This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Every swipe or tap of a creditcard comes with processing fees that can hinder a businesss profitability if not properly managed. This article will provide helpful strategies for merchants to offset these fees to minimize the costs of accepting creditcard payments. These fees typically range from 1.5%

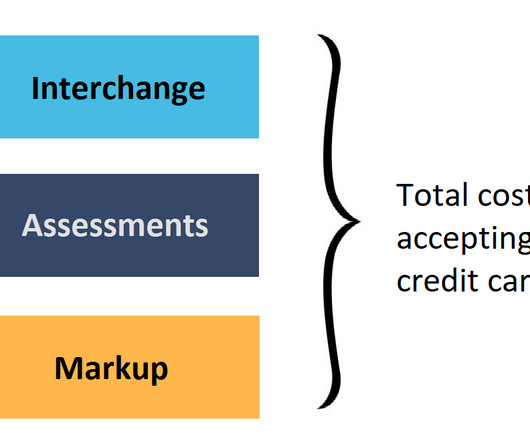

Interchange is the fee that creditcard companies like Visa and Mastercard charge businesses to accept their cards. In this article, we will break down creditcard interchange fees so you will know exactly how much you’re spending when running your business. How much does interchange cost?

As businesses navigate creditcardprocessing fees, zero costcreditcardprocessing has emerged as a valuable alternative. This option focuses on eliminating processing fees for the merchant by passing them onto customers, a practice thats steadily gaining traction.

Creditcards remain a favored way of making payments among customers. Purchase volumes through creditcards jumped 51% between 2015 and 2021. However, the idea of applying a creditcard surcharge to offset the processingcost of creditcards has always been a hotly debated topic.

Creditcards remain a favored way of making payments among customers. Purchase volumes through creditcards jumped 51% between 2015 and 2021. However, the idea of applying a creditcard surcharge to offset the processingcost of creditcards has always been a hotly debated topic.

Creditcard surcharges are increasingly becoming a fact of life. Industry data shows that 9 out of 10 creditcard users say they don’t want to pay surcharges but do it anyway. This is good news because it means you won’t have to inflate your base prices to cover payment processing fees.

Did you know that in 2021, merchants ended up paying a whopping $105 billion in creditcardprocessing fees? Even though they’re one of the most popular payment options today, accepting creditcards at your business can turn out to be a significant expense. to their payment processing company.

Passing creditcard fees onto customers has been hotly debated , but most of the country has agreed: Creditcard surcharge should be available to merchants. TL;DR Surcharging allows merchants to pass on creditcard fees. What is CreditCard Surcharging? There’s no way around it.

Creditcards are incredibly popular, and it’s easy to see why: they’re convenient and accepted nearly everywhere. But as great as they are for consumers, merchants know that accepting creditcard payments comes with added costs in the form of processing fees. Creditcard surcharging is legal in most U.S.

This article covers current statistics and general information of payment processing across the globe for merchants. Payment Process Fees Differ by Region The global overall average fee for processingcreditcard transactions in 2024 is approximately 2.4% Unlike Europe, where interchange fees are capped at 0.3%

One way to do that—though often overlooked—is to optimize their payment processing to reduce fees associated with creditcard purchases. Card companies like Visa, Mastercard, Discover, etc. charge interchange fees which, on top of other creditcardprocessing fees, can eat away at your profits.

Looking for a Printable creditcard fee sign ? Download PDF × With the prevalence of creditcard use in 2024 comes the often-overlooked detail of physical creditcard surcharge signs, which provide transparency of the fees merchants charge their customers to use creditcard payments to purchase.

In the complicated world of payment processing, understanding the nuances of debit card and creditcard payments, along with associated processing fees, is essential for businesses. After all, there are many more payment options available than ever before, and each comes with differing costs and technology needs.

When it comes to accepting payments, businesses often grapple with the costs of creditcardprocessing fees. The question “Is it legal to charge a creditcard fee?” Card types The type of card used in a transaction can dictate whether a surcharge is permissible.

In an era defined by digital transactions and cashless payments, the process of paying for goods and services is more convenient, and increasingly reliant on creditcard transactions. However, as the popularity of creditcards and digital wallet payments continues to surge, the costs associated with accepting them also do.

This may be concerning for certain types of businesses as they need to spend more to processcredit and debit card payments as compared to cash. Clearly, the monthly fees that businesses typically pay to accept card payments can eat away a significant portion of their revenue and overall profits.

While wire transfers and checks are quite common, the corporate creditcard market is projected to have a compound annual growth rate (CAGR) of 7.3% by 2026 , so we’ll likely see more creditcard use in the business sector. ACH payments take up to three days to process and cost around 1% of the transaction with a $10 cap.

If your company accepts creditcard payments ( which it should ), chances are, you’re going to be affected by Visa’s interchange rates. cards currently in use. So it’s virtually impossible for a business to not accept Visa cards. TL;DR Interchange rates are the fees charged by creditcard networks.

But if you just want a quick overview, here it is: Interchange is one of the three core components of creditcardprocessingcosts. Common Categories Common categories are the ones youll regularly see on your creditcardprocessing statement. Along with assessments and processors markup.)

While its free mobile app and API integration make it flexible for many users, its limitations, such as a 15-page processingcap and strict API rate limits, can hinder large scale document processing. Creditcard integration: Syncs corporate card transactions for easy reconciliation.

transaction fees to cover interchange and other variable processingcosts. Bill.com (see also #13 Invoice2Go) FAB Score = 842 ( down 120 ) HQ: San Francisco Bay Area Founded: 2006 Raised $496M including $216M in its Dec 2019 IPO ( Crunchbase ) Annual revenue (TTM): $1.2B ( Yahoo ) Market Cap: $5.1B ( NYSE:BILL 15 Aug 24) down $3.3B

Key Takeaways √ Hidden charges in payment processing can dig into and erode your bottom line. Merchants can implement several best practices to avoid surprise processingcosts. 5 minute read Hidden charges in payment processing can seriously impact any merchant’s bottom-line revenues. The IRS Mandate.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content