This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While consumer satisfaction with authentication differs across sectors, financial services topped other markets in a recent report. percent: Share of eCommerce consumers who were required to provide email addresses when signing up for an online account.

Many of these consumers are exploring digital banking for the first time, however, and are frustrated by customer onboarding pain points. Time-consumingauthentication methods, redundant application forms and sluggish processes can all drive away potential customers. Developments From Around the Digital-First Banking World.

Anti-fraud efforts can seem like word salad with exotic ingredients being tossed around: strong consumerauthentication ( SCA ), two-factor authentication (2FA), the second Payment Services Directive (PSD2) … you get the idea. Ask consumers what they want, however, and the acronyms vanish like a metaphor for things that vanish.

Five years ago, a merchant might have been able to rely on consumers being patient with a digital commerce experience that was less than perfectly smooth. This means authenticating a consumer has turned into something of a tricky and delicate process. To use it, customers have to download an app.

That’s the “unofficial motto” that Yehya Awad and his team have been kicking around for PulsePay , a heart rate-based method of online consumerauthentication that was the winner of the latest HackPSU that took place on April 9. The solution, he shares, was for the team to “right then and there buy Windows, download and install it.”.

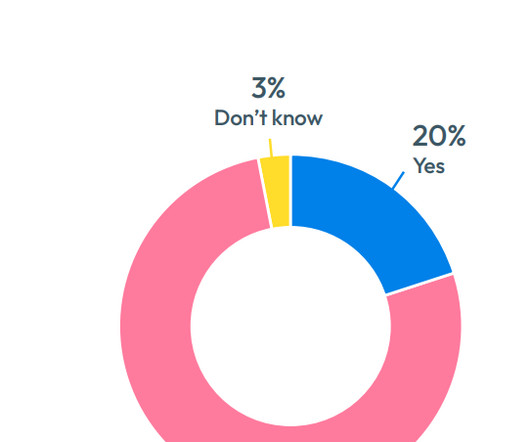

According to the Australian Competition and Consumer Commission’s Scamwatch , for example, more than 57,000 scams were reported in the first two months of 2023 alone. According to the 2023 FICO Global Scams Survey , 51% of consumers worldwide believe their friends or family members have been victims of similar scams.

According to FICO’s latest survey of consumers from 14 countries around the globe, 90% of all consumers have sent a real-time payment, and at least 95% of consumers have used real-time payments in India , Indonesia , the Philippines , and Brazil. Throughout the countries we surveyed, RTP usage shows no signs of slowing.

And card skimming is big business; the FBI estimates that “skimming costs financial institutions and consumers more than $1 billion each year.”. There are concrete steps that both banks and consumers can take to fight back against skimming fraud. Consumers can also look for things that seem “off” or “fishy” about a particular terminal.

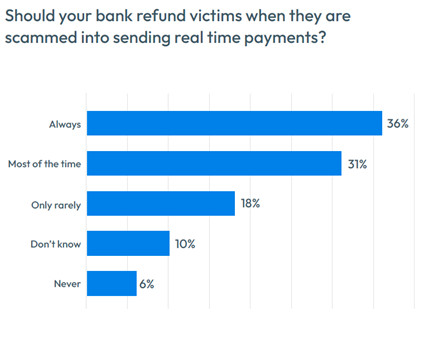

In the 2023 FICO Global Scams Survey , we asked consumers worldwide what they think banks could do better to combat scams and create a better customer experience for victims. In India and the Philippines , 70% or more of consumers would like to receive such warnings. This sentiment varies widely by region.

Step One: Correlate a consumer’s participation in various types of social networks (traditional, blog-based and professional) and their associated fraud risk. percent when a consumer participates in all three types. consumers who were identified using names, addresses, phone numbers and dates of birth (DOB).

Along with giving consumers the ability to purchase tickets online, the train service also made the shift to accepting digital tickets. This is really the key to a lot of my [decisions] for fraud management – the issuer will always have the greater relationship with, and the greater of the consumer behavior, than any merchant,” he explained.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content