This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A new report by Twimbit, a Singapore-based research and advisory firm, highlights the state of open finance in Southeast Asia, exploring the different factors such as regional integration, technological innovation, evolving business models, and API monetization that are fueling the growth of the sector.

But is the relevance of such a crisis relevant to finance professionals, or is this just an unfortunate occurrence that such workers will keep hearing about for the foreseeable future? All finance chiefs should stay well-informed and nimble in managing risks during this time. Being Proactive as Finance Professional During the Crisis 1.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The evolution of open banking into open finance, examining regional regulatory approaches and adoption trends. Why is it important?

Organization that are certified by CREST goes thorough assessments of their methodologies, quality assurance processes, and data security measures, offering assurance to clients seeking reliable and trustworthy security services. CERT-IN Empanelment : Recognized by the Indian government as a trusted security assessor.

In an era marked by rapid technological evolution, the finance function within businesses stands at the forefront of digital transformation in the Asia Pacific (APAC). This shift is not merely about adopting new technologies; it’s about reimagining the role of finance in driving future business success.

Although Vietnam’s digital finance market has seen rapid growth over the last few years, many consumers still struggle to access secure and high-quality financial services due to ineffective risk assessment systems. The post Fundiin Teams up With Visa to Enhance Credit-scoring Model appeared first on FF News | Fintech Finance.

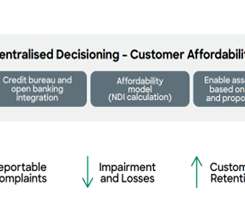

nearly three-quarters—financed through retail credit. These checks often lack the granular, real-time insights into income and expenses that lenders need to assess customers fairly. By elevating customer experience and refining credit assessments, the use of Open Banking helps retailers foster stronger brand loyalty.

Alternative Credit Scoring Models Fintech companies use data beyond traditional credit scores, such as transaction histories, online reviews, and even social media presence, to assess risk. Tala assesses creditworthiness through smartphone data, while Kiva uses peer-to-peer lending to connect small businesses with global investors.

Yield farming and liquidity mining have become key components of the decentralised finance ( DeFi ) ecosystem. However, the sustainability of these high yields often depends on several factors, including market demand and tokenomics. If the demand for the platform’s services or tokens decreases, the APYs can drop quickly.

This is especially important as consumers demand more clarity and accountability from financial service providers. Evolution From Open Banking to Open Finance While PSD2 paved the way for Open Banking, PSD3 sets its sights on open finance by expanding access to a broader range of financial data, such as investment and insurance accounts.

Open banking and open finance promise significant benefits for consumers and businesses alike. But what do firms need to do to ensure they make the most of the next future of finance? Organisations must evaluate whether their in-house capabilities can truly match the pace of change and innovation that open financedemands.

For many accounting and finance professionals, being a chief financial officer (CFO) is a career highlight. Taking that next step towards the finance executive table, whether you have 10, 20, or even 30 years of expertise in finance, is no easy task. However, getting there is only the start of the journey.

However, a pressing issue demands our collective attention: the de-risking practices that are inadvertently crippling legitimate money service businesses (MSBs) and empowering black-market alternatives. This shift increases financial crime risk and erodes the efficacy of the UK’s AML and counter-terrorist financing (CTF) frameworks.

Artificial Intelligence (AI) is gradually revolutionizing various industries, including the field of accounting and finance. In a recent webinar sponsored by Datarails , the FP&A solution for Excel users, three distinguished finance leaders came together to discuss the impact of AI on corporate finance.

What's behind it, and why should CFOs and finance leaders care about it? Continue reading to learn what ESG reporting is, what's new with ESG reporting standards, why Finance teams should care, and the five benefits of aligning ESG and financial reporting. But CFOs and Finance teams are now starting to become involved.

Affirm underwrites every individual transaction before making a real-time credit decision and only approves consumers following an assessment that evidences their ability to repay. Consumers demand payment choice, flexibility and transparency at checkout, and Affirm delivers all three.

Every modern enterprise, regardless of size, requires finance software to manage various aspects of its financial health. However, with the abundance of finance software available today, selecting the right one can feel overwhelming.

Maturity in finance, particularly in FP&A, entails accepting complexity and expanding your capabilities. Tom continues, “They are leading with digital transformation and the requisite skills in their Finance and Accounting teams. This , video below encapsulates exactly how they feel.

In Southeast Asia, demand for digital lending solutions is on the rise, driven by shifts in customer expectations, regulatory changes, and heightened scrutiny of environmental, social and governance (ESG) considerations.

Since vIBANs are often treated as extensions of master accounts rather than independent relationships, firms fail to apply appropriate risk assessment frameworks. Real-time monitoring tools must be implemented to detect suspicious patterns, while AI-driven risk assessments can help identify emerging threats in cross-border transactions.

Most, are on the heightened customer expectations, increasing regulatory demands, and intense competition from digital-native challengers. Closer to home, Asia Pacific is leading the global finance cloud market in growth , with a forecast CAGR of 17.5% The answer, however, is simple. billion in 2025, up from USD $595.7

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embedded finance has to offer and overcome across the globe.

The collaboration helped evaluate potential approaches for identifying and addressing operational challenges in digital finance, including monitoring for issues that may emerge throughout the lifecycle of digital assets. Transparency and risk management are critical to supporting institutional engagement in tokenized finance.”

