This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

PayMint , a leading financial technology company, has announced that it has obtained final approval from the CentralBank of Egypt to launch its first Meeza prepaid cards in partnership with Abu Dhabi Islamic Bank Egypt (ADIB-Egypt).

Paymob , the leading financial services enabler in MENA-P, announces it has been granted the Retail Payment Services License by the CentralBank of the UAE (CBUAE) after successfully meeting all regulatory conditions and requirements through a rigorous approval process.

America Biometric Payments 2 Global, especially mobile-first markets Cash Payments 5 Emerging Markets, some developed regions CentralBank Digital Currencies (CBDCs) 1 Asia, Caribbean Credit Cards Overview : Credit cards allow consumers to make purchases on credit, paying later and often with interest.

Customers in this age of instant gratification always expect a smooth and seamless online payments experience. As a business owner, you must have a clear understanding of how online payments processing works to be able to create a hassle-free checkout process that will keep buyers coming back to your eCommerce store.

In Vietnam, bank-owned apps are rapidly gaining popularity across all generations, outpacing independent fintech platforms like MoMo and ZaloPay, which are seeing a decline in usage and preference, according to a new report by Decision Lab, a Vietnamese market research firm. million monthly active users, giving it a massive scale and reach.

Just before the COVID-19 pandemic, one of the leading private banks in Latin America made a strategic move: it began replacing its legacy card issuing system in a bold shift toward digital-first issuing. With 24/7 online processing and event-driven decisioning, issuers deliver personalisation at scale—right when it matters.

Centralbank digital currencies (CBDCs) have rapidly evolved from theoretical concepts into live pilots and national deployments. From Asia to the Caribbean and Europe, centralbanks are grappling with how to digitise public money while preserving trust, utility, and sovereignty.

Mastercard, in collaboration with the CentralBank of Egypt (CBE) and Egyptian Banks Company (EBC), brings Apple Pay to users in Egypt, providing a safer, more secure and private way to pay in-store, in-app and online. Apple pay empowers consumers with a safer, more convenient way to pay, whether in-store or online.

How fintechs are challenging traditional banks in the merchant services space, posing a threat to banks’ core business and revenue streams. The shift driven by fintechs could erode banks’ dominance, forcing them to modernise or risk losing a significant share of the market. Why is it important? What’s next?

per cent CentralBank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. Through its regulatory sandbox, the CentralBank of Armenia (CBA) has attracted $90million in investments, propelling the country to 34th place in the Global Fintech Index 2023.

The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services. Looking to 2025, mobile payments and digital commerce are projected to exceed 10 trillion, with open banking and real-time payments leading growth. trillion.

The horse in front Just like the vast natural grassland of the Kazakh Steppe, which lies in contrast to the modern cities of Astana and Almaty, so is the traditional banking landscape (dominated by three large banking groups) contrasted by a fast-moving digital leader – Kaspi.kz (Kaspi). However, this was not the case for Kaspi.

Indigenous Banking (Shroffs and Mahajans): Long before modern banks, India had a thriving indigenous banking system. These banks introduced formal ledger-based accounting and cheque payments. This laid the foundation for a centralized monetary authority and future oversight of payment systems.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

For online shopping, Visa passkeys replace passwords or one-time codes. Click to Pay – Enables consumers to complete online transactions within a few clicks, powering a more seamless and secure checkout experience at scale. to broaden its merchant coverage network across Japan.

Egyptian fintech PayMint has received final approval from the CentralBank of Egypt to launch its first ‘Meeza’ prepaid cards in partnership with Abu Dhabi Islamic Bank (ADIB). PayMint plans for the new Meeza prepaid cards to enable its customers to carry out purchases, cash withdrawals, and online shopping in Egypt.

Ralf Germer, CEO and co-founder, PagBrasil Pix has been a giant windfall for Brazil and is now responsible for 90 per cent of bank transactions in Brazil. Through this collaboration, Bancard will offer this service to banks in Paraguay, enhancing convenience and financial accessibility for Paraguayan travellers.

Moreover, as super apps and embedded ecosystems gain traction in emerging markets, tokenisation offers a scalable security model that can flex with the complexity of multi-role, multi-wallet environments, notes Venkat Srinivasan, sales & go-to-market, banking and payments products, at Thales.

Mobile phone usage in Senegal has surpassed 60 per cent this year. Mobile money, in particular, has had a significant impact, with over 70 per cent of adults in Senegal reporting its use within the last 30 days. Despite this digital advancement, only seven per cent of the population utilises traditional financial services.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. They let buyers initiate payments by placing their mobile phone near a compatible payment terminal.

For businesses, enza will facilitate the acceptance of Mastercard payments across in-store, online, and in-app channels. billion mobile wallets globally. Fintechs will be able to configure pre-paid or post-paid accounts, as well as issue physical or virtual Mastercard cards.

The pressure to solve real challenges — such as low banking penetration, financial exclusion, limited access to credit cards, lack of interoperability, and acceptance barriers for traditional (and international) payment methods — planted the seeds for fintech and digital banks. And thats exactly what we did.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. And thats a really positive development.

Furthermore, Tap allows entrepreneurs to unify their online and in-person sales channels. Also, the Mollie platform facilitates a range of other financial services, including online payments, digital invoices, payment links, and business financing. The Tap terminal is available from EUR 45.

