This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With all the hype around artificial intelligence, many of our customers are asking for some proof that AI can get them better results in areas where other kinds of analytics are already in use, such as creditriskassessment. My colleague Scott Zoldi blogged recently about how we use AI to build creditrisk models.

With all the benefits of artificial intelligence, many of our customers are wanting to leverage machine learning to improve other types of analytic models already in use, such as creditriskassessment. My colleague Scott Zoldi blogged a few years ago about how we use AI to build creditrisk models.

When it comes to using alternative data in creditriskassessments, the field has really opened up over the last few years. Here is useful information on how to assess alternative data and combine it with so-called traditional data to improve creditrisk models. Multiple Types of Alternative Data.

Having worked in creditrisk for most of my career during the revolution in analytics, it continues to concern me that the collections and recoveries (C&R) divisions of banks seem to be left behind. Innovations in creditrisk analytics that have been widely adopted in other risk areas rarely get used at the C&R level.

Home Blog FICO What Does 2023 Have in Store for U.S. CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

The Empirica Score was developed by predictive analytics software company FICO with the aim of equipping organisations that offer credit to their customers with solid riskassessment when determining an applicant’s eligibility for a credit. Account Origination Analysis Shows Downward Shift in Risk.

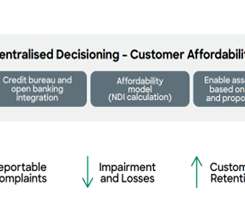

Covid to Cost-of-Living: Assessing Affordability in Uncertain Times. Affordability Assessments and Unrestrained Lending. Triggered in part by the US housing market collapse and an unprecedented number of loan defaults, the crisis uncovered a shocking level of unrestrained lending and excessive risk taking. by Matt Cox.

Now that EFL has partnered with FICO to sell our alternative credit scores, we get a lot of questions from FICO’s clients. In this and the next few blog posts, I am going to address the most common ones. How Is EFL Different from Other Alternative Credit Scores ? What character traits are predictive of creditrisk?

What were some of the most interesting risk analytics topics last year? Judging from the views on the FICO Blog, risk professionals are keenly interested in new ways to approach risk analytics. A New Way to Score CreditRisk – Psychometric Assessments. Using Alternative Data in CreditRisk Modelling.

In a previous blog , I defined what is meant by a security or cybersecurity posture. You need to understand the liability and exposure to risk your business has and this cannot be achieved without accurate measurement. As my colleague Doug Clare wrote in his blog , connectivity creates aggregate risk. Creditrisk.

The updated model reflects the evolving credit landscape and credit behavior to help better inform a higher level of consumer creditrisk prediction. The validation results for FICO Score 10 T demonstrate improved creditrisk prediction for this segment of the population.

Home Blog Feed test Icing on the Cake: How the FICO Score and alternative data work best together Significant attention has been paid recently to the potential for use of alternative data to enhance the predictiveness and inclusiveness in credit scoring. More than 200 million U.S.

As artificial intelligence applications exploded last year, our blog posts on AI and machine learning drew thousands of readers. Indeed, taken together, they explored many aspects of Explainable AI and its applications, particularly in the area of creditrisk. Combining Machine Learning with CreditRisk Scorecards.

Modern day credit tech stack could revolutionize Supply Chain Financing, streamlining processes and enhancing financial mechanisms. This blog explores the challenges in supply chain financing and how M2Ps Credit Stack is addressing them to empower businesses. What is Supply Chain Financing?

If an applicant has a medium risk of synthetic identity fraud at point of origination, this riskassessment may increase over the course of several years as new data indicates the now customer is part of a fraud ring. Lastly, step 3 requires thinking big across the risk and the fraud continuum.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? In uncertain environments, lenders seek ways to address creditrisk management gaps likely to emerge with a potential recession.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? In uncertain environments, lenders seek ways to address creditrisk management gaps likely to emerge with a potential recession.

How data sharing can improve creditrisk decisioning. The launch of the Open Finance Framework by Bangko Sentral ng Pilipinas (BSP) in 2021 was a big step forward in driving financial inclusion for millions of Filipinos across the market who still do not have access to credit. FICO Admin. Wed, 10/03/2018 - 23:42.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for creditriskassessment. That’s because FICO® Scores are built to last. Ethan has a B.S.

The blog posted excerpts from an email reportedly sent by Amazon Business to U.S. In its email, Amazon Business assured that companies will receive payment no longer than seven days past-due, while the eCommerce conglomerate also assured sellers that it will handle creditriskassessment, billing and collection.

Posts dealing with debt collection were among the most popular on the FICO Blog last year, for obvious reasons. We did not assess how they might behave once the crisis that triggered their financial stress was starting to pass. Collections Analytics: Are We Missing The CreditRisk Revolution?

This confusion and inconsistency may be causing additional collection records on credit bureau reports. As a data scientist from FICO’s Scores organization, I feel it’s important to remind our blog readers that collection information on a credit bureau report has consistently been found to be a strong indicator of increased creditrisk.

