This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The investment will help AKUVO expand its cloud-native collections and creditrisk solutions, enhancing efficiency and customer experience for banks, credit unions, and fintechs. Digital collections and creditrisk platform AKUVO landed a new round of funding today. .

This highlights the inherent risks lenders face. Therefore, financial institutions (FIs) need robust creditrisk management to minimise risk and boost returns and productivity. As per a report, as of March 31, 2023, 2,623 borrowers classified as wilful defaulters in India owe Rs 1,96,049 crore to the banks in India.

Carrington Labs, a leading provider of creditrisk analytics, has partnered with Oscilar, a leading provider of real-time decisioning infrastructure, to give lenders faster, easier access to advanced creditrisk solutions.

Of the seemingly inexhaustible uses of artificial intelligence (AI) in the financial sector, its applications around managing creditrisk and optimizing payment services are among the most promising. percent) and creditrisk underwriting units (33 percent). Decisions, Decisions. percent,” the latest AI Playbook states.

These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing creditrisk. This vital task is complicated even in normal times due to the multitude of financial risk factors in play at any given time. percent expect these systems to improve credit/portfolio risk.

Bloomberg customers will now be able to use the news site's terminal to look at Credit Benchmark 's creditrisk data, which comes from risk views of the world's largest financial institutions, according to a press release. Clients will also be able to use the data for an enterprise use case, the release stated.

Creditrisk continues to remain one of the areas of concern for a majority of traditional and new-age lenders. Additionally, new-age lenders often cater to underserved or high-risk segments, increasing the […] The post Understanding the Different Types of CreditRisk appeared first on Finezza Blog.

Managing creditrisk used to be a reactive process. Waiting until account holders fall behind to take action not only meant that customers’ credit scores would take a hit before their banks were alerted to a problem, but also that banks would lose the revenue from the scheduled payment.

Today in B2B, Bloomberg broadens its creditrisk data pool, and two ERP solutions secure B2B payments integrations. Bloomberg To Incorporate CreditRisk Data. The release stated firms have more often been looking for data to validate their own internal counterparty and creditrisk assessment.

CreditRisk. Core use cases that are getting a lot of traction, Dhala said, involve creditrisk. Any marginal improvement in terms of modeling or accuracy can result in significant gains because there’s a reduction in credit losses. AI can also help to spot creditrisk.

martini.ai, a leader in AI-driven creditrisk analysis, today introduced Financials Agent, an AI-powered tool that lets users upload financial documents such as 10-K filings and instantly generate a financial risk report.

How will these trends affect managing creditrisk? Delinquency rates on consumer loans and credit cards, which are currently being suppressed with government and bank support, are expected to increase rapidly. Unfortunately, many of them will not be able to return to their workplaces after pandemic.

However, traditional credit scoring models do not account for an individuals lack of credit history or other important parameters, including […] The post Behavioral Scoring: The Smart Approach to Line of CreditRisk Management appeared first on Finezza Blog.

However, traditional credit scoring models do not account for an individuals lack of credit history or other important parameters, including […] The post Behavioral Scoring: The Smart Approach to Line of CreditRisk Management appeared first on Finezza Blog.

British FinTech, Lemon, which specialises in SaaS finance for SMB’s has announced a strategic partnership with WiserFunding, a leader in alternative data for creditrisk assessment.

Nationwide Building Society , the UKs third-largest mortgage provider, has partnered with FICO , the analytics software company, to enhance its creditrisk and decisioning framework. Nationwide now uses the FICO Platform to process around 1.5

Broadstone, a leading independent pensions, employee benefits, investments and insurance consultancy, announces the acquisition of Vestigo Partners Limited (Vestigo), an experienced and dynamic analytics and creditrisk consultancy established in 2017.

Atto, a leading provider of creditrisk solutions using transactional data, is thrilled to announce a strategic partnership with FICO, a global analytics software leader, for the UK market.

In the dynamic world of financial services, the need for rapid and precise credit decisions has never been more crucial. This demand is driving a transformative shift towards leveraging Artificial Intelligence (AI) and automation to redefine credit and risk assessment strategies.

By merging credit spread data with essential corporate information, Agentic AI Company Research by martini.ai provides decision-makers including those in private credit with data-rich intelligence that highlights key trends, risks and opportunities. Rajiv Bhat, CEO of martini.ai With Agentic AI Company Research, martini.ai

CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

This collaboration aims to introduce AI-led creditrisk management to KBZ Bank, enhancing its ability to assess creditworthiness across retail and SME products with greater accuracy and efficiency. These advancements are expected to lower creditrisks and enhance operational efficiencies within the bank’s lending operations.

