This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Brite Payments , a leader in instant bank payments, has announced that George Parks Davie has been appointed VP Product. Davie also played an active role in shaping PSD2, which underpins open banking in Europe today, through the European Banking Associations Working Group on APIs under PSD2.

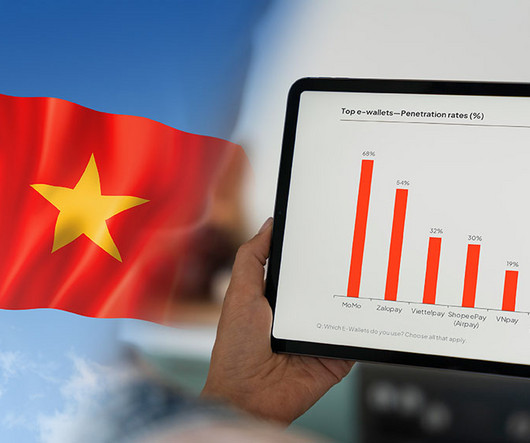

In Vietnam, bank-owned apps are rapidly gaining popularity across all generations, outpacing independent fintech platforms like MoMo and ZaloPay, which are seeing a decline in usage and preference, according to a new report by Decision Lab, a Vietnamese market research firm. million monthly active users, giving it a massive scale and reach.

Customers in this age of instant gratification always expect a smooth and seamless online payments experience. As a business owner, you must have a clear understanding of how online payments processing works to be able to create a hassle-free checkout process that will keep buyers coming back to your eCommerce store.

Visa bolsters Asia Pacific product suite Payments giant Visa showcased a range of new products and solutions at Singapore Fintech Festival, revealing plans to roll them out across Asia Pacific. These include: Visa Flexible Credential – This enables a single card product to toggle between payment methods.

In recent years, businesses have seen this massive shift from desktop to mobile devices which has forced them to develop apps with built-in integrated payment gateways. But when it comes to payments, mobile apps have to contend with a few unique challenges. Why Would Companies or Developers Want a Mobile App Payment Gateway?

Citi (NYSE: C) and Bank of Shanghai launched a first-of-its-kind payments solution on Bank of Shanghai ’s TourCard. The innovation helps enable travelers to add funds to their TourCard digital account with Bank of Shanghai from another source, helping to make the payment experience smoother when settling expenses locally.

UK bank NatWest has partnered with payments giant Mastercard to launch a new mobile virtual card payment solution for business, Approval2Buy with Mobile Virtual Cards. Firms can instantly generate virtual cards for online use, as well as for ‘Tap and Go’ payments via digital wallets.

billion Matrixport is a digital asset platform that provides a range of crypto investment products and financial services for both beginners and experienced investors. From high-yield savings and structured products to advanced trading tools, Matrixport helps users grow and manage their digital wealth. Matrixport Valuation: $1.05

In keeping with its constant dedication to providing cutting-edge services to its customers, National Bank of Kuwait (NBK) announced introducing a new service that allows customers to confirm payment transactions online through the NBK MobileBanking App, making itself as the first provider of this service in Kuwait.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactless payments continues to grow. Or they could use a mobile credit card terminal if they prefer to collect payments at the table.

How fintechs are challenging traditional banks in the merchant services space, posing a threat to banks’ core business and revenue streams. The shift driven by fintechs could erode banks’ dominance, forcing them to modernise or risk losing a significant share of the market. Why is it important? What’s next?

With so many payment options available from credit cards to mobile wallets it can be hard to know which methods are the best fit for you and your customers. But a growing number of businesses especially those online have dropped cash altogether because it doesnt make sense for their operations.

Fast innovators are 18 times more disruptive, reports BCG, and getting new products to market quickly generates more sales from them at least 30% of revenue. Indeed, rapid product development remains a top priority. Instead of hard coding, they create new products using flexible parameters.

Banking has entered a new era. To bank digital today is no longer a novelty, it is the default. From account opening to investment tracking, every core function of traditional banking now has a faster, more user-friendly counterpart online. What Does It Mean to Bank Digital?

Artificial intelligence (AI) is helping organisations take their offerings to the next level, and reflecting on how it has done so over the last few years for itself, the US based financial institution, Bank of America has revealed that AI is now embedded across multiple business lines and areas including global technology, operations and training.

The Visa Flexible Credential all started with a simple idea that consumers should easily be able to choose how they want to pay,” said Jack Forestell, Chief Product and Strategy Officer, Visa. We look forward to bringing millions more people a product that seamlessly brings debit and credit together, without late or hidden fees.”

