This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, with this widespread adoption comes an equally significant risk which is the growing threat of data breaches and payment fraud. This is where PCIDSS (Payment Card Industry Data Security Standard) compliance becomes essential for Australian businesses. The latest version PCIDSS v.4.0

That’s where PCIDSS, PSDS2, and AML come in. Non-compliance, on the other hand, can lead to data breaches and legal troubles. PCIDSS: Safeguarding cardholder data If you handle card payments, PCIDSS compliance is non-negotiable. What is PCIDSS? You know this already.

You can also check out the PCI at a glance infographic for a quick overview. For simplicity, I will just refer to PCIDSS standards as PCI for the rest of this article. What is PCI again? In the past, Ive written about how to achieve and maintain PCI compliance. What changed in PCI 4.0?

The Payment Card Industry Data Security Standard (PCI-DSS) is a set of global standards developed to safeguard cardholder data. Compliance ensures robust security practices to prevent breaches and protect sensitive payment card data. Staying up-to-date with PCI-DSS compliance should be a top priority.

How tokenization applies to being PCI compliant and meeting the 12 PCIDSS requirements. Minimize or Eliminate Compliance Requirements While necessary, compliance, particularly, the 12 PCIDSS requirements , are a significant burden for organizations to bear. This can be inconvenient and unwieldy.

Stage 2: Authentication and Security To prevent fraud, security measures are incorporated: EMV Chip Technology : EMV chips provide dynamic encryption for each transaction, making it harder to counterfeit cards. Tokenization : Converts sensitive card data into a unique token, reducing the risk of data breaches.

Click to Pay is based upon global EMV Secure Remote Commerce (SRC) standards, which include security measures like tokenization , multi-factor authentication , and 3D Secure protocols. The customer will then input the passcode to complete the authentication process. It is also built to be super secure.

Businesses using self-hosted gateways must handle data security measures and comply with industry standards like PCIDSS. Payment processors that comply with this regulation protect businesses from data breaches and credit card fraud. But with more control comes great responsibility.

It also ensures that data security best practices, particularly PCIDSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data. A good example is restaurants that accept customer takeout orders over the phone.

Moreover, network tokenisation reduces the regulatory burden by eliminating the need to store sensitive card data, supporting the Payment Card Industry Data Security Standard (PCIDSS) compliance and lowering the risk of data breaches.

As data breaches evolve and advance, a robust payment processing system that protects sensitive financial information is essential. PCI-compliant Sage 100 payment software providers must maintain strict security standards and enforce various measures, such as advanced encryption and tokenization, to safeguard sensitive payment data.

Measures such as encryption, tokenization, and fraud detection are vital for protecting payment transactions from cyber threats, fraud, and data breaches. 3D Secure (3DS) authentication and AI-powered fraud detection add extra security layers. Security is the core of any payment processing system.

Market dynamics signal a fundamental shift Five transformative technologies are redefining POS capabilities: SoftPOS, Cloud-based systems, Mobile solutions, Self-service kiosks, and Biometric authentication. Biometric authentication remains nascent but shows promise for premium applications. Average global data breach costs hit US$4.9

This tokenization keeps the sensitive card information off your servers, reducing the risk of a data breach and easing PCIDSS compliance. Ensure High-Level Security and Compliance Payment data breaches destroy customer trust and can bankrupt small businesses. Smart research now prevents costly mistakes later.

It spots anomalies before a threat becomes a breach. AI is enabling: Biometric authentication that eliminates passwords and PINs. AI enables real-time defence by continuously learning from behavioural patterns, device signals, geolocation, and transaction metadata. Predictive analytics identify emerging fraud patterns.

Strong encryption builds trust with customers and reduces the risk of data breaches. These gateways handle all payment details, providing a secure system that minimizes the risk of data breaches. Fraud detection and prevention are critical features of a payment gateway. How much does a payment gateway cost?

PCI compliance and security Integrated payment gateways typically come with built-in security features such as full compliance with Payment Card Industry Data Security Standards (PCIDSS) , tokenization, and encrypted data transmission.

Acumatica payment providers should comply with legal and regulatory requirements like Payment Card Industry Data Security Standards (PCI-DSS) , which safeguard payment data by implementing various security protocols. 3D Secure authentication requires an additional verification step during a credit card transaction.

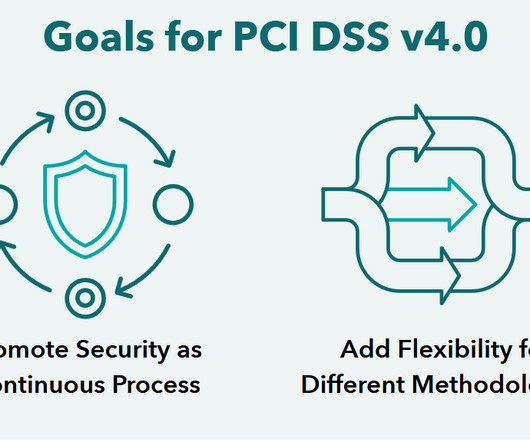

In our last discussion, we explored the evolution of Requirement 1 in the transition from PCIDSS v3.2.1 As we continue our exploration of the updated PCIDSS v4.0, These requirements’ main objective is to safeguard sensitive cardholder information and mitigate data breaches. to PCIDSS v4.0:

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

The PCIDSS Checklist is a crucial first step in securing your business. It’s a tool that helps businesses ensure they’re meeting all the requirements of the Payment Card Industry Data Security Standard (PCIDSS). To get started on your journey towards PCIDSS compliance, we recommend visiting the PCIDSS v4.0

Work with PCIDSS Compliant Vendors While the PCIDSS (Payment Card Industry Data Security Standard) is not a legal requirement, it is a sign that an organization or a product is up to par when it comes to combating common cyber threats.

