This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

America Biometric Payments 2 Global, especially mobile-first markets Cash Payments 5 Emerging Markets, some developed regions Central Bank Digital Currencies (CBDCs) 1 Asia, Caribbean Credit Cards Overview : Credit cards allow consumers to make purchases on credit, paying later and often with interest.

According to the US Federal Reserve in 2022, general-purpose card payments reached $153.3 On top of that, 69% of Americans online in 2023 said they used digital payment methods to make a purchase. It ensures the secure transfer of funds from a customer to a merchant via their preferred payment method. trillion in value.

Customers now prefer to skip the slow, fraud-prone process of swiping or inserting magnetic stripe cards. They simply tap their credit card , mobile device, or smartwatch to pay. Card emulation. This technology turns any NFC-enabled smartphone, smartwatch, or wearable into a contactless credit or debitcard.

A merchant account is a business bank account that allows companies to accept payments, such as debit and credit card transactions, electronic fundstransfers (EFTs), and Automated Clearing House (ACH) payments. This data is verified for accuracy and then forwarded to the cardholder’s issuing bank.

Some banks have chosen to develop their own in-house payment processing systems, delivering end-to-end services directly to their customers. Other banks have formed strategic partnerships with third-party providers. From internal solutions to partnerships, we’ll provide an overview of each bank’s approach.

Finding the right payment gateway for your business in 2025 is a critical step toward ensuring seamless online transactions, boosting customer satisfaction, and securing your revenue streams. When a customer initiates a payment, the gateway securely transmits the information to the payment processor and the issuing bank for authorization.

General Terms Merchant A business that accepts credit or debitcard payments. Transaction A payment made using a card or digital wallet. Authorization An authorization is a request to the cardholders bank to approve a charge. Acquirer (Acquiring Bank) The bank or processor that works with the merchant.

Understanding ACH credit payments means understanding the way in which different types of ACH payments are processed in the US banking system. ACH credit payments differ from ACH debit payments and both are distinct from credit and debitcard payments. Customers can initiate an ACH credit payment online or by phone.

This constantly updated article tracks the biggest and most important new products released worldwide by financial technology companies, along with banks, credit unions, investment advisors, insurance companies, credit card issuers and payment providers. Weve been obsessed with new fintech products since before the term was invented.

We can hail a ride from a mobile app, and our transactions for all sorts of goods and services can be easily paid for from our phones. There are a wide variety of digital payment types, such as mobile POS systems, contactless payments, and digital wallets. All you need to use a digital wallet is a smartphone.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

What is Electronic FundsTransfer (EFT)? If you've ever used onlinebanking, chances are you've used Electronic FundsTransfer, or EFT. EFT stands for Electronic FundsTransfer. Checking accounts allow you to write checks and use a debitcard to make purchases.

What is Electronic FundsTransfer (EFT)? If you've ever used onlinebanking, chances are you've used Electronic FundsTransfer, or EFT. EFT stands for Electronic FundsTransfer. Checking accounts allow you to write checks and use a debitcard to make purchases.

EFT payments are becoming increasingly popular as more and more people conduct their financial affairs online. An Electronic FundsTransfer (EFT) is the movement of money electronically from one account to another, either within a single financial institution or across multiple institutions, through computer-based systems.

Debitcards are pivotal to a bank’s digital payment mix. In India, the number of debitcards in circulation is projected to witness a steady increase of 84.6 million cards by 2028. The total number of debitcards is anticipated to reach an impressive 1 billion*.

Debitcards have become an indispensable part of our financial lives, with the majority of American adults, spanning all demographics, now possessing at least one debitcard. Every merchant should prioritize taking the time to understand debitcard processing to streamline operations and enhance customer satisfaction.

With the introduction of electronic fundstransfers (EFTs), gone are the days of paper checks and manual money handling. What is an electronic fundstransfer (EFT)? An electronic fundstransfer , or EFT, is a core pillar of modern banking and transactions. Why are EFTs important?

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobile payments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan. Why Uzbekistan?

In this 2024 report, we’ll explore how payment methods have evolved in the Canadian market, focusing particularly on the shift towards digital, contactless payments , and mobile along with other 2024 trends. Digital banks, sometimes called Neobanks, push consumers into digital banking and digital payments.

They’re also big fans of mobile wallets. billion mobile wallet users worldwide, with Gen Z and Millennials leading the pack. When it comes to credit cards, they’re using them smartly. They still use credit cards too, for about 26% of their transactions. Cash usage dips to around 13%.

Barely a couple of decades ago, there were just a few options available for transferring money from one account to another, but the rise of internet banking has given way to a bunch of different services with different names, processes, fees, and waiting times. What Exactly is an EFT Transfer?

The Continued Surge of Contactless Payments Contactless payments , facilitated by tap-to-pay cards, mobile wallets , and wearable devices, are set to maintain their upward trajectory. In 2024, they are anticipated to be used for over 40% of all online transactions in the U.S.

The world of Electronic FundsTransfer (EFT) payments is vast, spanning just about every payment method you can think of. TL;DR An Electronic FundsTransfer is an umbrella term for payments that are conducted electronically—essentially, any payment method except for cash and paper checks. Easy to use.

A merchant account acts as a pathway between your business, your customers, and the issuer and acquiring banks to process electronic transactions like credit cards. A merchant account refers to a business bank account that allows businesses to accept electronic payments for goods and services.