At the Visa Payments Forum in San Francisco, Visa has unveiled new products which will address the evolving consumer payments demands. The new products and services Visa unveiled will begin to roll out later this year. This year, new ways to ‘tap’ on a mobile device will become an integral part of the Visa experience.

These companies span every segment of the market, from long-established remittances players and banks to neobanks, business-to-business (B2B) platforms, stablecoin providers and regional specialists, and are powering global trade. It also offers services and products to businesses such as accounts, expense cards, and payroll.

In a country where mobile payment growth is projected at 22% annually, adopting solutions like Google Pay is essential to meet market demand. According to a recent report by Statista, the mobile wallet transaction market in the region is projected to reach $372.41 billion by 2025, compared to $59.74

Some banks have chosen to develop their own in-house payment processing systems, delivering end-to-end services directly to their customers. Other banks have formed strategic partnerships with third-party providers. From internal solutions to partnerships, we’ll provide an overview of each bank’s approach.

TRANSFOND , the Romanian Banking Association , and the entire banking community in Romania announce that the new RoPay system has become operational. RoPay allows users to make instant mobile payments in line with the national payment scheme. The first available use is for proximity-based person-to-person (P2P) payments.

Sometimes, the cashier entered the product and quantity manually. Its the central hub for businesses to complete purchases, whether in-store or online. Some retailers may use a mobile device, such as an iPad or Android device, as their POS instead of a computer. For online stores, this step is a bit different.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. These are not banks, but rather governing bodies that set interchange rates, and arbitrate between acquiring and issuing banks. Acquiring Bank: The business’ (i.e., merchant’s) bank.

Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Despite their significant contributions to GDP and employment, SMEs in emerging markets remain underserved by traditional banking. Traditional banks typically require extensive documentation, credit history, and collateral, which many lack.

We can hail a ride from a mobile app, and our transactions for all sorts of goods and services can be easily paid for from our phones. There are a wide variety of digital payment types, such as mobile POS systems, contactless payments, and digital wallets. All you need to use a digital wallet is a smartphone.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

Emirates NBD , a leading banking group in the Middle East, North Africa and Trkiye (MENAT) region, is set to be the first bank in the UAE to introduce the Visa Commercial Pay-Mobile Module for its SME and Corporate clients, in collaboration with Visa.

Like most business owners, your instincts tell you to hop on the bandwagon and launch an online store for your business. From different types of online payment gateways and key features to look for, to tips to help you choose the right payment solution for your business and implement it. This is expected to grow to 22.6%

MTN Mobile Money (U) Limited, in partnership with Mastercard , Diamond Trust Bank and Network International, has launched the Virtual Card by MoMo, an innovative payment solution designed to enable MTN MoMo subscribers to perform secure online transactions without needing a physical card or bank account.

As banking becomes more digitally-focused, it is becoming critically important for banks across the globe to embrace digital transformation, implementing more intelligent and embedded systems into their operations. It is about reimagining the core of banking – how a bank runs, scales and adapts – not just its interfaces.

They enable secure, efficient in-store and online payment processing and offer flexible payment options that customers demand today. Merchant services are comprehensive solutionstools, systems, and supportthat allow businesses to process in-person and online payments. custom software for a particular industry or market).

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

Artificial intelligence (AI) in mobile food ordering: tantalizing. That’s a silly simplification of the very serious matter of what AI is doing for the restaurant sector, among others, as online ordering becomes a way of life and not just a lockdown relic. Advanced AI Makes Systems Smarter. Catering to Individual Tastes at Scale.

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) To accept online payments, you need a payment processor and payment gateway.

On top of that, 69% of Americans online in 2023 said they used digital payment methods to make a purchase. A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. billion transactions and $9.76

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services. Looking to 2025, mobile payments and digital commerce are projected to exceed 10 trillion, with open banking and real-time payments leading growth.

Financial institutions (FIs) are among the entities that are working to securely meet clients where they are through mobile and online channels to complete tasks that would more often be completed in person. The technology is available at bank branches and remotely via mobile and its website. and 34 other countries.

Accepting payments always comes with processes and fees, particularly when it comes to online or digital payments. TL;DR A payment link enables you to request and accept online payments without having to build a website or checkout page. Payment links are ideal if you don’t process a lot of online sales.

Global payment juggernaut, Mastercard is expanding its presence in the UAE’s flexible payment and lending ecosystem as it partners with the shopping, payments and banking fintech, Tamara to launch a new virtual card.

Armenia Population: +2,967,000 Capital, financial hub and largest city: Yerevan Gross domestic product (GDP) per capita: +$8,500 Access to a formal financial account (adults): 52.3 per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. per cent holding a credit card.

With a payment gateway, they simply enter their card details online on your website or app. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer. For example, if you operate an online store, you need fast and secure online payment solutions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content