This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Singapore is enhancing its anti-moneylaundering (AML) framework with new recommendations from the Inter-Ministerial Committee (IMC). This comes after a review sparked by the high-profile moneylaundering case in August 2023, in which more than S$3 billion worth of assets were seized.

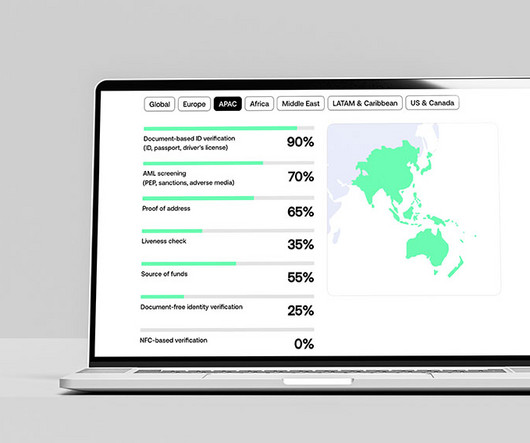

The report, based on Sumsubs internal identity verification and user activity data from 2023 and 2024, along with a survey of over 300 companies across the crypto, banking, payments, and e-commerce sectors, reveals that APAC was the only region to record a decline in crypto fraud in 2024, with fraud rates dropping from 2.6%

A recent comprehensive report by Chainalysis sheds light on the intricate world of crypto-related moneylaundering. The far-reaching study encompasses both crypto-native and non-crypto native methods, as well as strategies for prevention. Usage of mixers peaked in 2022, with over US$1.5

According to a UN report, moneylaundering activities of about $1.6 The US, therefore, requires financial institutions as well as financial services firms to have anti-moneylaundering (or AML) compliance programs in place. Non-compliance can have major implications. of global GDP. Let’s get started.

Buna’s compliance program integrates rigorous anti-moneylaundering (AML), counter-terrorism financing (CTF), and sanctions screening protocols both before and after settlement, offering real-time monitoring and thorough duediligence to safeguard financial transactions.

It highlights new corporate responsibilities, significant penalties for non-compliance, and the businesses need to implement strong fraud prevention measures to protect their financial and reputational standing. Duediligence : Ensuring employees and third parties adhere to anti-fraud policies. Why is it important?

Moneylaundering is a major threat in the United Kingdom , one some watchdogs say is not being taken seriously enough. The National Crime Agency (NCA) estimates that hundreds of billions of pounds are laundered through U.K. banks and their subsidiaries every year. and the philosophies that foster it. .

By thoroughly assessing merchants, processors can: Reduce fraud and chargebacks by identifying potentially fraudulent or non-compliant merchants before onboarding them. Ensure regulatory compliance by adhering to anti-moneylaundering (AML) laws and Know Your Customer (KYC) requirements.

12) that it will now allow corporates to join its KYC Registry in an effort to facilitate the sharing of data between companies and their banks. ” Indeed, researchers have found evidence that companies are struggling to manage the growing weight of KYC, anti-moneylaundering (AML) and other financial regulatory compliance demands. .”

Buna’s compliance program integrates rigorous Anti-MoneyLaundering (AML), Counter-Terrorism Financing (CTF), and sanctions screening protocols both before and after settlement, offering real-time monitoring and thorough duediligence to safeguard financial transactions.

In other news, European FinTech SIA is partnering with WizKey to create a platform to allow credit negotiations on blockchain for banks, financial operators and funds, according to a press release. Diokno, Philippines’ Central Bank (BSP) governor in the release.

In May, Fintech Global released its inaugural FinCrimeTech50 list, recognizing the world’s leading technology companies fighting moneylaundering, fraud and financial crime. It includes a suite of financial and non-financial crime risk domains with hundreds of risk indicators and controls, though users can also integrate their own.

In financial fraud, the breaches come when bank standards are lax. Australian bank Westpac Banking Corp. In an interview with Karen Webster, Stephen Taylor , general manager of anti-moneylaundering at NICE Actimize , said the issues spotlighted by the Westpac CEO are hardly confined to that FI alone.

The recent £29 million fine imposed on Starling Bank by the Financial Conduct Authority (FCA) for financial crime failings offers important lessons for businesses in the e-money and payments industry. For more details, you can read the FCA’s Final Notice on Starling Bank’s failings here.

The European Banking Authority (EBA) on 16th January extended its Guidelines on moneylaundering (ML) and terrorist financing (TF) risk factors to crypto-asset service providers (CASPs). Therefore, it is important that CASPs know about these risks and put in place measures that effectively mitigate them.

