This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The good old Need for Speed game is played in many industries, including card issuance. Cardissuers need for speed exists on several levels, and we at OpenWay see this firsthand, since our Way4 card management software is used by top banks, processors and fintechs around the world.

Cardissuerprocessors face integration, compliance, and fraud challenges but can stay competitive by streamlining processes and enhancing customer experiences. Read more

Interchange and assessment fees are set by card networks and are non-negotiable. Merchants can, however, negotiate with their payment processor to cut costs, tweak pricing, or secure better rates. Following are the key entities involved in credit card processing. Also known as card companies or cardissuers (e.g.,

Heres a simple breakdown: Interchange fees: Interchange fees go to the customers bank (the cardissuer). Assessment fees: These go to the card networks like Visa and Mastercard. Processor markup: This is the fee your payment processor (like Clearly Payments ) charges for facilitating the payment.

In payment processing, one component of the payment processing tech stack involving credit or debit cards is the Bank Identification Number or BIN. For payment processors and financial institutions, however, understanding BINs is essential for smooth transaction processing, security, and even risk management.

US-based card platform Highnot e has expanded its collaboration with Visa to include certification as Visa cardissuerprocessor under its fleet management solutions.

In this article, we’ll help you figure out which of them may be the best credit card processing companies for your business needs. TL;DR Processors act as the middleman between your customer’s card and your bank, but not all are created equal—some offer better service, pricing, and tools than others. Let’s get started.

Remember, chargeback fees can vary depending on the credit card networks and processors involved. Merchant Accounts Merchant accounts are specialized accounts established by merchants to facilitate credit card payments. These accounts are typically provided by acquiring banks or third-party payment processors.

In the payment processing industry , loyalty programs are seamlessly integrated with card transactions. Merchants leverage their payment processors to implement loyalty programs that track customer spending, reward purchases, and incentivize repeat business. These are particularly effective for credit card companies.

Managing fraud cases has been a top challenge for cardissuers, according to recent studies. Rising operations and outsourcing costs and burgeoning fraud recovery caseloads make it especially challenging for issuers to meet chargeback deadlines and avoid cardholder write-offs.

Merchants can end up paying high fees if they have many non-qualified transactions and payment processors may even abruptly change their classification criteria. The first key component is the transaction fee, which is the base cost merchants must pay for each credit card transaction.

Airlines, travel agencies, payments processors and cardissuers all need to recognize the role that speed, reliability and efficiency must be top of mind to maintain strong relationships with your customers. Innovations in the payments space are driving significant changes in the global travel industry.

The interchange fee usually includes a percentage of the card transaction value and an additional fixed charge. Payment processors usually tack on additional fees on top of interchange to compensate for their services (based on their pricing model ). Card networks typically use a combination of both when setting interchange fees.

began to grow and secure larger accounts, we realized the need to bring our card management capabilities in-house and work with an enterprise processor that could support us as we continued to scale up,” said Zach Johnson, Founder and CEO of dash.fi. . “As dash.fi

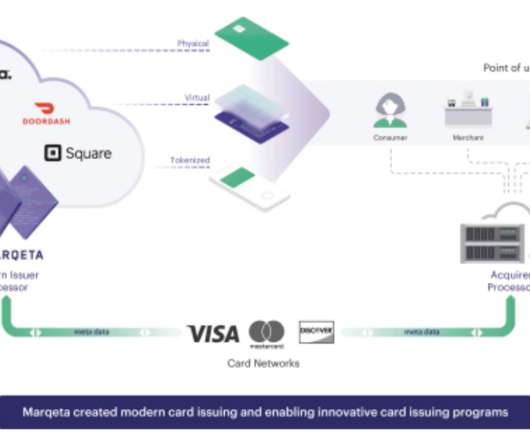

Marqeta , the global card issuing platform, debuted its new Tokenization-as-a-Service (TaaS) product, which allows cardissuers to access its tokenization technology, the Oakland, California-based company announced on Tuesday (Sept. It is used to instantly provision cards into a mobile wallet.

In a blog post this week, the director reiterated that payments processors, credit cardissuers and debt collectors are attracting scrutiny from his agency.

Visa interchange fees Mastercard interchange fees Discover interchange fees American Express interchange (OptBlue) What is the total cost of accepting credit cards? Set rate processing Subscription rate processing TL;DR Interchange fees are not collected by your payment processor or bank; they go directly to the card-issuing banks.

By understanding how these fees actually work, you can find leverage to negotiate with your credit cardprocessor and increase your profits. Understanding Credit Card Processing Fees There are three main components to credit card processing fees. Here’s an example.

