable. It encrypts data, utilizes industry guidelines on secure coding, and hosts data in facilities with high levels of physical and network security. Related Article: Subscription and Recurring Billing Options.

In this blog post, we will explore the essential features of loan origination systems that every lender must have. Here are the security protocols that should be in place for new-age lenders: Data Protection: Advanced encryption and multi-factor authentication safeguard borrower information, ensuring that sensitive data remains secure.

Step 4: Obtain PCI Certification Every business that transmits or handles payment information must comply with the Payment Card Industry’s Data Security Standards or PCIDSS. Typically, becoming PCI certified takes several months and no less than $50,000. As the last step in the PayFac journey, this one never truly ends.

Compliance with Industry Standards Your business should comply with industry bare minimums like Payment Card Industry Data Security Standard (PCIDSS). PCIDSS compliance sets industry requirements that safeguard payment card data using encryption, firewalls, and regular security audits. Use secure payment methods.

In this blog, we dive into the world of credit card reconciliation, the top softwares to solve this, key features to look for and challenges to overcome, and how solutions like Nanonets can help businesses. It employs encryption, access controls, and audit trails to protect sensitive financial information.

Look into their payment fraud prevention measures, including data encryption, anti-fraud filters, and adherence to PCIDSS. PayFac as a Service’s vendors may guide businesses in obtaining licenses and security certifications that ensure compliance with industry standards.

This blog will walk you through how your customers are using mobile credit card processing, how you can accept payments using mobile technology, what sorts of features to look for in a mobile solution, and some exciting statistics about the future of payment technology.

Most people assume they’re covered if they have antivirus software and SSL encryption, but thats only part of the picture. If a host doesnt mention industry standards like GDPR, PCIDSS, or SOC 2, that should raise eyebrows, especially if you’re handling sensitive user information like emails, passwords, or payment data.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content