This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

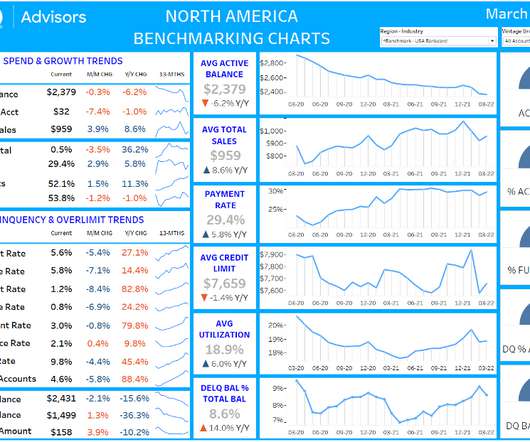

This Frankenstein approach to fraud cost US lenders an estimated $20 billion in 2020, according to the FederalReserve. These synthetic identities often use valid Social Security numbers belonging to children or individuals without credit histories, combined with fictitious names and addresses.

A new survey has revealed the steep plummet the consumer credit market took as the pandemic began, the FederalReserve Bank of New York reported. The FederalReserve Bank of New York’s Center for Microeconomic Data released results on Monday (Dec.

trillion, according to a CNBC report that cited the New York FederalReserve. However, credit card balances have dropped compared to before the coronavirus pandemic. That decrease in credit card balances comes even as the creditlimits have been increased by $34 billion, leaving $3 trillion available in credit card lines.

In the third quarter, banks tightened their loan standards to firms of any size and also saw weaker demand than usual, according to the FederalReserve ’s October 2020 Senior Loan Officer Opinion Survey on Bank Lending Practices.

April wasn’t a good month for consumer-credit use. According to the latest FederalReserve data , U.S. All in, consumer credit took a $68.8 billion hit in April, with revolving debts like credit cards taking the hardest hit — falling by a steep 64.9 consumer borrowing dropped 19.6

In today’s top payments news, ongoing security concerns have caused the FederalReserve to take a closer look at the Big Tech firms that serve the banking industry. Also, Goldman Sachs CEO David Solomon is denying claims that gender bias is apparent in the algorithm the bank uses to decide creditlimits for applicants.

credit card balances are approaching the $1 trillion figure, according to the FederalReserve. And credit card balances are on the rise as well. Credit card balances rose 3.4 At the same time, increasingly more nonprime consumers are getting access to card credit, usually at lower creditlimits.

During the pandemic, systemic financial assistance programs such as federal stimulus payments and the availability of lender-provided payment accommodations undoubtedly prevented and helped manage the dramatic increases in delinquencies and losses we witnessed in 2008-9. inflation, geopolitical instability, ongoing supply chain issues).

The US FederalReserve's new payment rail FedNow can shake up the landscape, offering significant time and cost savings. FedNow, by the FederalReserve, is a versatile payment rail catering to individual users and businesses. What is FedNow? This feature optimizes accuracy and expedites the payment process.

And consumers who have high “utilization ratios” measured by borrowings divided by creditlimits, will also have lower scores. For example, consumers who transfer credit-card debt to a personal loan but continue to rack up credit-card balances will likely experience a bigger drop in their credit scores,” the news outlet reported.

FederalReserve Chairman Alan Greenspan said Tuesday (Nov. Goldman Denies Discriminatory Apple Card Practices, Says It Will Reassess Limits. Goldman Sachs has promised to re-evaluate how creditlimits are determined for Apple Card users after being accused of gender discrimination. Former U.S.

Major net fractions of banks also tightened important terms on credit card loans, including creditlimits and minimum credit scores required,” the Fed noted. “Over the second quarter, major net shares of banks tightened lending standards on all categories of consumer loans.

Higher inflation is also leading to rising interest rates as the FederalReserve has already increased the base funding rate by 75 basis points this year and has said that they will continue to raise rates to tackle inflation. These changes to creditlimit management led to a 30.9%

Undoubtedly, systemic financial assistance programs such as federal stimulus payments and the availability of lender-provided payment accommodations have prevented the dramatic increases in delinquencies and losses we witnessed in 2008-9.

Tarullo, who has resigned from the FederalReserve Board of Governors — and who stated that forgetting those lessons would be “tragic.” . Those “restrictions and requirements” include creditlimits and resolution procedures, and yet compliance amid the complexity is a challenge.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content