This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

FXC Intelligence, a data platform specializing in the cross-border payment and e-commerce sectors, has released its annual selection of the world’s most promising cross-border payments companies in 2024. One of Singapore’s entries is Partior. million Series A funding round led by Sequoia Capital Southeast Asia.

Payment trends in Asia are changing how businesses and people transact from the digital-first economies of China and Singapore to the quickly changing markets of Indonesia and Vietnam. The shift toward digitised payments brings heightened concerns about cybersecurity, fraud, and regulatory compliance.

Not because it’s free, but because the payments were seamlessly integrated into the apps you’re using. In simple, layman’s terms, embedded finance is when financial services – like payments, loans, or insurance – are integrated directly into non-financial platforms. But it’s not just about BNPL.

one of Europe’s leading financial services providers, reveals digital wallets and Open Banking as pivotal forces set to transform the payments landscape in 2025. The findings reflect an industry-wide shift toward faster, more adaptable payment methods that meet consumer expectations in an increasingly digital economy.

The payment processing market in the United States has demonstrated robust growth, driven by rising consumer demand for digital payments, advancements in financial technology, and the expansion of e-commerce. The value chain in payment processing involves multiple parties that play specific roles in facilitating transactions.

Acumaticas electronic payment processing is a game-changer for businesses looking to enhance their sales and receivables processes. Integrating a payment gateway into Acumaticas system further streamlines online transactions, allowing businesses to accept payments securely and efficiently. What is Acumatica?

Morgan Payments is adding the Netherlands-based payments network iDEAL as a new payment method option at the checkout of its global commerce platform, in a move to expand its European e-commerce capabilities. Expansion plans The integration of iDEAL comes after J.P Expansion plans The integration of iDEAL comes after J.P

Trek partnered with Gr4vy to power an online-to-offline payment experience, offering consumers accurate inventory checks and simplified checkout. Gr4vy’s payment orchestration dynamically routes transactions, which reduces friction, increases authorization rates, and allows Trek to manage multiple merchants efficiently.

If youre like many people, its been a while since you last made a payment exclusively with cash. said theyve used electronic payment methods to make a transaction in the past three months. Credit and debit cards, digital wallets , ACH transfers , and other digital payments have become the norm.

Thanks to Way4s flexibility, Equity Bank Kenya was the first in the world to enable interoperability between the payment card network and a leading digital wallet ecosystem M-PESA. This can be an account opened in Way4 or in the integrated Core Banking System. Now we have more time and capacity to develop the payment business.

Telr , an award-winning leader in digital payments across MENA, has secured a Retail Payment Services License (RPS) by the Central Bank of the UAE, marking a transformative milestone in its mission to drive financial innovation and seamless digital transactions.

Cashflows, the platform that makes it easy for businesses to accept payments, today announces its new offering of SUNMI in-person payment terminals. The Android devices will be available to Cashflows partners and customers from today, enhancing the already robust in person payment offering.

Morgan Payments is expanding its European e-commerce capabilities, enabling our merchant clients to offer their customers a varied choice of payment options to suit their needs with the integration of iDEAL , the leading payments network in the Netherlands, as a payment method at checkout to our global Commerce platform.

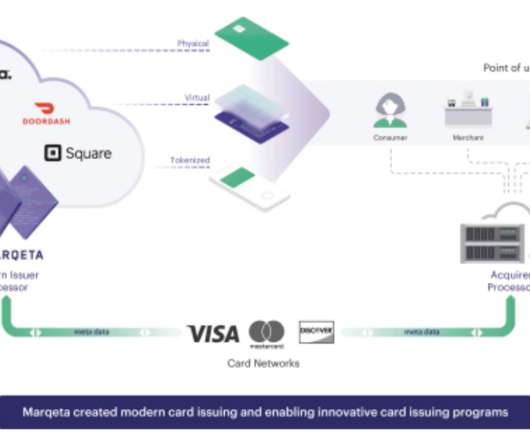

Marqeta is not just another payments company. By offering flexible, developer-friendly infrastructure, Marqeta empowers companies to launch, control, and manage customisable payment cards at scale. Marqeta set out to solve these problems by building a flexible API platform for issuing physical and virtual cards on demand.

From digital payments to decentralised finance (DeFi), these companies are solving real-world challenges like financial inclusion and cross-border transactions, while setting new global standards for innovation. billion payments Coda 2.5 billion payments, gamification Airwallex 5.5 billion insurtech Matrixport 1.05

Digital wallets, open banking and instant bank transfers are set to become the main forces transforming the payments landscape in the coming year, according to new research by payabl , the European financial service provider. As Europe’s SEPA Instant payment deadline approaches on 9 January 2025, industry readiness remains uncertain.

This integration allows businesses to offer banking-like services, enhancing customer experience and simplifying transactions. Consumers benefit from seamless access to payments, loans, and insurance, all within familiar digital environments. E-commerce platforms offer Buy Now, Pay Later (BNPL) options, improving purchasing power.

These member-driven organizations face competition from larger rivals in the banking industry, as well as new entrants from technology and retail who are leveraging embedded finance to offer a widening range of financial services, including payments and lending. Many businesses stand to gain from automating many internal processes.

What was once a manual chore is now an integrated part of modern money management. Bill payment is no longer a task, it is an experience. It is especially useful for recurring payments like utilities, mortgage instalments, and subscriptions. Alerts ahead of payment dates help prevent overdrafts and missed charges.

