This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The fintech unicorns in Asia are moving to reshape the very fabric of how people and businesses interact with money. Out of the unicorns worldwide valued at a combined $4 trillion , a rising share are coming out of Asias fast-moving fintech ecosystem. These include two decacorns from India and China, each valued at over $10 billion.

Fintech solutions are changing this landscape, offering SMEs tailored tools to overcome these barriers. From innovative lending platforms to advanced payment processing, fintech is enabling them to access growth opportunities and thrive in today’s competitive markets. Fintech companies see this gap as an opportunity to innovate.

For decades, banks have innovated around functionalitystreamlining transactions, expanding access, and introducing digital tools. Techcombank , Vietnams fifth-largest bank in asset size and second-largest private bank, has answered that call with clarity and conviction. But the rules of the game have changed.

Senegal is one of many countries across the Middle East and Africa trying to diversify its economy and future-proof itself by hosting financial inclusion by employing fintech solutions. Mobile phone usage in Senegal has surpassed 60 per cent this year. appeared first on The Fintech Times.

Welcome to the Fintech Review guide , our definitive source for everything fintech. Over the years, weve covered a broad range of fintech topics from digital banking to decentralised finance , regtech , green fintech , and more. What Is Fintech? At its core, fintech challenges the status quo.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financial inclusion and helping people develop healthy financial habits. Sending cross-border payments, for example, often comes with heavy processing costs and conversion fees.

Think about how easy it is to order a ride on Grab, book a hotel on Agoda, or pay for groceries on Shopee without even needing to pull out your credit card or open a banking app. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

year-over-year (YoY), according to the National Bank of Cambodia (NBC). Wing Bank, TrueMoney among most used services for e-commerce payments Findings from the study featured in the Profitence report further underscore the rapid rise of digital payments and digital banking in Cambodia. million transactions in 2023, up 28.7%

In emerging markets, fintech is profoundly transforming financial services. These markets, often characterised by underdeveloped financial infrastructure , benefit significantly from fintech innovations. This article delves into how fintech is reshaping financial services in these regions.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

13 fintech companies from Southeast Asia have been named among this year’s top 250 fintech companies worldwide, recognized for their growth and significant impact on the global fintech landscape. These companies are featured on the World’s Top Fintech Companies 2024.

The Fintech Times Bi-Weekly News Roundup takes a look at the latest fintech stories from around the world on Tuesday 21 January 2025. Offa , the UK Islamic property finance fintech, is joining Connect IFA , a specialist mortgage brokerage network. Most recently, he served as chief operating officer at Bankable.

We examine both quantitative gains— such as higher customer satisfaction scores, rising self-service usage and digital adoption rates—and qualitative developments, including more personalized services, smarter virtual assistants and greater accessibility in digital banking. IDC estimates the banking industry will invest about $31.3

Businesses can now process payments across multiple channels – including in-person, online, mobile, and over the phone – with greater speed, efficiency and security. The post Epos Now Partners with Lloyds Cardnet appeared first on FF News | Fintech Finance.

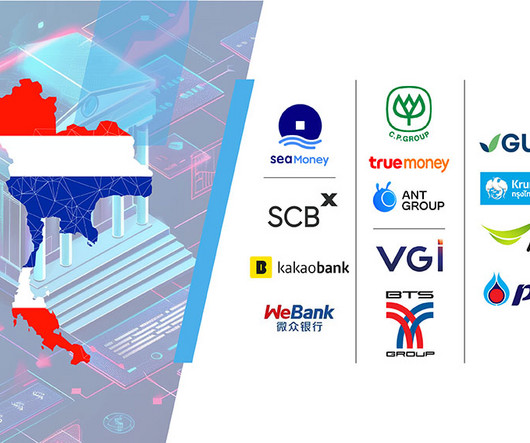

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

Kueski , the buy now, pay later (BNPL) and online consumer lender in Latin America, has launched an in-store version of Kueski Pay, which will become available to all consumers by the end of Q2 of 2024, to offer them the ability to complete transactions through the Kueski mobile app, regardless of internet connection, in physical stores.

Who are the top funded fintech startups in Indonesia as of early 2024? In 2022, the country was home to 993 active fintech companies, representing about 25% of all fintech ventures operating across the ASEAN region, data from a 2022 report by the United Overseas Bank (UOB), PwC Singapore and the Singapore Fintech Association (SFA) reveal.

The Singapore Fintech Festival (SFF) has announced the finalists for its 2024 Fintech Excellence Awards, organised in partnership with the Singapore Fintech Association (SFA) and supported by PwC Singapore. Integrated with bank accounts and digital wallets in Pakistan, Hakeem provides customers with easy disbursement options.

In celebration of this year’s International Women’s Day on 8 March, the Fintech News Network is unveiling its selection of ten of the most influential female fintech leaders in Asia Pacific (APAC). These trailblazers are elevating the industry, demonstrating resilience and leadership in the ever-evolving fintech landscape.

Over the past decade, Singapore has emerged as a global powerhouse in fintech innovation, not just in Southeast Asia but across the broader Asian region. This rapid growth has solidified Singapores position as a leader in the global fintech ecosystem while driving significant investments in other forms of financial tech.

Now encapsulating a focus on societal impact and the environment, the term ‘fintech for good’ has evolved from its initial meaning of charity. This July, we are on the hunt to find out how the fintech industry is doing ‘good’ for local communities and the world, revealing current and future plans to make change.

