This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Highlights Contactless tap, familiar ease Consumers pay instantly from their bank accounts without redirects or entering card details. Strong ConsumerAuthentication Each transaction is securely authorized via biometric authentication, with tokenisation and encryption protecting all payment data.

The customer expects processes that are smooth and swift — and if a transaction does not meet those expectations, the consumer will likely continue down the line to the next provider who can give them that experience. This means authenticating a consumer has turned into something of a tricky and delicate process.

Biometrics promise to take a larger role in authentication security in 2019, helping to stop online fraud and bringing speed, efficiency and security to transactions ranging from QSR mobile-order ahead to airport car rentals. Google was granted a motion for summary judgement by U.S. Larger Trends.

The foreseeable changes stem from the already delayed strong customer authentication (SCA) regulations that are due to go into effect in Europe by the end of the year. Under the new SCA rules, merchants will need to be able to securely authenticate every customer before authorizing eCommerce transactions. The Path Ahead.

Banks can use this information to define rule sets to increase monitoring or do proactive customer outreach in case of balance inquiries, helping to head off criminal activity before it results in losses. We saw that in 2022, 58% of the attempted transactions in fraud cases were balance inquiries. Debbie holds a B.A.

Putting flexible business rules into place can be effective, too, limiting how much people can transfer out of their accounts. To attack fraud in its planning stage – indeed, at any stage of attack – Kraus advises following this golden rule: “Assume you are being attacked all the time.”. Proactive Fraud Prevention.

Separate regulations coinciding with PSD2 could also challenge FIs’ process of implementing the new rules, analysts warned. The only way to obviate these difficulties is to start implementing the third-party interface and strong customer authentication as soon as is possible.”. It won’t be easy, though.

And it’s been transparent to policymakers since 2012, when there became a source of truth called the CFPB consumer complaint database, that credit reporting agencies are one of the top three places that consumers say they consistently feel the most pain. I think we all know the answer to that question now.

banks have to analyze AML regulations before even beginning to innovate, and the rules in question change often. Working consumer access into the already-fraught field of AML protection creates problems, too, as banks need to be sure they are accurately authenticating the customers in question before sharing data with potential fraudsters.

There isn’t a payment problem at the federal government level, he said, there are 85 payment problems — one for each individual department that has its own payment scheme with its own processes, rules and antiquated technology stack supporting it. COBOL , anyone?). “It It shouldn’t be that way; I don’t know why it is that way.

People can use [Sapphire] to validate information, correlate information to prediction services and then, if they want to, step up and do secondary authentication with physical documentation,” he said. The single API means its customers can validate their consumers’ personal identification information without having to use multiple vendors.

First, think about using separate rules and strategies to address the different exposure types. Her roles have included developing a consumerauthentication solution for Experian and managing credit and identity theft management applications. Debbie holds a B.A.

Finally, banks can use geographically based rules to help combat skimming fraud. Her roles have included developing a consumerauthentication solution for Experian and managing credit and identity theft management applications. Debbie holds a B.A.

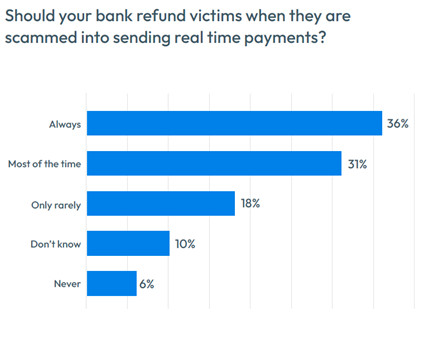

Consumer defection and acquisition are costly, as are customers who may maintain but cease to use an account. 23% Complaining to regulators: Nearly a quarter (23%) of consumers will complain to regulators if dissatisfied. In most cases, customers feel that banks should reimburse them when scams occur. Debbie holds a B.A.

As far as Trulioo’s presence on that buildout, Ufford said the work is akin to building out the telephone poles that carry the wires and, ultimately, the data — routing the information that allows networks to scale with operating rules, standards, codes of conduct and governance that will transform digital identity verification.

While advancements to digital commerce and authentication technology have revolutionized a number of industries, one where their influence is perhaps most visible in the travel sector. The solution approaches digital authentication by flagging anomalies when consumers, issuers and merchants all come together, online, to do business. “3D

Use a “cool off period” for large payments Survey responses: Nearly half (45%) of consumers worldwide think enforcing a “cooling off period” for larger payments is an improvement banks could make to combat scams. In Indonesia , Malaysia , and South Africa , however, 54% or more of consumers like the idea. Debbie holds a B.A.

Securely registering and authenticating trusted agents: The program will require trusted AI agents to be registered and verified, after which they will be able to make secure payments on behalf of their users.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content