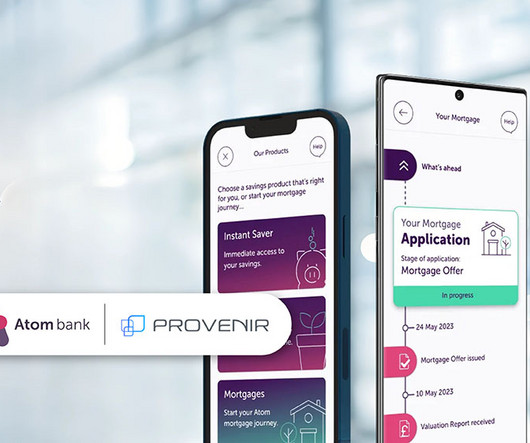

Atom Bank has chosen Provenir s AI decisioning platform to enhance its creditrisk decisioning and data orchestration capabilities across its consumer and business banking products. Founded in 2016 as the U.K.s

One of the few clear implications from the initial two months of the lockdown with the changes to consumer behavior and the uncertainty ahead is the imperative for organizations to regain clarity on creditrisk by obtaining a more complete picture of consumer creditworthiness, says LexisNexis Risk Solutions' Ankush Tewari.

AKUVO , a leading technology organization specializing in collections and creditrisk management, is proud to announce that Prosperity Bank , with $40 billion in total assets, has chosen AKUVO’s platform to streamline its collections processes.

In fintech, this means AI systems that dynamically manage creditrisk, automate trading decisions, and even preemptively block fraud, all without human intervention.

Given the roller coaster ride consumer finances have been on for the last 10 months, managing risk has become critical for financial institutions (FIs), both in terms of rising fraud counts and in terms of rising consumer delinquencies. Driving Actionable Intelligence In Real Time. Focusing On The Consumer And Building The AI.

The launch comes after a successful pilot program, Visa noted, with the focus of the chosen FinTechs ranging from small business creditrisk and buy now, pay later to merchant search and transaction compliance.

AI Also Helps Manage CreditRisk. For instance, Mastercard has been using AI to help its banking partners with creditrisk management, aiming to provide the right amount of credit to customers — and the smartest collections efforts — in today’s uncertain economic climate.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. They are one of our most sophisticated clients in terms of advanced analytics.”. by FICO.

Alternative lending companies are one of the strongest examples of how leveraging rich financial transaction data can be used to go beyond traditional creditrisk assessments, says Finsync's Eddie Davis.

By leveraging line-by-line transaction data, Recap’s creditrisk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

Auto lenders are incorporating artificial intelligence into their processes to improve customer service automation and credit decisioning while eyeing uses for underwriting.

The company maintained a prudent approach to creditrisk, with non-performing loans (over 90 days past due) at 2% of the loan portfolio. Featured image credit: Grab The post Grab’s Digibank Deposits Reach US$479M, Driven by Growth of Malaysia’s GXBank appeared first on Fintech Singapore.

And in banking, financial institutions can incorporate artificial intelligence into their consumer credit strategies at a time when a retroactive approach to creditrisk management has become less feasible amid COVID-19. All this, Today in Data. Data: $189B : Amount that U.S.

Even more significantly, our research shows that FIs are using AI with greater focus than they have in the past, with two areas emerging as key applications: payments fraud and creditrisk. Supervised systems like BRMS are simply not capable of responding to the dynamic, constantly shifting nature of these risks.

Even so, he acknowledges that banks have a reputation for being slow to change, as well as deep organizations that require many different stakeholders on board — including legal, compliance and business/creditrisk. De Vere added that even small, independent lenders present their own challenges to essentially the same set of problems.

By leveraging line-by-line transaction data, Recap’s creditrisk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

The news comes as during Hong Kong FinTech Week, FinTech firms have certain "key advantages" over traditional banks when it comes to building out a client base and cutting down on risk. Bloomberg to Incorporate CreditRisk Data.

NEW REPORT: The Banks’ How To Guide To Using AI To Manage CreditRisk. Banks have long turned to a familiar set of tools for managing creditrisk — late fees and other penalties. In the 2021 AI Business Plan Playbook For Banks, PYMNTS provides a six-step framework to help banks use AI to manage creditrisk.

Different than traditional credit bureau data, the use of trended data considers a historical view of data such as account balances for the previous 24+ months, giving lenders more insight into how individuals are managing their credit. . To learn more about FICO® Score 10 T please visit: www.fico.com/ficoscore10T. James Wehmann.

Ltd : Developed an ‘e-KYC’ solution to digitally onboard customers, using advanced technologies like artificial intelligence, machine learning, thumbprint and facial recognition for a streamlined digital KYC platform Soft Net Technology : Proposed a centralised loan application platform in response to pre- and post-Covid challenges.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content