This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). Checks can bounce, and cash can get lost. EFT and ACH payments are fast, secure, and hassle-free. No cash or checks needed.

ACH transfers, or payments made through the Automated Clearing House network, account for billions of dollars in payments annually. In fact, NACHA, the nonprofit that governs the ACH payments network reported 6.1% The average consumer commonly uses the ACH network for automated bill payments and larger transactions.

National Processing Check 21 vs ACH: Key Differences and Which One Fits Your Business A merchant or business trying to decide the best electronic payment processing system may be interested in the differences between Check 21 and ACH.

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financial institutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

Two of the more common methods are known as ACH and EFT transfers. Time for a deep dive, but first, let’s have a basic, simple-terms introduction to the two services before looking closer at ACH vs. EFT payments and transfers. What Exactly is an ACH? Depending on your end goal, there are a few different types of ACH.

Point & Pay is utilizing Trustly’s Pay by Bank tools for enabling single sign-on with banks to deliver a next-generation approach to paying government obligations, reducing the occurrence of returned checks – a first in the electronic government payment platform space.

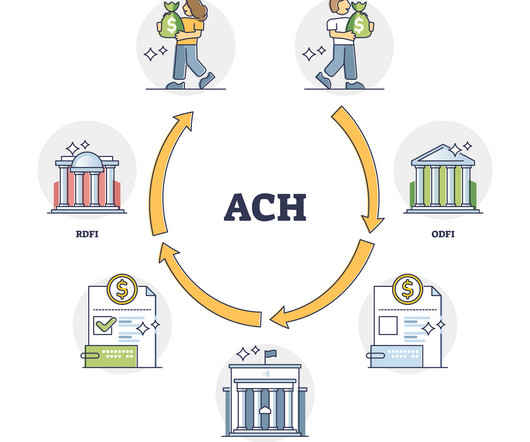

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. Unlike payments facilitated by card networks like Visa or Mastercard, ACH payments are managed by a body called the National Automated Clearing House Association (NACHA). Let’s get started.

ACH & Bank Transfers Some businesses, especially those in B2B (business-to-business) sectors, rely on bank transfers like ACH payments or wire transfers. Chargebacks when customers dispute a paymentcan also be expensive and time-consuming. These sectors prioritize speed and customer experience.

Much like in the United States (and practically the rest of the world, for that matter), Canadian consumers have widely adopted credit cards and digital payments. of consumers owning at least one credit card. Beyond credit cards, Stax supports ACH, mobile payments, and online invoicing, providing flexibility for your customers.

These include the investment world, where paper checks are often used to pay out quarterly dividends or other such disbursements. Paper checks’ drawbacks for such payments have been evident for some time as they represent both a time-consuming and costly way to send out disbursements.

If ever there was a time to kill the check, that time would be now. The remaining tens of millions, those who do not have direct deposit payment information on file with the IRS … will have to wait for the proverbial (paper) check in the mail. There also is Mastercard Send for push payments as an alternative to ACH.

Checks, despite their near extinction in consumer payments, remain alive and well when it comes to businesses paying each other. The check – for its many, many flaws – does address all three of those aspects. That is why checks have been so resistant to replacement. And that’s pretty well why it persists.

It’s been a boon for ACH payments, said Jeff Thorness, president of Forte Payment Systems , a CSG company. As Thorness explained, their embrace of ACH processing technologies is likely to have far-reaching impacts into how they send and receive payments with government suppliers, too, particularly as ACH innovation accelerates.

Transaction volume on the EPN ® system, the ACH network operated by The Clearing House Payments Company L.L.C., in 2024, continuing the trend of yearly ACH volume and value growth. ACH commercial volume last year. per year, as businesses and consumers continued to embrace electronic payments.

Automated Clearing House (ACH) transactions are revolutionizing how businesses and consumers transfer money, offering a variety of payment types to meet diverse needs. Recognizing the different types of ACH payments and their relevant codes is crucial for navigating this complex landscape. What are ACH payments?

Accepting paper checks is an inconvenient and outdated business practice. In today’s world, ACH payments thrive and replace the paper check as the more convenient, safer, and faster payment solution. In recent times, ACH payments have increased in popularity. One might think accepting a paper check is free.

Many businesses today still rely on paper checks to disburse funds. However, according to the ACI Speedpay Pulse 2024 Report, consumer preference for digital payment channels is trending upward, with more than 75% of Americans preferring digital transactions.

While paper checks are increasingly passing into the realm of consumers’ memory, there are certain niches where they have managed to hold on, even as the rest of the world tries rather adamantly to move on. We’ve known for more than 10 years that there are issues with mailing checks, which is why we’ve seen over 4.5

But the transition is one that must consider, and maybe even embrace, several emerging options and payment rails in a bid to move data and money more quickly across borders, and move, decisively, away from paper checks. Moving Beyond ACH . Real time and the ACH network can actually work together to displace paper checks.”

You’ve probably heard the term “ACH deposit,” but what does it really mean? ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? ACH direct deposits are common. What Is an ACH Deposit? So, what does an ACH deposit mean?

The payment processing market in the United States has demonstrated robust growth, driven by rising consumer demand for digital payments, advancements in financial technology, and the expansion of e-commerce. This growth is driven by increased adoption of digital payment methods, evolving consumer behavior, and an expanding e-commerce sector.

The Financial Crimes Enforcement Network (FinCEN) issued a press release warning financial institutions (FIs) and consumers about pandemic-related scams, including some connected to cryptocurrency. FinCEN warns that bad actors “are engaged in fraudulent schemes that exploit vulnerabilities created by the pandemic.”

