This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Payment trends in Asia are changing how businesses and people transact from the digital-first economies of China and Singapore to the quickly changing markets of Indonesia and Vietnam. The shift toward digitised payments brings heightened concerns about cybersecurity, fraud, and regulatory compliance.

Not because it’s free, but because the payments were seamlessly integrated into the apps you’re using. In simple, layman’s terms, embedded finance is when financial services – like payments, loans, or insurance – are integrated directly into non-financial platforms. But it’s not just about BNPL.

But launching your eCommerce store is just half the equationaccepting payments efficiently and effectively is a whole different ball game. On the surface, it seems effortless, with customers only taking a few seconds to initiate and complete payments. Its the bridge between an eCommerce website, its customers, and the bank.

If youre like many people, its been a while since you last made a payment exclusively with cash. said theyve used electronic payment methods to make a transaction in the past three months. Credit and debit cards, digital wallets , ACH transfers , and other digital payments have become the norm.

We’ll also outline how to choose the best payment solutions for your unique business needs. Credit card merchant services are the systems, tools, and agreements that allow businesses to accept payments via credit and debit cards. Together, these tools form the foundation of your ability to process payments reliably and securely.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The evolution of open banking into open finance, examining regional regulatory approaches and adoption trends. Why is it important? What’s next?

As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms. The need for traditional banks to digitise has never been more apparent.

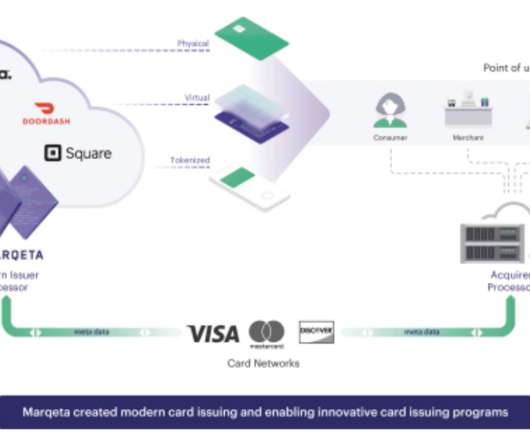

Marqeta is not just another payments company. By offering flexible, developer-friendly infrastructure, Marqeta empowers companies to launch, control, and manage customisable payment cards at scale. Marqeta set out to solve these problems by building a flexible API platform for issuing physical and virtual cards on demand.

Embedded finance is transforming industries by incorporating financial services directly into non-financial platforms. This integration allows businesses to offer banking-like services, enhancing customer experience and simplifying transactions. This shift is redefining traditional banking structures.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. Banking-as-a-Service (BaaS) describes the concept that enables non-bank platforms to access banking capabilities traditionally only offered by licensed banks.

Digital payments are transforming global financial systems, reshaping how individuals and businesses transact. In the fintech space, digital payments represent a major driver of innovation. By integratingpayment solutions directly into non-financial platforms, companies can offer seamless user experiences.

Airline credit cards, payment plans for costly items, and car rental insurance are forms of embedded finance that have been around for a while. Request Quote Understanding Embedded Finance Embedded finance is the seamless integration of financial services and digital banking into conventionally non-financial business services.

Modernising banking infrastructure The advent of CaaS has highlighted the need for financial institutions to modernise their banking infrastructure. “This technology supports digital wallets, open banking , and Cards-as-a-Service (CaaS).

Merchant-facing regulation: What merchants need to know in 2025 15 May 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The regulatory framework governing payments continues to expand in scope, with increasing implications for merchants operating in the UK and EU. Why is it important?

Marqeta , a cloud-based open API platform for modern card issuing and transaction processing, recently filed its S-1 in preparation for its shares to start trading publicly in June. Marqeta allows businesses to offer payment card products to customers without having to deal directly with a traditional bank. First name.

These companies, which represent countries such as Malaysia, the Philippines and South Korea, are tackling challenges in sectors such as lending, banking, and business finance, leveraging innovative business models and cutting-edge technologies to boost efficiency and enhance accessibility across the financial services industry.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. Continuing our focus on e-commerce and the checkout experience, we now turn our attention to the potential implications of embedded finance for traditional payment processors.

Banks in Asia-Pacific (APAC) are diversifying their offerings and embracing innovative digital strategies including super-app platforms, financial marketplaces and banking-as-a-service (BaaS) models. Indian bank and financial services company ICICI Bank is highlighted as one of the top BaaS providers in APAC.

It will also continue to invest in its comprehensive tech stack to power the end-to-end customer journeys across banking, insurance, and embedded commerce. Founded in 2008, Perfios is a B2B SaaS company serving the banking, financial services and insurance industry in 18 countries, empowering 1,000+ financial institutions.

Supporting the rapidly growing B2B e-commerce space has been an integral part of Allianz Trade ’s strategy for several years. When a buyer purchases online, the e-merchant receives immediate payment for the purchase, while the BNPL provider will chase the payment of the buyer.

Cards-as-a-Service allows for business to roll out their own payment card offerings such as debit cards and credit without the usual challenges that comes with it. Modernising banking infrastructure The advent of CaaS has highlighted the need for financial institutions to modernise their banking infrastructure.

In the rapidly evolving world of online gaming, having a reliable and secure payment gateway is crucial for both gamers and gaming businesses. A gaming payment gateway allows players to make payments seamlessly while ensuring that their financial information is protected. What is a Gaming Payment Gateway?

It enables quick product configuration, seamless third-party integrations (credit bureaus, payment gateways), and ensures regulatory compliance. This robust system also includes critical features such as Days Past Due (DPD) and Non-Performing Asset (NPA) tracking and provisioning.

Whether its personal loans, SME financing, auto loans, or BNPL (Buy Now, Pay Later), todays Loan Management Systems are built to handle the complexities of modern lending while ensuring efficiency, compliance, and seamless customer experiences. Improved customer satisfaction with flexible payment options. Billion by 2029!

Tackling the Fintech Threat: A Guide for Banks and Credit Unions. billion globally in 2021 – banks and credit unions are losing their status as the primary financial services providers to American consumers. Taking the FinTech Threat Seriously: What Should Banks Be Doing to Compete? banks collected $15.47 by Darryl Knopp.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. “These platforms, operating at the API layer, enable rapid and seamless integration of a wide array of financial services into e-commerce platforms. .

Aadhaar-enabled Payment Service (AePS) AePS, in India, enables individuals to conduct basic banking transactions like d eposits, withdrawals, balance inquiries, bill payments, etc. without requiring a traditional bank account or debit card. Unlike physical cash or bank deposits, CBDCs are purely electronic.

The regulatory landscape for fintechs and financial services companies operating in the European Union is expected to undergo significant changes this year, with new standards, guidelines, and rules governing payments, data privacy, digital assets, and more. One early issue will be compliance with the Instant Payments Regulation (IPR).

As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms. Its far easier to integrate into a point of sale or a web or an app-based offering than ever before.

Payments regulation roadmap: Q2 2025 14 April 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is the roadmap about? It provides a structured view of the regulatory developments set to shape the payments sector from Q2 2025 onwardsacross the UK, EU, and international markets. Why is it important?

BNPL solutions are a prime example of the intersection of shopping with financial services , effectively integrating financial firms into the consumers purchase journey. This is spurred on by the pressure to compete with non-bank players and address the shifting demands of enterprise retailers.

This dynamic industry thrives on innovation, leveraging technology to disrupt traditional banking models and set new standards for customer experience. Businesses and consumers alike are witnessing a seismic shift in how financial interactions are managed, from digital payments to sophisticated lending platforms.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content