This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Describe how Almond FinTech ensures the affordability of cross-border transactions for end-users. Almond’s SOE puts end-users at the core of our mission. What innovations make Almond FinTech’s platform unique from other cross-border payment solutions in the market? Let’s dive in.

This integration provides users with an unprecedented payment experience, allowing faster and safer transactions while redefining how Colombians shop. In a country where mobile payment growth is projected at 22% annually, adopting solutions like Google Pay is essential to meet market demand. billion by 2025, compared to $59.74

Share Energy brings an innovative, customer-first approach to the energy market, with its attractive profit-share revenue model poised to drive rapid, large-scale customer growth. The partnership with PayPoint ensures that robust payment services and infrastructure are in place to support this anticipated demand.

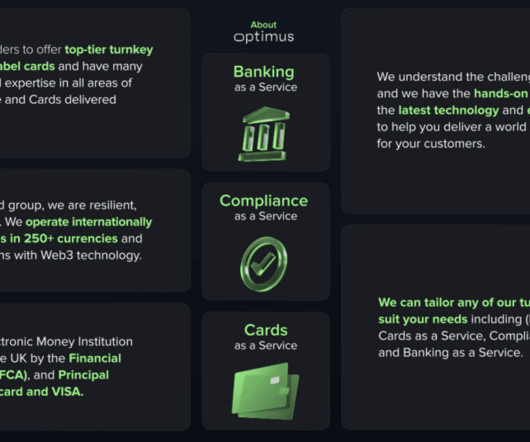

Virtual account and IBAN issuance: Recognising the growing demand for digital payment solutions, Optimus provides businesses with the tools to create and manage virtual accounts for their customers. Optimus’s solution enables corporate and retail end-users to send payments utilising local banking rails.

Why do some embedded analytics projects succeed while others fail? We surveyed 500+ application teams embedding analytics to find out which analytics features actually move the needle. Read the 6th annual State of Embedded Analytics Report to discover new best practices. Brought to you by Logi Analytics.

As FinTechs and other financial service providers drive commercial card adoption, virtual card technology becomes an increasingly popular focus of innovation initiatives, particularly as corporates demand solutions to support a remote workforce. Barclaycard Debuts V-Card For Expense Management.

While vIBANs offer innovation in payment systems, they introduce risks like money laundering due to insufficient oversight. Currently, large enterprises are the primary users, while small businesses and consumers have shown limited adoptionlikely due to unclear policies on customer eligibility and risk exposure. Why is it important?

Payment technology and innovation are accelerating across the fintech industry, with more companies recognising the importance of adapting to changing customer needs, with non-cash transactions projected to hit 2.3 trillion transactions by 2027. This will help create digital payment ecosystems that can reach the 1.4

October 7th 2025 15:00 BST | 16:00 CEST | 10:00 EDT Online Join this Webinar Why have banks’ priorities shifted from core modernisation to ensuring end-to-end bank modernisation? What key technological innovations should banks be investing in? How can these modern tools be integrated into existing systems?

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

Simultaneously, it would entail trade-offs in security, user experience, and operational design that demand careful scrutiny across the industry. Continued collaboration is essential to ensure security, usability, and trust in this evolving financial innovation. However, this structure introduced practical constraints.

In financial services today, security and innovation can work with each other, and against each other. FinServ cybersecurity is, of course, a prime target for innovation. But customers’ constant demand for cutting-edge products and services is adding to the load of already heavy security burdens. What is driving this trend?

Therefore, the adoption of solutions like Google Pay is a must for organisations to stay competitive and meet market demands. The integration of GPay responds to the needs of consumers and merchants for innovative tools that simplify the payment process, said Jaime Parra , head of product LatAm at PayU.

As digital payments become ever more mainstream, consumers will demand seamless interaction with their financial institutions, which means FIs must look at ways they can pivot from branch-based experiences, yet deliver those same high-touch services through digital channels. The change has been a long time coming.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. Eli Shoshani : Early participation allows banks to set themselves apart as leaders in innovation and efficiency.

The acquisition brings together two major players in API-based financial innovation, aligning with Fabrick’s broader mission to enable embedded finance across the region. The announcement that Fabrick acquires finAPI highlights the growing demand for scalable open banking platforms across the continent.

And he said the opportunity surrounding cross-border real-time payments (RTP) will have the most significant impact on end-users due to the “potential implications” for changing how the FinTech conducts business. Blockchain.

For all of the innovation that's occurred in the banking landscape, it's often consumers – not corporates – that benefit from the latest technologies. Looking ahead, data integrations and APIs will continue to be integral components of the corporate banking world as new innovations emerge. The Drive To Upgrade. Connectivity Is Key.

Mastercard is already partnering with ERP (enterprise resource planning) platforms to deliver VCN-led innovation that automates end-corporate users workflows. This substantially streamlined process empowers corporate end-users to seamlessly utilize VCN technology on systems that they use every day such as HRS and Cvent.

In financial services, demand for ease of use and security are sky-high, even for business customers. While that focus on data security is positive for the industry, Cohen warned that it can also hamper financial services players’ other key focus on promoting a better end-user experience.

A pioneer in open banking, Neonomics unveils an innovative new product suite launched as Nello, with the goal to bring open banking to the next level through AI-driven solutions and seamless payments. Every decision was guided by the feedback and experiences of our customers and endusers. Launching across the EU and the U.K.,

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. Among corporates, there is an increasing demand that their global payment activity is able to keep up with the pace of doing business.