Contact the Payment Processor Notify your payment processor as soon as possible. Advise them of the potential fraud and instruct them on the steps they should take, such as contacting their cardissuer to report the incident and potentially canceling their affected cards.

The customer will provide card information and transaction details on the checkout page of your website, and the data will also be captured by your online payment gateway. Authorization The credit card details captured by your POS or online payment gateway will be sent to your payment processor.

By integrating a payment processor, companies can improve cash flow, reduce administrative burdens, and gain better visibility into payment activities. Here are five common payment processing fees to be aware of: Credit card processing fees: Credit card processing fees are the fees merchants pay to accept credit card payments from customers.

Since MCCs offer several advantages for businesses and consumers, its essential to understand these benefits to help you make the most of your credit card transactions. This helps credit card companies and payment processors understand what kind of goods or services are being sold. MCCs help enforce these restrictions.

If you are one of the ten million-plus American businesses with a merchant processing credit card account, the chances are you are aware of an industry term known as interchange. Each new credit card transaction is assigned to what is known as a target interchange category. That’s the most important thing you need to know.

What are virtual credit cards? Virtual credit cards, as their name implies, are digital versions of credit cards. There is no physical card. Theyre linked to the customers account through their cardissuer and used (primarily) for online purchases. How do customers pay with a virtual credit card?

The payment settlement process involves various intermediaries, including the cardissuer, the acquiring bank, and the payment processor. The choice between gross and net settlements often depends on merchants’ preferences and payment processors’ policies. How long does it take for merchants to get paid?

Enfuce , the cardissuer and processor, has partnered with Swedish banking-as-a-service (BaaS) provider SEB Embedded and fintech Humla to launch a co-branded payment card, for customers of Hemkp , one of Sweden’s largest supermarket chains.

The cardissuer then contacts the merchant on behalf of their customer and requests that they refund the purchase price to the cardholder. If the cardissuer fails to make contact or the merchant does not refund the money, the cardissuer can reverse the charge on the cardholder’s statement.

Payment processors are financial institutions that help merchants accept credit, debit and other forms of electronic payments. In addition, some payment processors offer merchant services such as fraud prevention, customer management tools and reporting. The processor then settles the transaction with the cardissuer.

For example, there are approximately 300 acquiring banks in the US alone, even though there are around 200 issuerprocessors globally. . Financial institutions were the primary users of card-issuing technology, and their needs have remained the same over the years. The post Modern CardIssuer Marqeta Is Going Public.

Prosa has operations in eight Latin American countries and will provide mobile payment services to its customers, who comprise 95 percent of credit, debit and prepaid cardissuers in Mexico.

Global payments processor and cardissuer Mastercard and ecommerce payments service provider HyperPay have announced a partnership to expand digital payments in the MENA region.

PSCU has transformed its business model and evolved from a transactional processor and reseller of a platform partner’s products to an integrated, value-add financial technology solution provider, and we look forward to delivering the benefits of this scale to Primax clients,” he said, according to the press release.

When you run any BIN number through a checking system, you end up with accurate information about the geolocation, cardissuer, and card type. Since online banking systems have become more popular and virtual cards have become a norm, BIN numbers aren’t necessarily bank-issued. Next, there is clearance.

Prior to Mexico, NovoPayment has received certifications in Chile, Colombia, Ecuador, Peru and Venezuela as cardissuerprocessors. The direct partnership with Mastercard opens the door for service providers to collaborate on initiatives that drive value, innovation and seamless experiences in the evolving payment ecosystem.

Merusha Naidu, global head of partnerships at Paymentology “As a cloud-native cardissuer and processor, and one of the first issuerprocessors in Europe to connect to the Visa Cloud Connect endpoint in the EU, we believe the enablement of Visa services through AWS is a gamechanger,” said Merusha Naidu , global head of partnerships, Paymentology.

The merchant’s website will initiate a 3DS request with the customer’s cardissuer on the payment page. This is the first step of the process, and it is handled directly between the merchant and the payment processor. The payment processor will send a request for authentication to the customer’s cardissuer.

Core Payments Infrastructure At their heart, both Stripe and Adyen are payments processors – they enable businesses to accept a wide range of payment methods and get paid online (and offline). Stripe has countered by developing its own smart routing and “adaptive acceptance” algorithms, and by working with cardissuers.

This involves using a physical point-of-sale (POS) terminal to process card payments. How It Works The customer swipes, inserts, or taps their card on the POS device. The terminal communicates with the cardissuer to approve the payment. How It Works Customers enter their card details during checkout.

With greater digital dependency, having real-time purchase details is critical for consumers, merchants and cardissuers alike,” he said, according to the release. “We We continue to collaborate with industry partners to bring clarity and simplicity before, during, and after transactions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content