From bustling megacities to remote villages, digital finance is breaking down barriers, giving millions access to banking, credit, and investment opportunities for the first time. Here, we spotlight the fastest-growing Asia Pacific fintechs leading the charge in the future of finance in 2025. They’re reimagining whats possible.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. First name. Company Name. Phone number. Source: PwC.

NOW Money , one of the leading inclusive digital payroll and banking platform for migrant workers, today announced its new strategic partnership with Mastercard , a global technology company in the payments industry. Customers can handle payments, transfers, and other financial operations directly from their mobile phones.

Now encapsulating a focus on societal impact and the environment, the term ‘fintech for good’ has evolved from its initial meaning of charity. This July, we are on the hunt to find out how the fintech industry is doing ‘good’ for local communities and the world, revealing current and future plans to make change.

Virtual bank Radius Bank — which services small businesses (SMBs), micro-firms and consumers — is rolling out a revamped digital banking platform and a mobilebanking app, the company said on Monday (Dec. The platforms have added new digital solutions for financial budgeting and tracking as well.

The report, Advancing Economic Inclusion—Empowering Underserved Communities with Fintech , highlights the innovative products and services revolutionizing the way commerce is conducted through safe, secure, convenient, and rewarding solutions.

Lloyds Banking Group is shutting down its mobile van banking service this year and closing 123 branches, sparking concern over reduced access to essential financial services, particularly in rural and underserved areas. is unhappy with Lloyds’ decision to stop its mobile van banking service.

Cambodia is leveraging fintech innovations and strategic reforms to boost economic growth, financial inclusion and international partnerships, positioning itself as a key player in the Southeast Asian digital economy. per cent this year and six per cent next year, according to the Asian Development Bank. million in 2021 to 19.5

In the sixth annual compendium of 500 burgeoning companies across the Asia Pacific (APAC) by the Financial Times and Statista , technology enterprises constitute nearly a third of the 2024 roster, with 8% of the APAC’s fastest-growing entities being fintech companies.

That means actual funds reside in their account inside your system, not just a link to their card or bank. It simply facilitates transactions by linking to your customers existing financial instruments, like bank accounts or credit/debit cards. Digital wallets, meanwhile, appeal to digitally active, banked customers.

Orange Middle East and Africa (OMEA) ( www.Orange.com ) and Mastercard have announced a strategic partnership to expand access to mobile financial services across Sub-Saharan Africa. The partnership will be rolled out in seven countries including Cameroon, Central African Republic, Guinea-Bissau, Liberia, Mali, Senegal and Sierra Leone.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

Indigenous Banking (Shroffs and Mahajans): Long before modern banks, India had a thriving indigenous banking system. These banks introduced formal ledger-based accounting and cheque payments. This expanded the reach of formal banking to rural areas. This introduced standardization and divisibility.

With the launch of a new payment system, the platform now automates the collection of funds into integrated business bank accounts—aiming to double its transaction volume via SEPA Instant. “At YowPay, our mission is to simplify SEPA transfers for merchants across Europe.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. Chilean fintech Banca.me

This revolutionary service provides over 5 million Lebanese citizens with the ability to manage their payments securely and transparently for local and international purchases without needing a bank account. Through Wink Pay, we can simplify and digitize customer onboarding, as well as facilitate online payments.

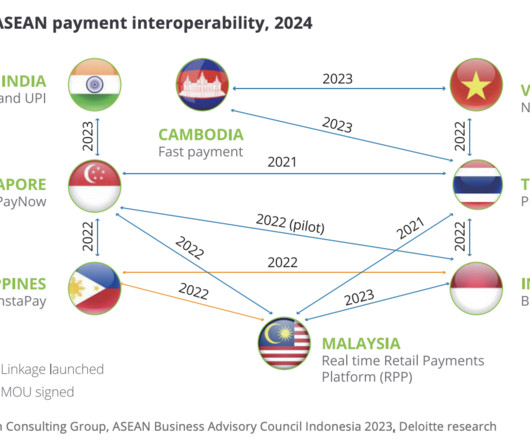

Asia Pacific point-of-sale payment methods – Select markets, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Payment interoperability The growth of digital payment innovations in APAC has emphasized the need for connectivity and interoperability in both online and offline transactions.

Orange Middle East and Africa is strategically partnering with global payments giant Mastercard to expand access to mobile financial services across Sub-Saharan Africa. Only 48 per cent of the African adult population is banked, according to the African Digital Banking Transformation Report.

Traditional banking products, including checking, credit, and savings accounts, are under threat from a new crop of digital-first startups. Many of these startups are launching products without a bank charter and targeting a very specific customer base. DOWNLOAD THE 61-PAGE consumer banking REPORT. savings accounts.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

However, recent stringent regulations imposed by the Reserve Bank of India (RBI) have significantly impacted the sector, leading many fintech companies to reassess their BNPL strategies. Similarly, Slice, originally a BNPL firm, has transitioned to offering prepaid credit cards and is now merging with North East Small Finance Bank.

Consumers in the Philippines are demanding so much from online technologies, that research from Digido , the Filipino online lender, has found the digital lending market could reach $1billion in the second half of 2025. Digido revealed that in terms of market structure, non-bank digital lenders are expected to make up 55.2

New research from Economist Impact supported by Temenos finds that European banks are fighting back against competition from platform players, neobanks and payment providers. European banks are also migrating core banking systems to public cloud and SaaS in greater numbers than their counterparts in other regions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content