Whether you run a small online store or a major brand, accepting electronic payments is a must for all businesses. According to Onbe, 73% of consumers prefer using digital payments like cards and payment apps. In order to receive card-based payments, businesses need to have a merchant account.

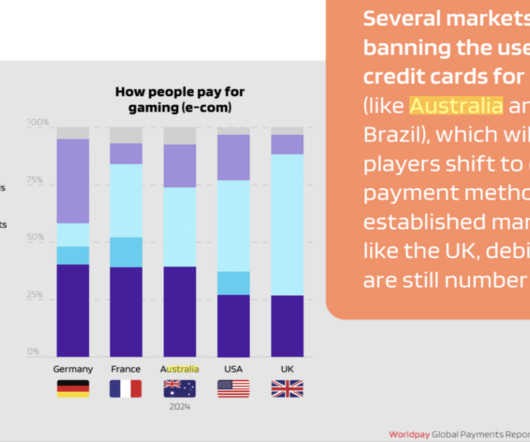

Lets take a closer look at the landscape of online gaming in Australia? Online gaming in Australia has experienced significant growth. The online gaming industry in Australia has evolved into a dynamic ecosystem, driven by technological advancements and changing consumer behaviors. billion and is expected to double by 2033.

In the world of eCommerce and online payments, one of the crucial decisions that merchants face is selecting the right online payment gateway. What is a Payment Gateway As online merchants rely on a technology platform to ensure the seamless functioning of e-commerce operations, and this essential tool is known as a payment gateway.

A payment gateway is a must-have for online stores. And the best way for online businesses to start accepting payments is with a payment gateway. TL;DR A payment gateway is a solution that securely reads and transfers a customer’s payment information to a merchant’s bank account—both for online and in-person transactions.

This process is vital for businesses, as it enables them to accept payments through various methods, including credit and debitcards, electronic banktransfers ( EFT/ACH ), and digital wallets. It then sends an approval or denial response back through the card network to the payment processor. trillion by 2027.

They are an additional type of payment you can take along with debitcard transactions and credit card payments from card networks like Mastercard, Visa, American Express, and Discover. Or mobile wallet payment solutions like Google Pay and Apple Pay. TL:DR ACH Payments are essentially digital check payments.

Aadhaar-enabled Payment Service (AePS) AePS, in India, enables individuals to conduct basic banking transactions like d eposits, withdrawals, balance inquiries, bill payments, etc. without requiring a traditional bank account or debitcard. Unlike physical cash or bank deposits, CBDCs are purely electronic.

The cards are largely associated with the 10 million or so unbanked families in the U.S. as one of their primary tools of financial management — since prepaid cards can be used in ways essentially analogous to debitcards for payments, funds storage, cash-outs at ATMs or receipt of salary.

Wire transfers and electronic fundstransfers have been staples of financial transactions for decades, but various electronic transfer methods have emerged with the innovation in banking technology. What is an electronic fundstransfer (EFT)?

Online and contactless adoption multiplied, and digital payments rose. Consumers are increasingly gravitating towards quick and convenient payment methods such as contactless payments and mobile wallets when transacting with businesses. Between 2019 and 2020, the number of U.S. What are the Most Common B2B Payment Methods?

The most ubiquitous form is credit and debitcards, seamlessly accepted through various channels – be it in-person via mobilecard readers, virtual terminals, or securely online through payment gateways. This is up significantly compared to 2016 when 65% of HVAC companies accepted credit cards.

Driven by shifting consumer preferences and innovative fintech solutions, online shopping has never been more convenient and accessible. Australias New Payment Platform (NPP) The New Payments Platform (NPP ) is Australias real-time payment system, launched in 2018 to enable fast, 24/7 banktransfers.

Acquirers: The Foundation of Payment Networks At the heart of payment processing, acquirers, often referred to as acquiring banks , play a foundational role. Not only do acquirers authorize and process credit and debitcard transactions, but they also ensure the seamless transfer of funds between merchants and consumers.

When The Clearing House (TCH) unveiled the Real-Time Payments (RTP) system in 2017, it propelled swifter payments and brought about the next generation of fundtransfers. Most modern bills (73 percent) are paid directly to the biller, according to recent research , while the rest are reconciled by bank bill pay (BBP).

Visa, and more specifically Visa Direct, made two great pushes for outward expansion, while Apple is working to push both its new card and its new line of phones, possibly in reaction to its China slowdown. Then there was the pushback of the week, care of PayPal, which is looking for better defined mobile wallet rules from the CFPB.

For example, you could add a convenience fee if your standard payment method is cash or check, but a customer wants to pay over the phone or online with a credit card. A convenience fee is applied for using a non-standard payment method, while a surcharge is an additional fee added specifically for credit card transactions.

In simplest terms, payment terminals are the machines used to pay for things using credit or debitcards when you make a purchase in-person. When you buy something at a store and insert your chip card into a machine that uses EMV technology, that’s a payment terminal. Learn More What are payment terminals?

Your business can benefit from payment links since they don’t involve technical requirements for the payer and offer versatile payment links such as credit cards, electronic payments, and mobile payment options. These links also provide safer and faster fundtransfers and work well with various payment service providers.

Card-based transactions in China — where UnionPay holds a state-enforced monopoly on all card-based payments — are up 35 percent over this time a year ago. And though UnionPay was once among the first to develop mobile payment QR code technology, it has largely ceded that ground to China’s two dominant mobile app payment players.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content