In 2019, 77% of US consumers were using at least one type of digital payment system. What has grown more significantly is the number of electronic payments and alternative payment methods consumers now use. The adoption of digital payment systems in the US has grown, with 78% of consumers using at least one type by the end of 2020.

While payment methods vary depending on location, merchant, and type of transaction, ACH payments are one of the most used electronic payment systems in the U.S. What is ACH? ACH transfers refer to the electronic transfer of funds between banks through the ACH network. What is an ACH return?

Automated Clearing House ( ACH) transfers have revolutionized the way we handle our finances, offering a convenient and secure method to send and receive money electronically. Whether it’s receiving your paycheck through direct deposit or paying your bills online, ACH payment solutions have become an integral part of our daily lives.

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACH network in a single transaction or within a specified period. This article will shed light on what ACH transactions are, the nature of their limits, and the influencing factors. What is an ACH transfer?

What is an ACH transfer? ACH (Automated Clearing House) payments are basically EFTs ( electronic fund transfers ) that use the ACH network to move funds between bank accounts in the United States. ACH is most commonly used for direct deposit of payroll, payment of bills, and business-to-business payments.

While there has been some innovation in wage payment mechanisms as more employers shift away from the paper check toward direct deposit and payroll cards, little has changed about the timing of those payments. consumers living from paycheck to paycheck, according to PYMNTS’ latest Navigating the COVID-19 Pandemic report.

For example, suppose a huge global consumer packaged goods (CPG) conglomerate wants to introduce a new shampoo. Maybe ACH ? Or maybe even fast ACH? Slowly but surely, corporates are migrating away from checks. When it comes to global B2B procurement, nothing is simple. Does it do so by old-school wire transfer?

If your institution saw an increase in ACH transactions last year, you’re not alone. NACHA, the payments clearing house through which ACH transactions flow, reported a banner year in 2020, posting an 8.2% Additionally, ACH internet transactions rose 15% from 2019 to 2020. As it happens, 2020 was a banner year for ACH fraud, too.

The Automated Clearing House (ACH) payment system facilitates the movement of billions of dollars every day, operating behind the scenes in the U.S. In this article, we'll explore the ACH network and ACH payments, how ACH payments function, and the ways in which it impacts our daily financial transactions.

More and more, cash-only businesses are falling by the wayside, unable to keep up with consumer demand for convenient electronic payments. TL;DR An Electronic Funds Transfer is an umbrella term for payments that are conducted electronically—essentially, any payment method except for cash and paper checks. EFT payments are fast.

Now, if youre a small business managing all of that can be time-consuming and difficult. This gives customers maximum flexibility over how they want to paywhether that be ACH (bank account transfers), digital wallets, to credit and debit cards. Apple Pay, Google Pay), or ACH transfers. This is where payment links come in.

Myriad universities still use paper checks to send tuition or housing payments, despite the well-documented inefficiencies. Just 5 percent of millennial students paid their tuition with checks. Check delays could prevent them from paying for housing, food or academic supplies, putting them behind academically and financially.

NACHA released new statistics late last week on growth of ACH transaction volume in the U.S. According to the firm, B2B transactions were a key driver of ACH transaction growth in the third quarter of the year, leading NACHA Chief Operating Officer Jane Larimer to describe the ACH Network as “thriving.”. In all, more than 3.3

This week’s examination of the latest in payments rails innovation finds financial service providers innovating on top of existing rails to address the friction of ACH, checks and other bank transfer infrastructure. ACH Gets A Boost In The Public Sector. Invoiced Tackles The Friction of Check.

He said increased sharing of account information through third-party apps supports consumers’ desires, but it is not without its risks. This provides consumers increased transparency and control over their payments, eliminating unintended overdrafts, and reducing fraud. This has resulted in some delays and consumer confusion.

But how consumers will get those payments — hundreds of millions of payments, covering hundreds of billions of dollars — well, that’s open to some discussion. In a panel discussion, three payments executives discussed the ways disbursements on a huge scale must make the leap beyond the paper check, beyond the ACH conduits.

Even though ATMs, mobile banking, and credit card payments are part of our everyday life, some people still write checks. For others, they take advantage of the processing lag-time to give a few extra days to receive the money they are writing the check against. So as a business owner, how should you handle bad checks?

Ach and Wire are two of the most popular ways of money transfer in the United States. First, let's delve into the mechanics of ACH and Wire transfers, followed by an exploration of their distinctions, guidance tailored for small businesses, and concluding with instructions on establishing ACH and Wire processes.

Payments speed is a crucial consideration for today’s consumers and microbusinesses when receiving disbursements, with PYMNTS’ research finding that more than half of the former and roughly 70 percent of the latter say they received at least one nongovernment payment within the past 12 months. percent of consumers and 70.8

Part of the tailwind comes from the fact that consumers are becoming more aware that there’s a better mousetrap out there. As has been widely reported, millions of Americans had to wait weeks and months for paper checks to arrive. In other cases, stimulus payments were commingled with tax refunds, and were subject to garnishment.

Consumers and microbusinesses have access to many disbursement options, yet they receive a significant share through legacy methods such as paper checks or digital methods that are non-instant. percent of consumers and 42.5 percent of Generation X consumers are unfamiliar with instant payments, while only 39.3

Fact: modern consumers are increasingly gravitating towards eCommerce businesses. Instead of driving down the complicated road of bank transfers or check payments, you can give your customers a simpler way to complete their purchases through your own website. Payment gateways step in when a customer is about to check-out online.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content