This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Navigating AML obligations in the age of virtual IBANs February 10 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The compliance challenges of virtual IBANs, focusing on AML obligations and regulatory gaps. Why is it important?

It highlights new corporate responsibilities, significant penalties for non-compliance, and the businesses need to implement strong fraud prevention measures to protect their financial and reputational standing. Compliance requires proactive fraudriskassessment, the implementation of preventive procedures, and a culture of accountability.

As director/MLRO of SENDS, a UK-licensed EMI, I see AI’s potential in fraud prevention, AML, and compliance. Sends leverages AI to mitigate risks, comply with FCA, PSD2, and PCI DSS, and enhance client experience with secure and innovative services.

Regulators need clear guidelines on accountability, particularly in cases of erroneous or harmful AI-driven decisions, such as wrongful frauddetection or unfair credit scoring. Also, the autonomous nature of the AI means decision-making is often removed from human oversight.

Fraud and risk platform DataVisor launched its anti-money laundering (AML) solution this week. The new offering combines fraud fighting and anti-money laundering operations in a unified, approach that helps institutions better deal with emerging threats and evolving regulations.

We have built on top of the FICO TONBELLER solutions using FICO’s battle-proven and patented artificial intelligence and machine-learning algorithms, which are used in FICO Falcon Fraud Manager to protect about two-thirds of the world’s payment card transactions. The weights of the model are either expert-driven or based on limited SAR data.

ComplyTek introduces an advanced transaction screening solution for instant payments , designed to ensure compliance and mitigate fraud within the critical 10-second processing window. Leveraging machine learning and AI, the platform offers comprehensive monitoring and frauddetection capabilities.

Frauddetection and riskassessment: MCCs assist frauddetection and riskassessment operations by flagging suspicious transactions. For example, if a credit card is suddenly used at a pawn shop after being consistently used at beauty shops, this can indicate fraud.

Guest panelists included James Nurse, Managing Director at FINTRAIL; Hannah Becher, Lead of Fraud and AML Surveillance at Pleo; Matthew Tataryn, Director of Financial Crime Risk at Tide Platform; and Jeremy Doyle, Director of Growth, AML Solutions at SEON. We see synergies, especially in escalating high-risk cases.

As the global marketplace grows more interconnected and transactions shift online, businesses face an unprecedented wave of commercial fraud attempts, from sophisticated “bust-out” schemes to synthetic identity fraud that blends real and fabricated data. Please consider becoming a paid subscriber. billion in 2022 to $252.7

FRAML, or Fraud and Anti-Money Laundering, represents a holistic strategy that presents an effective way for organizations to strengthen their defenses against both fraud and risk. Bridge the Gap Learn how FRAML fosters collaboration between fraud and compliance teams, breaking down siloes for a more robust defense.

AI can make it easier for financial institutions (FIs) to predict how likely their customers are to make timely payments and improve overall riskassessment capabilities. However, many FIs lack internal proficiency to use AI-assisted credit riskassessment for maximum effectiveness.

A riskassessment follows, evaluating the merchants profile through credit checks and performance analysis, leading to application approval or rejection based on these findings. Risk Management Advanced frauddetection tools monitor transactions in real time to identify potential fraud.

In this article, we’ll discuss what SaaS companies looking to become payment facilitators need to know about risk management strategies. PayFacs handle riskassessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks.

PayFacs need to equip themselves with an effective risk management strategy that helps them continuously monitor risks and employ appropriate risk responses if needed. Frauddetection and prevention. Early detection can help in the rapid mitigation of fraud.

Banks that use AI-driven predictive models are able to detect the risk of delinquency as many as 12 months before a customer ever misses a payment, providing banks and their customers the breathing room they need to take action. The practical applications for AI extend far beyond credit riskassessment and detection, however.

With the Economic Crime and Corporate Transparency Act having received royal assent on 26 October, financial institutions must ensure they up their game and deliver sophisticated riskassessments over the coming months. Without them, those found to have failed to prevent certain instances of fraud could pay a very heavy price.

In payments, AI-powered systems can enhance frauddetection and streamline cross-border transactions, potentially revitalising correspondent banking relationships that have dwindled due to regulatory pressures. This could help address the decline in correspondent banking relationships, a concern highlighted in the BIS report.

With the acquisition of Tonbeller in 2015, FICO expanded its fraud portfolio and moved into the growing market for financial crime and compliance solutions to bring the benefits of advanced analytics to a field dominated by rule-based systems. By investing in AML, you can actually gain competitive edge. In the U.S.

KYT is an anti-money laundering (AML) and counter-terrorist financing (CTF) requirement. The goal is to try to detect fraudulent transactions and combat behavior associated with money laundering and other fincrime such as terrorist financing. Ask an Expert What Does KYT Mean for AML Compliance? Why Is KYT Important?