The forum’s theme, “ Boost Resilience, Reshaping Smarter Finance Together ,” encapsulates the industry’s collective ambition to navigate the challenges of an uncertain future through technological excellence and collaborative innovation. This gathering comes at a pivotal moment.

It's the most reliable way to get to the heart of your company's data demands and devise a strategy for the future. Whatever use cases the company has established, the finance professional's job is to assess the financial effect and return on investment of possible data initiatives in relation to the company's strategic objectives.

Decades ago, asset-based finance developed a nasty reputation. As a financing tool that requires business owners to place valuable assets — whether working capital or physical — up for collateral, asset-based financing (ABF) was often viewed as a solution to a dire problem when no other options were available.

Often, talk around SME finance centres on access to loans. Common issues include: Standardised risk assessments that overlook innovative or early-stage firms. Alternative finance options and commercial credit data sharing initiatives can help modernise credit evaluation, but awareness among SMEs remains low. Representing 99.9%

of this (nearly three-quarters) financed through retail credit. These checks also often lack the granular, real-time insights into income and expenses that lenders need to assess customers fairly. By elevating customer experience and refining credit assessments, the use of open banking helps retailers foster stronger brand loyalty.

Participants tackled five central themes: underleveraged innovation, the operationalisation of AI, regulatory challenges, the evolution of embedded finance, and strategic risk planning for 2025 and beyond. To meet this demand, OpenPayd has expanded its licensing infrastructure to include virtual asset service provider (VASP) capabilities.

As 2024 approaches, CFOs need to assess their 2023 achievements and plan for the coming year. Revamp Finance Operations As the , CFO's responsibilities grow, the finance function's impact also expands. Managing vast amounts of data, finance leaders now play a crucial role as data custodians.

European banks and financial services players have fallen significantly behind those in the US in the embedded finance race, according to new research by payment consultancies PSE Consulting and The Strawhecker Group (TSG). The payment consultancies found a significant gap in the use of embedded finance in the US compared to Europe.

“One-click” loans become reality through instant credit assessments. Data Analytics: Making Informed Decisions Data is now the lifeblood of modern loan management, empowering lenders with insights to assess creditworthiness, predict risk, and personalize loan terms. AI is poised to revolutionize loan origination.

Additionally, the event will provide a forward-looking perspective on the future of BNPL and its potential to reshape consumer finance and the wider payments industry. The event will explore cybersecurity careers within the banking, finance, and fintech sectors, particularly in response to the increasing frequency of cyber attacks.

Brankas, an open finance platform provider, has launched a solution aimed at simplifying open banking compliance for financial institutions in the Asia-Pacific region. Brankas’ platform addresses key compliance requirements such as API standardization, authentication, and encryption. Brankas and ADVANCE.AI Featured image credit: ADVANCE.AI

The chill has been taken out of the industry as investors regain confidence, new startups can launch with less risk, and established players are doubling down on new technologies to meet evolving customer demands. From fresh AI applications to the new uses for embedded finance, fintech is experiencing a renewed momentum.

As such, trade finance will be an important piece of the global recovery puzzle. Connecting B2B vendors to financing on their unpaid invoices can grant them the financial stability they need to keep trade flowing, but it comes with its own set of challenges — both for the vendor and financiers. With a trade finance gap as large as $1.5

However, PSPs must ensure their systems and processes support this capability, which may involve implementing blockchain analytics tools and strengthening compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) regulations. Why is it important?

According to the British Business Bank, nearly half (48%) of all UK SMEs with employees sought external finance in 2023, demonstrating the high demand for solutions like Paycorp’s. The post Paycorp Expands Embedded Business Funding into UK appeared first on Fintech Finance.

One way to secure funding is to use invoice financing. In an interview with PYMNTS, CEO Johannes Brouwer said that for smaller firms seeking access to financing as they look to grow operations, the process has typically been time-consuming and expensive. Many companies, he told PYMNTS, rely on private lending.

In addition, ransomware attacks and associated demands for payment, which are almost exclusively denominated in CVC, are increasing in severity.". The rationale for the new regulations, as the government laid out in the Federal Register, is that "U.S.

HSBC is expanding the trade financing solutions it offers for businesses trading on e-commerce platforms in mainland China and Hong Kong, in partnership with Dowsure Technologies. HKECIC will provide insurance coverage for the loan portfolio within its merchant financing programme.

In response, regulatory bodies like the Financial Conduct Authority are tightening anti-money laundering (AML) and counter-terrorism financing (CTF) measures, levying steep penalties for non-compliance. This urgency often leads organisations to choose vendors who claim to deploy solutions swiftly to meet compliance demands.

Covid to Cost-of-Living: Assessing Affordability in Uncertain Times. Food and fuel prices are soaring day by day and more than a third of adults in the UK are now struggling financially, with many more experiencing a significant squeeze on their finances for the first time in their lives. Despite this, demand for housing continues.

Many corporate leaders are now wrestling with how to keep up with demand as the US economy recovers faster than anticipated. Fitness organizations, for example, that used to offer physical equipment now sell monthly memberships to online lessons that users can watch on-demand from the comfort of their own homes.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content