Innovation Potential: Ability to create proprietary technology aligned with strategic goals Risk of Incomplete Features: May initially lack key functionalities, requiring iterative updates. He says: “A lot of smaller companies can end up overspending by thinking they need enterprise-scale solutions.

one of the largest FinTech hubs of the world today, initiatives like Open Banking demonstrate the opportunity for regulatory mandates to encourage innovation and competition — even in markets where such regulatory mandates don’t exist. Achieving A Better User Experience. Mixing Innovation With Compliance. With the U.K.

Meanwhile, 36% are likely to receive more cross-border payments, driving the demand for robust international money transfer solutions. Our joint commitment to innovation and financial inclusion will undoubtedly reshape the landscape of cross-border fund transfers in the region.

Rapid globalisation and available technological advancements have spurred the demand for more efficient, transparent, and accessible cross-border payment systems. The G20 Roadmap for Enhancing Cross-border Payments of the Financial Stability Board (FSB) also lists them as a key priority for enhancing such payments.

Last year, 15% of users reported relying on BNPL because they had no other access to credit, this figure has almost halved to 8% in 2024. This is not just about spreading costs; it’s about British consumers taking charge of their financial well-being and making informed choices that align with their changing economic circumstances.”

In addition, enduser spending on wearable devices is expected to reach $42 billion in 2019, with $16.2 In addition, enduser spending on wearable devices is expected to reach $42 billion in 2019, with $16.2 billion of that amount on smartwatches. billion of that amount on smartwatches.

COVID-19 has closed bank and credit union (CU) branches across the United States, sending the demand for digital banking solutions soaring as consumers hop online to manage their finances from home. However, CUs are not the only financial institutions (FIs) looking to offer digital banking innovations to their members.

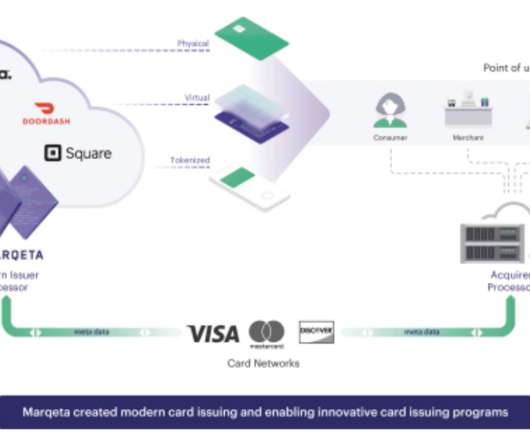

Marqeta (NASDAQ: MQ), the global modern card issuing platform that enables embedded finance solutions for the world’s innovators, today announced a new customer, Swiss4 , providing real-time and personalised digital payment services for their customers.

Amid the pandemic-driven acceleration of e-commerce and shift to digital payments, Marqeta has seen rapid growth in revenue and demand for its card-issuing technology. Revenue is up 103% year-over-year : Marqeta’s revenue for the fiscal year ending December 30, 2020, was $290M , up from $143M in the previous year. First name.

Volt will power Sumsubs Penny Drop Verification flow, which involves an enduser being directed to their banking app after scanning their identity document. Belvo , the open finance platform, secures $15million in a new round of funding to expand open finance access and innovation across Latin America.

NYSE: JBL) today announced ongoing innovation between its payment solutions business unit and Revolut , a digital banking pioneer and global financial super app provider, to support the neobank’s rapid growth trajectory and global expansion in merchant acquiring.

Devices and end-user computing emerged as the second most important investment priority for the finance sector, with over a third (36 per cent) of respondents planning to invest in this area in 2024.

Banking as a Service (BaaS) is poised to change the enduser experience of corporates as they navigate the daily challenges of cash flow management, supply chain activity and the need to become digital-first. So far, corporate banking users are always left out in the cold.” They’re out there; they just have to be used.”.

Now, PayPal stablecoin users can send PYUSD on Ethereum or Solana when transferring out to external wallets. Impact on PayPal users Faster transactions : Because Solana’s blockchain is known for its high-speed processing capabilities, PYUSD transactions on Solana will be much quicker, which will enhance the experience for endusers.

FinTech innovation has opened the floodgates for a stream of new platforms and products designed to help small businesses and corporates more efficiently manage money and make payments. The acceleration of payments innovation has also added complexity to the ability of an accounting platform to integrate payments functionality directly.

To that end, in an interview with PYMNTS, Vincent Caldeira , chief technologist, Financial Services, APAC at Red Hat , said that moving to the digital age will require banks to renovate their suite of core banking functions (checking and savings, for example) by moving to the cloud — and to microservices in particular.

SaaS companies deliver software applications over the internet on a subscription basis, simplifying access and management for users. ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. Primarily through direct-to-user subscriptions and third-party distributors.

Your end-users and clients will demand more as soon as you start improving your analytics. Reach out to the tried and true and highly innovative. It demonstrates The disparity stems from how each department defines "High" as a "Lead Priority." Marketing defines a lead as “High” if they have called into the company.

That includes Payments-as-a-Service (PaaS) in which providers help enterprises accept a range of transactions from their end customers — whether those endusers (the ones actually paying and getting paid) are consumers or corporates. Flexibility Is Key. Technology brings the concept of flexible payments into reality.

” At the same time, ongoing shifts in customer expectations and demands mean that addressing the underbanked does not necessarily mean having to build more physical bank locations. He added that open banking appears to be an “inevitability” as the broader financial services market continues to innovate worldwide.

Here are six practical ways to optimize the experience, boost adoption, and drive more valuefor both your users and your business. Native packages with integrated payments are a great way to provide an easy, seamless user experience and controlled payment processing to your software users. Heres how to select the best provider.

A decade ago, Butler said, an integrated software vendor would partner with an acquirer on the back end. The payments are almost invisible to the end customer, he said. Small businesses, he said, are increasingly demanding that a continuum of customer data be embedded within the software applications they use. “In The Journey.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content