Australian banking giant Westpac has agreed to a massive fine of $920 million ($1.3 million in Australian dollars) in a bid to put a money-laundering scandal behind it. 24), noting that Westpac had violated anti-moneylaundering (AML) and terrorism financing regulations more than 23 million times.

Not only must PayFacs safeguard themselves and their clients against potential threats like fraud or cybersecurity breaches but also ensure PCI compliance , customer duediligence, and adherence to card regulations. However, several complex types of risks come along with this. This requires sound underwriting policies and procedures.

BaaS provider Synapse filed for Chapter 11 bankruptcy in April, leaving its clients, including Evolve Bank & Trust and multiple others, unable to verify and manage funds. In all, around $85 million in consumer funds are missing due to discrepancies in Synapse’s records.

Indicators for enhanced duediligence The NCA, in collaboration with other government agencies, has outlined red flags to assist businesses in identifying potential illicit activities. Purchases under a letter of credit consigned to the issuing bank: Not to the actual end user, with supporting documents not listing the actual end-user.

A partnership aimed at helping banks, payment providers and fintechs meet the ever stronger regulatory demands while reducing effort and expense. . We serve corporates, insurance companies, and banks – be it a retail, private, wealth management, automotive or telecom bank, tier 1 or tier 3 bank. What do you do?

The country’s financial and non-financial regulated institutions will be able to use the FICO ® TONBELLER™ Siron ™ KYC module to perform duediligence processes, in compliance with local laws and regulations, through APC Intelidat’s powerful technology infrastructure.

Thorough duediligence, technology, and adherence to regulatory guidelines are essential in a PayFac’s risk management strategy. You need thorough duediligence, technology, and adherence to regulatory guidelines in your risk management strategy. The duediligence doesn’t stop at onboarding.

For many banks, KYC — Know Your Customer — means asking them how they intend to use a product, where the funds are coming from for their new account, etc. At the same time, the bank will check the customer against sanction lists, PEP (politically exposed persons) lists, and so forth. Should banks care? It’s not enough.

Regulator sets out its expectations for banks looking to provide digital asset custody services, and sell and distribute tokenised products. All of this recent guidance aims to deliver more certainty for banks and securities firms seeking to capitalise on developments in digital assets and tokenisation. loyalty points, in-game assets).

The move aims to protect against financial crime and loss, particularly in digital fraud, and includes broadening DPT service definitions and enhancing Anti-MoneyLaundering (AML) protocols such as Customer DueDiligence and transaction monitoring. Sparrow Tech Private offers digital asset products and solutions.

These methods may include bank transfers, checks, PayPal, digital wallets, and more, depending on the options provided by the affiliate program or merchant. This lack of control can lead to affiliates engaging in unethical or non-compliant marketing activities. Non-compliance can result in fines and legal action.

As banks and payments companies endeavor to meet anti-moneylaundering (AML) regulations to avoid hefty fines for non-compliance, easily identifying customers in the digital channel becomes paramount to their success. Some “old school” methods that worked in the past aren’t working anymore. In the U.S.

In June 2023, Hong Kong introduced a comprehensive regime to regulate VA service providers operating a virtual asset trading platform (VATP) (see this Latham blog post ) through an amendment to the Anti-MoneyLaundering and Counter-Terrorist Financing Ordinance (AMLO). Certain regulated entities exempted. Powers of the CED.

The Discussion Paper received responses from a wide variety of stakeholders, including industry bodies, crypto native firms, and banks, and the HKMA announced in the Discussion Conclusions that it would propose a risk-based regulatory framework for fiat-referencing stablecoins (FRS), with further consultation in due course.

Coin Listing Policy Requirements Under the Proposed Guidance, a VCE need not seek prior DFS approval to list a coin that does not appear on DFS’s Greenlist via self-certification, so long as: DFS has approved the VCE’s coin-listing policy which meets DFS standards for self-certification of the listing of non-Greenlisted coins.

A staggering 67% of global banks are experiencing client abandonment during the KYC onboarding process, marking a significant jump from 48% in 2023, according to new research by regtech firm Fenergo. Global financial penalties for non-compliance with anti-moneylaundering (AML) regulations cost financial institutions US$6.6

In a survey of 644 financial services professionals, WWF and Themis found that over 60 per cent said that a land conversion risk policy was either non-existent (45.7 This creates a risk if bad actors initiate illicit activity after onboarding with a bank. per cent) or not yet developed or in place (18.6 per cent) in their firm.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content