This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? X (formerly Twitter) has made its first decisive step into fintech, announcing a partnership with Visa to power its ambitious new digital wallet, X Wallet.

In the past decade, digital wallet adoption in Singapore has surged, overtaking long-standing payment methods such as credit cards and cash as the preferred payment method. When shopping online, survey respondents cited Apple Pay (24%), PayPal (20%), ShopeePay (18%) and GrabPay (18%) as their top digital wallets.

From digitalpayments to decentralised finance (DeFi), these companies are solving real-world challenges like financial inclusion and cross-border transactions, while setting new global standards for innovation. Coda aims to make digital transactions simple, inclusive, and accessible to everyone. Coda Valuation: $2.5

The payment processing market in the United States has demonstrated robust growth, driven by rising consumer demand for digitalpayments, advancements in financial technology, and the expansion of e-commerce. The value chain in payment processing involves multiple parties that play specific roles in facilitating transactions.

From innovative lending platforms to advanced payment processing, fintech is enabling them to access growth opportunities and thrive in today’s competitive markets. Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Fintech companies see this gap as an opportunity to innovate.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactless payments continues to grow. In fact, ResearchAndMarkets.com forecasts the global credit card payment market to grow to $762.16

According to the US Federal Reserve in 2022, general-purpose card payments reached $153.3 On top of that, 69% of Americans online in 2023 said they used digitalpayment methods to make a purchase. It ensures the secure transfer of funds from a customer to a merchant via their preferred payment method.

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) And how can you find a reliable payment processing solution for your business?

The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobilePOSpayments, and BNPL services. Looking to 2025, mobilepayments and digital commerce are projected to exceed 10 trillion, with open banking and real-time payments leading growth.

said theyve used electronic payment methods to make a transaction in the past three months. Credit and debit cards, digital wallets , ACH transfers , and other digitalpayments have become the norm. To accept electronic payment methods fast and securely, you need a payment gateway.

A fundamental element that every business leader should be well-versed in is the merchant account — a critical service that facilitates electronic payments. As digitalpayments continue to grow in popularity, a frictionless payment processing system is vital. What is a merchant account? How do merchant accounts work?

A centralised omnichannel point-of-sale (POS) system emerged as the most common Unified Commerce strategy, with 41% of merchants currently using one to streamline payments and customer experience. Of these, over 40% reported that it resulted in higher customer spend.

Driven by mobile adoption, digital identity initiatives, and regulatory reforms, the Indian fintech ecosystem is reshaping financial services not only at home but increasingly abroad. This article highlights the top 10 Indian fintechs making significant waves across payments, lending, wealth management , and embedded finance.

8 common features of enterprise merchant services Merchant accounts are specific types of bank accounts that allow enterprise merchants to accept credit, debit, Automated Clearing House (ACH)/eCheck, and other payments. This account holds funds from sales until they’re deposited into a business’s primary bank account.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

Credit card processing fees are comprised of several fees, such as: Interchange fees: Interchange fees are paid to the card-issuing bank and typically consist of a percentage of the total transaction amount plus a small, fixed charge. Review your average sales volumes and whether you primarily process in-person or online transactions.

In Pakistan, and elsewhere, the stars are aligning for greater use of digitalbanking and payments to improve financial inclusion. A widespread embrace of mobile devices, said Wain, “made it possible for new players in that ecosystem to build and deliver services on top of the mobile telecom infrastructure.

We’re still navigating the pandemic — which means doing what we used to do offline, increasingly, through digital means. As PYMNTS found in a recent consumer study, 40 percent of individuals are doing more of their daily retail and transactions online, partly because, well, there’s no other way to do it. As Good noted, four in 10 U.S.

For financial institutions (FIs) and enterprises that seek to pivot to meet the growing demand for digitalpayments, observing and reacting to shifts in how different generations prefer to pay will be critical during the pandemic and beyond, according to Royal Cole , executive vice president, FI payment solutions at FIS.

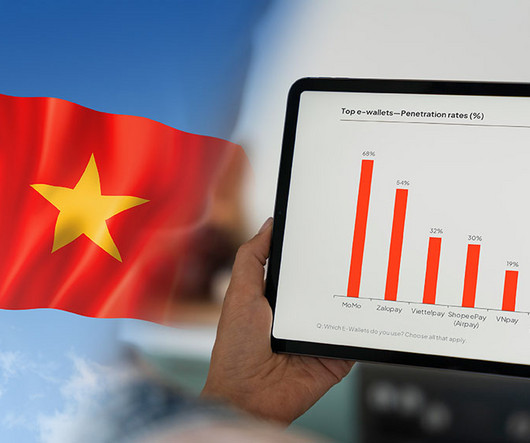

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

A new report by Reputa, an online reputation monitoring system provided by Viettel, Vietnam’s state-owned telecommunications giant, offers an analysis of the country’s fintech sector and provides rankings of the most reputable fintech companies in Vietnam based on their online reputation and reach.

Fast forward to now where much has changed, and research anticipates contactless mobilepayments to exceed one billion users globally by 2024. Customers can pay with their watch or phone just by tapping it on a card reader, and businesses can host an entire POS system on a mobile phone.

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobilepayments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan.

