This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is where PCIDSS (Payment Card Industry Data Security Standard) compliance becomes essential for Australian businesses. In todays article, we are going to learn how PCIDSS compliance protects businesses from data breaches. The latest version PCIDSS v.4.0 This is where the PCIDSS comes into play.

In our last discussion, we explored the evolution of Requirement 1 in the transition from PCIDSS v3.2.1 As we continue our exploration of the updated PCIDSS v4.0, With the impending retirement of PCIDSS v3.2.1 Modification to Requirement 2 from PCIDSS v3.2.1 to PCIDSS v4.0:

That’s where PCIDSS, PSDS2, and AML come in. PCIDSS: Safeguarding cardholder data If you handle card payments, PCIDSS compliance is non-negotiable. What is PCIDSS? PCIDSS stands for Payment Card Industry Data Security Standard. You know this already.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

You can also check out the PCI at a glance infographic for a quick overview. For simplicity, I will just refer to PCIDSS standards as PCI for the rest of this article. What is PCI again? In the past, Ive written about how to achieve and maintain PCI compliance. Timeline PCI version 4.0

The PCIDSS Checklist is a crucial first step in securing your business. It’s a tool that helps businesses ensure they’re meeting all the requirements of the Payment Card Industry Data Security Standard (PCIDSS). To get started on your journey towards PCIDSS compliance, we recommend visiting the PCIDSS v4.0

Welcome back to our ongoing series on the Payment Card Industry Data Security Standard (PCIDSS). Networks that store, process, or transmit cardholder data naturally fall within the PCIDSS scope and must be assessed accordingly. PCIDSS v3.2.1 PCIDSS v4.0 Testing Procedures: 4.2.1.1.a

In our ongoing series of articles on the Payment Card Industry Data Security Standard (PCIDSS), we’ve been examining each requirement in detail. Today, we turn our attention to Requirement 8: Identify Users and Authenticate Access to System Components. Changes Overall Focus Strong emphasis on eliminating shared accounts.

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0 c: Confirm that software applications comply with PCIDSS. - c: Confirm that software applications comply with PCIDSS. - In PCIDSS v4.0, PCIDSS v3.2.1

Work with PCIDSS Compliant Vendors While the PCIDSS (Payment Card Industry Data Security Standard) is not a legal requirement, it is a sign that an organization or a product is up to par when it comes to combating common cyber threats.

As more consumers gravitate online, they risk putting more sensitive authentication data and financial information on the internet. This is why PCIDSS compliance is critical. In this article, we’ll discuss why your business needs to ensure PCI compliance and what the 12 PCIDSS v4.0

The Payment Card Industry Data Security Standard (PCI-DSS) is a set of global standards developed to safeguard cardholder data. Staying up-to-date with PCI-DSS compliance should be a top priority. This guide will break down what you need to know about PCI-DSS compliance. PCI-DSS version 4.0,

In our exploration of PCIDSS v4.0’s So, what’s the purpose of Requirement 3? Changes in Requirement 3 from PCIDSS v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0 a Review policies and interview staff at issuing entities to confirm justified storage of sensitive authentication data.

How tokenization applies to being PCI compliant and meeting the 12 PCIDSS requirements. Minimize or Eliminate Compliance Requirements While necessary, compliance, particularly, the 12 PCIDSS requirements , are a significant burden for organizations to bear. This can be inconvenient and unwieldy.

Key security features include: Advanced Machine Learning Fraud Detection: Prevent unauthorized access with IP Allowlisting & Multi-Factor Authentication (MFA), and monitor suspicious activity with user behavior analytics. Runa Assure safeguards the entire payouts journey so businesses can protect their recipients, revenue, and reputation.

Ensure the gateway offers PCIDSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. A payment gateway is a tool that allows merchants to authenticate and receive payments from their customers electronically. Learn More What is a Payment Gateway?

Although BINs play a critical role in how payments are processed and authenticated, they often go unnoticed by the average consumer or merchant. Card Verification and Authentication : BINs support the verification process by providing immediate access to the issuing institution’s information.

Know Your Customer (KYC): This check involves verifying government-issued IDs, business licenses, and ownership structures to confirm the merchants legitimacy and authenticity. Ensuring adherence to legal and regulatory standards, such as PCIDSS (Payment Card Industry Data Security Standard) requirements.

Stage 2: Authentication and Security To prevent fraud, security measures are incorporated: EMV Chip Technology : EMV chips provide dynamic encryption for each transaction, making it harder to counterfeit cards. Authentication 0.5 – 2 seconds Verification of cardholder identity via EMV, biometrics, or token.

Today, the framework introduced in the early 2000s outlines 12 PCI requirements that merchants must satisfy to process credit card transactions on the card networks. Nearly 20 years later, with more than 300 requirements and sub-requirements, PCIDSS continues evolving. Don't, however, let the term "merchants" fool you.

TL;DR The PCIDSS determines security protocols and sets the standards for payment security. How do two-factor authentication and “3-D secure” protect payment information? Multi-factor authentication (MFA) adds additional layers of security by requiring additional verification during the transaction process.

Click to Pay is based upon global EMV Secure Remote Commerce (SRC) standards, which include security measures like tokenization , multi-factor authentication , and 3D Secure protocols. The customer will then input the passcode to complete the authentication process. It is also built to be super secure.