Lynn , partner at BPM , an assurance, advisory, tax and wealth management company, explains the benefits that automation can offer firms: “Risk orchestration is designed to enhance frauddetection and reduce risk to the entity that implements it. For fraud, the focus was historically on customer identity.

Risk management framework: Develop a robust risk management framework that identifies, assesses and mitigates key risks associated with your business operations. This includes conducting a thorough riskassessment, implementing appropriate risk controls and establishing effective monitoring mechanisms.

This includes a high concentration in anti-money laundering (AML), frauddetection, and client onboarding. 85% of digital-first payment firms report live AI integration, particularly in fraud analytics and real-time risk scoring.

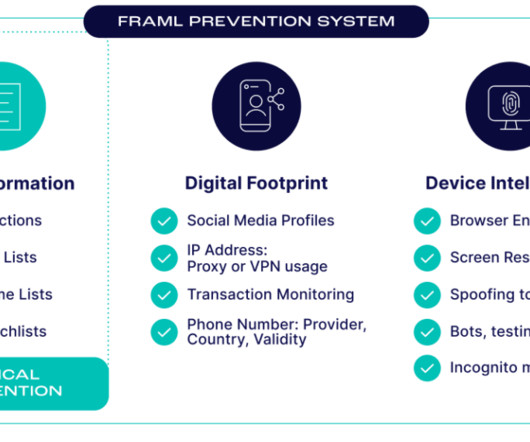

Advanced technologies, including artificial intelligence (AI), blackbox and whitebox machine learning (ML), digital footprinting and device intelligence, collectively transform the real-time frauddetection and prevention paradigm.

Applicable to large organisations, the offence imposes criminal liability if firms do not have adequate fraud prevention procedures in place, even if senior leadership is unaware of the misconduct. For merchants, particularly large retailers, platforms, or multi-channel businesses, this marks a significant shift in fraud liability.

Bank extraction software can be used to extract this information and use it for loan approvals and riskassessments. Automate your mortgage processing, underwriting, frauddetection, bank reconciliations or accounting processes with a ready-to-use custom workflow.

The advancements in AI, ML and automation transform frauddetection and protection by augmenting human capabilities with algorithmic precision and scalability. Such instances erode trust and undermine the perceived reliability of a company’s frauddetection systems. In 2023, global AML fines reached beyond $5.8

Increased accuracy - automation can eliminate the risk of human errors in data entry and processing, resulting in more accurate customer filtering. Better riskassessment - automation can provide lenders with more detailed financial information on potential borrowers, enabling them to make better riskassessments.

Security & Fraud Prevention Given the high-risk nature of online gaming, security is non-negotiable. Look for a gateway that includes PCI compliance, frauddetection tools, chargeback mitigation strategies, and AI-driven risk analysis to protect transactions and user data.

Enhanced FraudDetection and Security One of the most significant advantages of AI and Machine Learning in banking is its ability to detect fraudulent activities and enhance security measures. What dangers lurk in the shadows of Generative AI in Banking?

In this Q&A, NVIDIAs EMEA Payments & FinTech Leader, Georgios Kolovos, explains how AI is revolutionising frauddetection, risk management, and customer engagement in the payments industry. False positives in frauddetection remain a major challenge for payments companies.

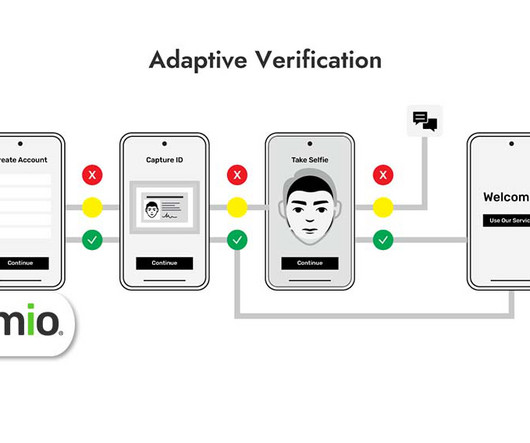

The Jumio Platform provides AI-driven eKYC, riskassessment and AML compliance services in a unified workflow to verify the identities of new and existing users, fight fraud and help meet compliance mandates throughout the customer journey.

From anti-money laundering (AML) to know-your-customer (KYC) obligations, the compliance burden is growing. More Accurate Risk Management Photo by Francesco Ungaro on Pexels.com Fintech companies operate in dynamic environments. AI models can monitor live data feeds and adjust riskassessments dynamically.

Irregularities in Credit RiskAssessment- Credit riskassessment is critical in microfinance to ensure that loans are extended to creditworthy borrowers. They faced challenges in fraud prevention, riskassessment, compliance, customer retention, NPA management, operational efficiency, and collections.

This includes undertaking robust fraudriskassessments, embedding tailored internal controls, and delivering ongoing staff training. Firms are also expected to maintain proper oversight mechanisms and ensure that anti-fraud policies are proportionate, dynamic, and integrated into business-as-usual operations.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content