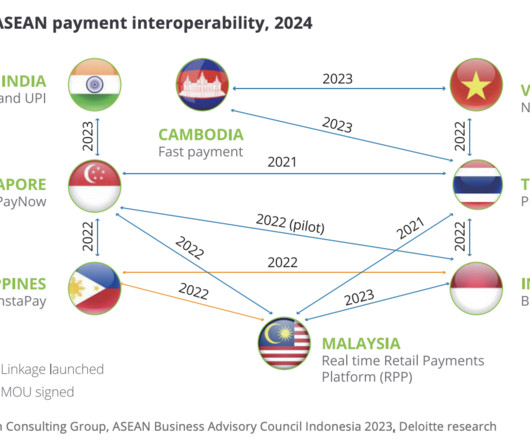

A new report by Deloitte delves into the latest developments in the cross-border payment sector in Asia-Pacific (APAC), identifying four major trends reshaping the landscape and offering significant opportunities for merchants. The digitalpayment revolution The first trend outlined in the report is the digitalpayment revolution.

Obviously, consumers are looking to buy everyday goods online as opposed to going inside a store, [and] we effectively have seen two to three years of eCommerce growth in a matter of three or four months. The first phase of responding to COVID-19 was largely an all-hands-on-deck drive toward digitization, Abele said.

Piatt noted that FIs have come up with a variety of solutions, like beefing up call centers or creating drive-thru-only banking services. And FIs want to help consumers spend money in the places where they want to spend money — which, in the wake of COVID-19 — is largely online. Recreating The Card For A Digital-First World .

To that end, the banking giant J.P. Morgan is focused on enabling payments for the millions of small businesses that are the lifeblood of Main Streets across the U.S. – Morgan is bringing payments to the point of sale (POS), with an eye on making inroads into a landscape dominated by firms such as PayPal and Square.

Thankfully, with mobilepayments from Stax , you can quickly accept and process payments from your customers. Learn all about mobilepayments and why you may want to consider joining the Stax family to streamline payments and boost your small business’ productivity.

The potential union would unite Ovo , Indonesia’s giant digitalpayment service that is backed by Singapore’s ride-hailing giant Grab Holdings , along with Dana, Indonesia’s digital wallet platform, an Alibaba Group Holding Ltd. Ovo and Gojek have been battling for top payments spot for the last two years, the report said.

By the late 20th century, these inefficiencies prompted the development of alternative payment systems. The foundation for modern digitalpayment solutions began to take shape with the advent of credit cards. The Emergence of Card Payments The introduction of credit cards in the mid-20th century marked a pivotal moment.

It’s a stalemate, Movile CEO Patrick Hruby told Karen Webster, that can likely be broken if Facebook agrees to integrate its service with the central bank-backed instant payments platform PIX, slated for rollout in October. “In The changes that are happening in Brazil and across the region, he noted, aren’t exactly new.

Commissioned by Discover® Financial Services’ PULSE debit network and conducted by Banking & Payments Group , the study gauged insights from large banks, credit unions and community banks. point-of-sale (POS) transactions, two account-to-account transfers, and 1.9 ATM transactions.

Customers expect unified retail experiences as they shop between in-store and online. Around The MobilePoint-Of-Sale World. The scarcity of cash in Zimbabwe is making it difficult for consumers to complete basic purchases, driving a need for digitalpayment solutions. Read the full feature in the Tracker.

The first quarter of 2020 should have been business as usual — especially for the payments processors and financial services technology companies — the firms that keep commerce humming across offline and online channels. Merchants, too, enjoyed the tailwinds of a strong economy and sanguine consumer mindset. Setting The Stage.

A payment gateway is a must-have for online stores. In fact, research from 2023 shows that 69% of Americans said they’ve used a digitalpayment method in the past 3 months when making a purchase. And the best way for online businesses to start accepting payments is with a payment gateway.

FIS Global reports that in Norway, Sweden, and other Scandinavian countries, more than 90% of transactions processed at point-of-sale (POS) in 2023 were cashless. Further, Statista projects that the value of global digital transactions will exceed $11 trillion in 2024. What Is an ISV vs PayFac?

During the 2020s, almost all businesses will have been looking at b2b payments processing solutions to meet changing consumer needs. Online and contactless adoption multiplied, and digitalpayments rose. consumers using two or more types of digitalpayment methods increased by 8%.

Whether you run a small online store or a major brand, accepting electronic payments is a must for all businesses. According to Onbe, 73% of consumers prefer using digitalpayments like cards and payment apps. But to seamlessly receive these payments as a merchant, you’ll need merchant processing services.

The way people pay and get paid has changed more in the past five years than in the last 50, and the latest innovations will bring new payment experiences to transform commerce and money movement spanning eCommerce, face-to-face in-store shopping, and seamless money transfers.

Linking buyers and sellers across online platforms? Supply and demand get a bit balanced in the digital realm. To that end, Jess Turner , executive vice president of products and innovation for Mastercard , and Radha Suvarna , head of digitalpayments and lending for the Citi U.S. No problem.

For a merchant to accept credit cards, they need to pay both credit card processing fees to the banks involved and for the soft and hardware required to process cards. Typically, the merchant’s payment processing software will build the credit card processing rates into their fee. Card Network (e.g., Card Network (e.g.,

We're focusing on the ability for consumers to use their rewards points at over 60 million merchants around the world, whether that’s online, in-store or via contactless using a major wallet such as Apple Pay or PayPal – and really bringing [loyalty redemption] to life.”. Points as Cash and the Future of Loyalty. My Rewards 2.0

PayPal has inked a deal with point-of-sale (POS) company ebizmarts to help retailers offer both POS and digitalpayments. According to news from MobilePayments Today , under the partnership, PayPal’s mobile card product will be combined with ebizmart’s mobile app Magento.

Coverage includes SnapPay teaming up with Alipay to bring the digitalpayment method to a supermarket company in Canada. SnapPay teamed up with Alipay to bring the digitalpayment method to locations of Canadian Chinese grocery store chain FoodyMart, according to an announcement from the companies. or Canadian dollars.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content