Use multi-factor authentication (MFA) for SWIFT interfaces and applications. We are also offering AuditFusion360 a one-time audit service for all your compliance needs, including SWIFT CSP, PCIDSS, SOC 2, GDPR, ISO 27001, and more. Use surveillance and access controls for server rooms and data centers.

Businesses using self-hosted gateways must handle data security measures and comply with industry standards like PCIDSS. For eCommerce payment systems, these measures include two-factor authentication, fraud filters, real-time transaction monitoring, card verification value, device fingerprinting, and address verification system.

PCIDSS compliance, a global framework, mandates specific requirements and best practices for maintaining credit card data security. Enter the PCIDSS compliance. The PCI Security Standards Council (PCI SSC) has robust measures to protect cardholder information and prevent unauthorized access, fraud, and data breaches.

Moreover, network tokenisation reduces the regulatory burden by eliminating the need to store sensitive card data, supporting the Payment Card Industry Data Security Standard (PCIDSS) compliance and lowering the risk of data breaches.

TL;DR PCI compliance is essential because it helps prevent data breaches, ultimately cultivating customer trust. There are 12 requirements under PCIDSS, divided into six major categories. What is PCI Compliance? PCIDSS stands for “Payment Card Industry Data Security Standards.”

(The Paypers) PCI Council has released PCIDSS 3.2 compliance standards which include requirements that merchants and banks must implement in strong encryption and multi-factor authentication.

Card-on-file transactions are becoming increasingly popular, and tokenisation is critical to meet PCI/DSS compliance and prevent the risk of storing sensitive card data. For manual card provisioning, implementing robust step-up authentication processes is crucial.

The first step is implementing robust authentication processes, including multi-factor authentication, biometric verification , and tokenization , to enhance user access security. Secure Network Configurations Configuring secure networks is fundamental to PCIDSS compliance.

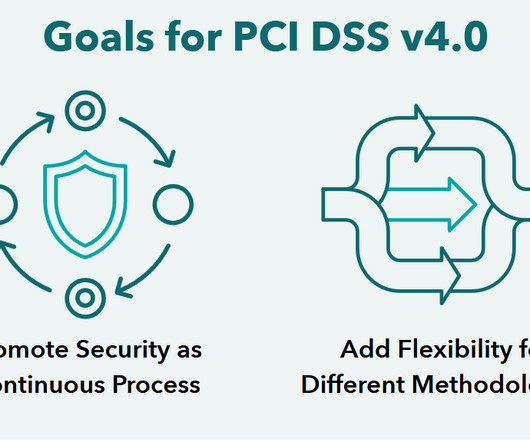

Enter the Payment Card Industry Data Security Standard (PCIDSS): a comprehensive framework that sets forth stringent rules and regulations to ensure the secure handling, processing, and transmission of cardholder information. As we approach the highly anticipated release of PCIDSS 4.0 a notable change is on the horizon.

Encryption and transfer of payment information The payment gateway that underpins your checkout page will now encrypt the customers payment details as stipulated by industry data security regulations like PCIDSS (Payment Card Industry Data Security Standard) before transferring the data to your payment processor.

Those vendors must also be compliant with both the company’s own program standards and the Payment Card Industry Data Security Standards (commonly known as PCIDSS). Finally, said the blog post, the registry also names those providers that have proven to be early adopters of the most recent version of the PCIDSS 3.2,

Multi-Factor Authentication (MFA) Implementing multi-factor authentication (MFA) adds an extra layer of security to the authentication process. PCI PIN and PCIDSS: Standards for securing payment card data. ISO27001: An international standard for information security management systems.

He noted that Scalefast must ensure GDPR and Payment Card Industry Data Security Standard (PCIDSS) compliance (the firm has a dedicated team in place to handle attacks or chargebacks), without any action needed from the D2C firm itself.

It also ensures that data security best practices, particularly PCIDSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data. The company facilitates the transfer of information and funds between the customer’s bank and your business’ bank.

This tokenization keeps the sensitive card information off your servers, reducing the risk of a data breach and easing PCIDSS compliance. Data is Encrypted & Tokenized Immediately after submission, the payment gateway encrypts the card data and replaces it with a token—a random, one-time-use ID.

Use multi-factor authentication (MFA) for SWIFT interfaces and applications. We are also offering AuditFusion360 a one-time audit service for all your compliance needs, including SWIFT CSP, PCIDSS, SOC 2, GDPR, ISO 27001, and more. Use surveillance and access controls for server rooms and data centers.

.” In the Philippines, The Philippine Statistics Authority in partnership with the Department of Information and Communications Technology, launched the Digital National ID this June, together with authentication platforms, National ID eVerify and National ID Check.

AI is enabling: Biometric authentication that eliminates passwords and PINs. From Payments to Experiences: What the Future Looks Like The future of payments isn’t just faster—it’s intelligent, anticipatory, and invisible. Proactive engagement , reminding users of bill deadlines or offering personalised credit.

Fraud prevention measures, such as tokenization and multi-factor authentication, add layers of security to verify transactions and protect against unauthorized use of payment credentials. Today, most mobile wallets are already using biometric authentication, requiring the user to scan their fingerprint before the wallet can be opened.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content