Cyberbank Core became an integral part of Galileo’s offering after SoFi’s acquisition of Technisys in 2022. We are thrilled that our new commercial payment services sponsor bank program is built on Galileo’s powerful tech platform,” said Anthony Noto, CEO of SoFi. Galileo is a subsidiary of SoFi. “We

As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms. That makes it hard to offer the API-first, real-time solutions that embedded finance demands.

As technological advancements continue to unfold, the payment landscape in the United States is poised for a transformative journey in 2024 and beyond. These key trends are set to redefine how consumers and businesses engage with payments, introducing innovation and unparalleled convenience.

Software as a service (SaaS) is a significant part of the global software market, making up one-third of it, and is making an impact across various industries, including payments. In response to these concerns, dedicated SaaS solutions , such as those offered by global payments software provider OpenWay, provide an alternative.

They have been successfully used in cross-border payments, remittances, and payroll for global workforces because they enable instant payouts at rates much cheaper than funds sent via traditional banking rails. BNPL With Klarna’s IPO taking place in 2025, we can expect to see interest in the BNPL space surge to new heights.

Plend , the dedicated B Corp personal lender in the UK, has launched an embedded credit API enabling partner organisations to offer their users affordable and sustainable credit directly. The API enables firms to integrate affordable and longer-term credit into a third-party customer journey or at point-of-sale.

A newly announced partnership between institutional payment orchestration platform Paydock and Australia’s Commonwealth Bank (CBA) will give merchants in Australia the ability to offer their customers a range of new payment options. Launched this spring, NameCheck is built to prevent scams and mistaken payments.

Wero , the new European payment solution developed by the European Payment Initiative (EPI) will be available to Computop customers from the moment it launches e-commerce payment in mid-2025. While payments between individuals will be available in 2024, online retailers will be able to offer wero payments by mid-2025.

credit card payments surpassed $10.6 Contactless payments continue their rapid adoption, projected to account for more than 60% of in-store purchases. From the cardholder to the merchant, and all the way through the financial institutions and payment processors, each participant brings something essential to the table.

Digital payments are transforming global financial systems, reshaping how individuals and businesses transact. In the fintech space, digital payments represent a major driver of innovation. By integratingpayment solutions directly into non-financial platforms, companies can offer seamless user experiences.

Marqeta said that Goldman Sachs “will leverage our modern card issuing platform” to introduce digital checking accounts to Marcus customers, according to a Marqeta blog post on Thursday (Jan. Silicon Valley’s Marqeta is a card-issuing platform that offers infrastructure and tools for building and operating payment solutions.

Slope powers the Slope Card which enables low-interest buy now, pay later (BNPL) loan options for its commercial customers. The Slope Card enables businesses to pay in-store or online with 30 or 60-day loan options, allowing for increased flexibility and choice in how they make payments and manage their finances.

Merchant-facing regulation: What merchants need to know in 2025 15 May 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The regulatory framework governing payments continues to expand in scope, with increasing implications for merchants operating in the UK and EU. Why is it important? for credit.

“By leveraging real-time customer data for personalised offerings, financial institutions can develop value-driven products integrated into customers’ daily routines, boosting satisfaction and cultivating stronger loyalty in the digital landscape,” explained Mike.

Marqeta , a cloud-based open API platform for modern card issuing and transaction processing, recently filed its S-1 in preparation for its shares to start trading publicly in June. Marqeta allows businesses to offer payment card products to customers without having to deal directly with a traditional bank. First name. Company Name.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. Continuing our focus on e-commerce and the checkout experience, we now turn our attention to the potential implications of embedded finance for traditional payment processors.

FXC Intelligence, a data platform specializing in the cross-border payment and e-commerce sectors, has released its annual selection of the world’s top cross-border payment companies, recognizing the leading publicly traded companies, startups and private companies operating in the space worldwide.

Paywatch, which operates across Malaysia, the Philippines, Indonesia, and South Korea, has recorded notable growth, processing over US$58 million in salaries to date and posting monthly disbursements of nearly US$8 million. The company expects to exceed US$120 million in disbursed salaries by the end of the year.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. “BaaS enables non-banking entities to provide financial solutions, such as payments and loans, seamlessly embedding them into their ecosystems.

Splitit’s groundbreaking solution, FI-PayLater, enables FIs to connect directly into Splitit, or connect via their existing card network, to drive incremental lending and fee income from BNPL use cases. Additionally, merchants experience increased sales driven by seamless, flexible payment options.

Payment initiation and account aggregation were frequently discussed, showing their potential to impact financial services. Standardising APIs and data-sharing practices was also flagged as crucial for further progress. Alongside the many opportunities, attendees also addressed several challenges.

Celerant Technology , a leader in retail software and eCommerce solutions, has announced additional integration functionalities with Sezzle. Sezzle is a ‘Certified B Corp’ BNPL solution that empowers consumers to shop with options to split payments over set periods of time. This opens up new revenue opportunities.

Payments are arguably the face of fintech. When you think about financial technology, it is easy to think about solutions which are making payments faster, easier and more accessible. We take a retrospective look and investigate which payment technologies have shaped the industry into its current iteration.

Source: twimbit analysis Banking-as-a-service (BaaS) The first trend outlined in the report is BaaS, a business model which involves the provision of banking products to non-bank third parties through application programming interfaces (APIs). India’s Paytm is one example of a successful super-app platform in APAC. trillion by then.

Supporting the rapidly growing B2B e-commerce space has been an integral part of Allianz Trade ’s strategy for several years. When a buyer purchases online, the e-merchant receives immediate payment for the purchase, while the BNPL provider will chase the payment of the buyer. We have a solution.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content