For example, contactless acceptance and PIN Online have been supported in nexo protocols since the beginning, whereas some countries took over 10 years to roll them out. nexo protocols have since been adopted by major players across Europe and beyond — not only for card payments but also supporting mobile and QR Code -based payments.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

Home News Security Bank of England accused of 'blundering' to security disaster as hundreds of laptops go missing Editorial This content has been selected, created and edited by the Finextra editorial team based upon its relevance and interest to our community. Meanwhile, 109 mobile phones went missing worth an estimated £1737.

Hyperdesk – San Francisco, California and Mexico City, Mexico Founded in 2025, Hyperdesk provides an AI-powered search engine that helps credit unions and community banks grow their loans and deposits by better engaging with local businesses. Karen Elliott is CEO. Eric Yez is Founder and CEO. Polish fintech BidFinance raised 1.6

He brings over 30 years experience in financial services with senior roles across global banking, private equity and accounting. He also joins the board of Quantum as director of fintech and banking, helping with its plan to list on the London Stock Exchange in 2026. Radford previously held the CEO role at Revolut UK from 2020 to 2023.

million, and, more importantly, its banking license. The deal still requires sign off from Argentina centralbank, says Bloomberg, citing sources. Revolut will secure Cetelems assets, which are worth just $6.4 We use cookies to help us to deliver our services.

Brazil’s CentralBank has suspended WhatsApp’s payment feature in the country, citing antitrust concerns, according to Bloomberg on Tuesday (June 23). Mastercard and Visa have been requested to stop payments and money transfer services through the app in Brazil as well, the bank said.

Sweden’s Riksbank is assessing e-krona, a new form of digital currency that hopes to take the country a step closer to the creation of the world’s first centralbank digital currency (CBDC), according to reports on Thursday (Feb. CBDCs are a digital form of traditional money issued and governed by a country’s centralbank.

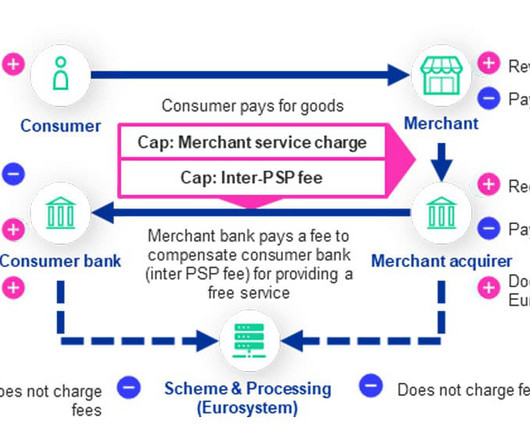

TRANSACTION FEE: A step-by-step overview of the digital euro compensation model Payment service providers will be able to charge merchants a fee for enabling them to accept digital euro transactions, the European CentralBank (ECB) has revealed, but a cap will be placed on the amount that it will be possible for them to charge.

The recently released report by the Bank for International Settlements ( BIS ) offers a general framework for digital currencies. The BIS noted of centralbank digital currency ( CBDC ) that “a CBDC could provide a complementary centralbank money to the public, supporting a more resilient and diverse domestic payment system.

The centralbank of Kenya is putting forward new legislation to govern interest rates charged for digital lenders’ loans. Online lenders will need the green light from the centralbank to roll out new offerings or hike lending rates if the legislation is put into law, Quartz Africa reported.

A group of big European banks is planning to challenge Visa ’s and Mastercard ’s positions as the world’s two largest payment processing networks, Electronic Payments International reported. . The launch, first reported by Les Échos, is expected to be revealed by the 24 banks as early as Thursday (July 2). .

To remedy the problem, the Reserve Bank of India supports an option for offline payments through cards, wallets and mobile devices. The country’s centralbank has proposed a pilot program for such a platform with built-in safety and liability protections for users. It’s going to be a long-drawn process,” he said.

The new license from the country's centralbank will let MercadoLibre have autonomy in creating and directly operating financial services in Brazil, along with accessing new types of financing. MercadoLibre's credit arm MercadoCredito was formed in 2017 in Brazil, and has been tied to mobile wallet service MercadoPago.

In Asia-Pacific (APAC), fraud is becoming an increasingly serious challenge for financial institutions, an issue that has been exacerbated by the rapid adoption of digital transactions and onlinebanking. A year later, Kathmandu-based NIC Asia Bank suffered a major heist, with hackers managing to make about US$4.4

Open banking is appealing to financial institutions (FIs) and regulators in many markets, even as the pandemic sweeps across the world. Regulators in other regions, including Latin America, are also shaping and announcing plans to enable open banking and better support digital financial systems. Around The Data Protection World.

The CentralBank of Ghana (BoG) has announced it granted Vodafone Cash and CalBank customers the opportunity to test its online version of its digital currency (CBDC), the eCedi.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

The People’s Bank of China (PBoC) has ordered all online payment companies to channel mobile payments through a new clearing house by next June, which could have an impact on the dominance of Ant Financial and Tencent. China is the world leader in mobile payments, with transaction volumes rising last year to Rmb59tn ($8.8tn).

According to Visa, tokenized transactions accounted for 85% of all mobile debit transactions in North America in 2023. World Bank data indicates that global remittances reached $794 billion in 2023. World Bank data indicates that global remittances reached $794 billion in 2023.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content