In our ongoing series of articles on the Payment Card Industry Data Security Standard (PCIDSS), we’ve been examining each requirement in detail. Today, we turn our attention to Requirement 8: Identify Users and Authenticate Access to System Components. Changes Overall Focus Strong emphasis on eliminating shared accounts.

In our exploration of PCIDSS v4.0’s It boils down to minimizing the risk of data breaches and maximizing the security of cardholder information. This reduces the potential damage in case of a data breach. Changes in Requirement 3 from PCIDSS v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0

As more consumers gravitate online, they risk putting more sensitive authentication data and financial information on the internet. This is why PCIDSS compliance is critical. In this article, we’ll discuss why your business needs to ensure PCI compliance and what the 12 PCIDSS v4.0

Today, the framework introduced in the early 2000s outlines 12 PCI requirements that merchants must satisfy to process credit card transactions on the card networks. Nearly 20 years later, with more than 300 requirements and sub-requirements, PCIDSS continues evolving. Don't, however, let the term "merchants" fool you.

Driven by big breaches like the Equifax incident, all stakeholders in card payments will have to demonstrate multi-factor authentication, writes Michael Magrath, director of global regulations and standards at VASCO.

TL;DR The PCIDSS determines security protocols and sets the standards for payment security. It’s also critical to ensure card information is protected from data breaches with secure encryption and cybersecurity standards in place. How do two-factor authentication and “3-D secure” protect payment information?

According to a Verizon report , over 80% of hacking-related breaches are due to compromised passwords. In such attacks, cybercriminals exploit weak or reused passwords to breach multiple accounts, leading to significant data breaches and financial losses. PCI PIN and PCIDSS: Standards for securing payment card data.

TL;DR PCI compliance is essential because it helps prevent data breaches, ultimately cultivating customer trust. There are 12 requirements under PCIDSS, divided into six major categories. What is PCI Compliance? PCIDSS stands for “Payment Card Industry Data Security Standards.”

Security, Compliance, and Regulatory Risk: Cybersecurity risk involves the threat of data breaches and unauthorized access to sensitive payment information. The first step is implementing robust authentication processes, including multi-factor authentication, biometric verification , and tokenization , to enhance user access security.

PCIDSS compliance, a global framework, mandates specific requirements and best practices for maintaining credit card data security. Enter the PCIDSS compliance. The PCI Security Standards Council (PCI SSC) has robust measures to protect cardholder information and prevent unauthorized access, fraud, and data breaches.

Enter the Payment Card Industry Data Security Standard (PCIDSS): a comprehensive framework that sets forth stringent rules and regulations to ensure the secure handling, processing, and transmission of cardholder information. As we approach the highly anticipated release of PCIDSS 4.0 a notable change is on the horizon.

Feedback came from 700 firms participating in the council’s network, along with industry reports on data breaches. A significant change in PCIDSS 3.2 includes multi-factor authentication as a requirement for any personnel with administrative access into environments handling card data. A significant change in PCIDSS 3.2

The purpose of a PIN is to authenticate the identity of the cardholder during a transaction. Mobile wallets using biometric authentication generally bypass the need for a PIN. Terminals should be PCIDSS (Payment Card Industry Data Security Standard) compliant. What is a PIN?

The primary security standards that payment systems typically adhere to include: Payment Card Industry Data Security Standard (PCIDSS): PCIDSS sets forth requirements for securing payment card data, including encryption, access control, network monitoring, and regular security testing. Two-Factor Authentication (2FA).

Look no further than the US presidential debates , where our two candidates have highlighted the need to address hackers, security breaches and even foreign nations that may be using sophisticated cyber tactics to influence the outcome of the upcoming November elections. These days, cybersecurity is a hot-button issue in policy circles.

McAfee Labs recently published its 2018 Threats Predictions report , and after a year of high-profile cyberattacks and data breaches, analysts say the threat won’t let up in the new year. If there’s one thing the enterprise has learned this year, it’s that a data breach can happen to any business — including small businesses (SMBs).

The Payment Card Industry Data Security Standard (PCIDSS) plays a crucial role in protecting cardholder data for businesses that accept credit card payments. Adhering to these guidelines is essential for businesses to ensure the safe handling of credit card data, helping to minimize the risk of fraud and security breaches.

There are various methods of enforcing data security, such as data masking, encryption, authentication, and data tokenization. Besides the enhanced data security, other benefits include reduced risk of breaches, easier regulatory compliance, and compatibility with legacy systems. Let’s get started.

Biometric authentication, such as fingerprint or facial recognition, is increasingly used to verify the identity of the user, adding a personal layer of security to the transaction process. Integration of Biometric Authentication : Security concerns are paramount in the realm of mobile payments.

The API authenticates the request, forwards transaction details for authorization by the respective banks, and processes the transfer of funds upon approval. Authentication : The payment gateway API authenticates the request using API keys or OAuth tokens to ensure it originates from a trusted source.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content