We will dive into this further in future blogs so keep an eye out.). On the ‘opportunity’ side, I cited: The speed to powerful insights that ML offers, making it ideal for R&D efforts aimed at assessing new analytic challenges, and/or the potential of new data sources to add incremental lift.

Its biggest plan, reports said, is to use QuadMetrics’ capabilities in predictive analytics and riskassessment strategy to create an “enterprise security score” for business customers. QuadMetrics says it had achieved 90 percent accuracy in predicting the chances that a company will suffer a cyber attack. .

In our previous blog post I examined the shifting regulatory landscape, recent changes in bank overdraft program changes, and what’s next with regulations on overdraft. Banks can choose to assess a fee immediately (the current state) or within a defined period of time (i.e. Consider the following setting. post grace period).

FICO Fact: Can having no credit score be better for consumers than a low credit score? To avoid situations like this, it is critically important that credit scoring models are proven over time and based on sufficient data to reliably assess a consumer’s creditrisk in a way that doesn’t generate a low score.

Saudi Credit Bureau Delivers Access To Loans For Millions with Score. We have been on a journey in Saudi since 2011, to grow lending and increase financial inclusion through the adoption of advanced riskassessment tools,” said Swaied Alzahrani, CEO of SIMAH. How FICO Can Help Improve Your Ability To RiskAssess Customers .

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumer creditrisk. Which raises the question: Should rental data be widely reported to the three primary consumer credit agencies (CRAs)?

But as more providers take steps towards extending mobile phone leasing to underserved markets, new demographics and segments with thin credit files, while offering the lasts handsets and access to high-speed services, they face a multitude of challenges. He has a Master’s degree in Economics, with an emphasis in econometrics and game theory.

Home Blog Feed test ‘FICO Drift’: What Is It, and What Causes It? consumers’ credit scores were “inflated“ after a decade of economic growth and prosperity. We’ve addressed the topic in a blog post , which for those who have read this far, will sound quite familiar! Ethan has a B.S.

14% said the financial outlook for their company was very strong, and another 50% assessed the outlook as strong. Investors and other secondary market participants want a credit score that is predictive of creditrisk and proven over time. Greater volatility in the securitization market is anticipated this year.

Other expenditure blind spots, such as Buy Now Pay Later, can be removed through the use of digital income and expenditure assessments or Open Banking data. The value of emerging, non-traditional data sources should not be overlooked.

The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times.

FICO Fact: Can unconstrained AI/ML expand access to credit? Machine Learning is simply another analytic technique; one that can help produce highly predictive credit scores which must also be explainable, with two important caveats: . The use of Machine Learning must be balanced with deep domain expertise in creditrisk modeling.

FICO Score hitting a new high in 2018 or the use of machine learning to challenge the score - dominated reader interest on the Risk & Compliance blog in 2018. credit quality. Topics around the FICO® Score - whether it's about the average U.S. Here are the five posts with the most views. Average U.S. FICO Score Hits New High.

Reach out to your Solution Success Manager or Client Partner at FICO for a discussion and current state assessment if you need help completing this evaluation. If you have questions or are interested in discussing these insights in more detail, please contact me, Leanne Marshall, through comments on this blog or at leannemarshall@fico.com.

Amazon has also promised that it will handle creditriskassessment, billing and collection for its sellers. For all Pay by Invoice transactions, payment to you is guaranteed, even if the Amazon Business customer is late or defaults on their payment to Amazon,” the email stated, according to the blog.

Home Blog FICO Top 5 Scores Posts of 2022: Steady FICO Score, BNPL and Alternative Data 2022 marked the first year in over a decade the average FICO Score did not increase, while the industry’s attention remained on topics such as alternative data and BNPL. million previously “unscorable” consumer files.

Plenty still have siloed data across marketing, creditrisk, customer management, fraud, compliance, and collections operations. Importantly, when assessing whether a product represents fair value, market rates and prices for comparable products can be considered. FCA’s Consumer Duty Mandates Sharper Use of Technology.

In assessing the predictive value of new scores or new data, significant weight is given to model performance measures. I have seen studies claiming a creditrisk score can offer as much as 20% improvement in creditriskassessment over a predecessor model, as measured by relative improvement in Gini.

The “innovation” VantageScore claims can score more people is simply the weakening of credit score criteria. The minimum criteria needed to produce the FICO Score aren’t arbitrary — they are the result of decades of research into riskassessment. More detail and can be found in Figure 1.

Trust combines this fast onboarding journey with comprehensive riskassessment by using predictive models, analytics and parameters built into its decision engine. We combine risk management fundamentals with data science and customer segmentation to help us arrive at optimum risk outcomes,” said Lohia. “We

Reach out to your Solution Success Manager or Client Partner for a discussion and currect state assessment if you need any help completing this evaluation. If you have questions or are interested in discussing these insights in more detail please contact me, Leanne Marshall, through comments on this blog or at leannemarshall@fico.com.

It’s clear there are opportunities to provide convenient, competitive and desirable options for pay-in-four instalments, while still accurately assessing a customer’s ability to pay and analyzing precise exposure for at-risk consumer segments. chevron_left Blog Home. Tue, 07/02/2019 - 02:45. expand_less Back To Top.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content