This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These banks introduced formal ledger-based accounting and cheque payments. Cheque System: The cheque emerged as a formal payment instrument, requiring physical movement and manual clearing processes. This was a significant step towards non-cash payments but was slow and prone to errors.

Helena Mao , vice president of global product strategy for payments at Blackhawk , spoke to PYMNTS, explaining why many consumers were slower to adopt the rollout of mobile wallets and payment methods in places like the United States — and why those feelings may be shifting. By contrast, U.S. is suddenly popping up everywhere. “QR

Music aficionados who swear that digital distorts the sound of music. solution in a world of digitalpayments that continues to stick around. Checks have a long and frequently complained about history of being both slow and costly — a friction-filled paper-based payments method. And there’s the paper check — a 1.0

Wells Fargo announced Tuesday (April 2) the launch of contactless consumer credit and debit cards. In a press release , Wells Fargo said the new cards will enable customers to complete transactions quickly and with a single tap at millions of merchants and transit systems that accept contactless payments.

As payments become more intricate, Mastercard today announced the latest enhancement to its new Mastercard Payment Passkey Service which enables secure, on-device biometric authentication through facial scans or fingerprints, the same way consumers unlock their phones every day.

Today we hear insights from payments experts, including the adoption of tap-to-pay technology, the role of blockchain and AI in payments, flexible payment terms, security in authentication methods, PSD3 implementation, vertical-specific solutions, and the rise of digital wallets.

Visa announced that it will bring the power and ubiquity of installment lending to digital and physical points of sale (POS) through application program interfaces (APIs) that support the development of customized installment plan options for Visa cardholders. trillion market in 2017 growing at twice the rate of credit cards.

In the absence of corporate travel and entertainment, as the road warriors stay (and work) at home, it may make sense that commercial card use would see a pause in the B2B space. But we’ve focused on finding new areas of spend for buyers to utilize their cards,” Leavitt noted. “But But in an interview with Karen Webster, Dean M.

Can pushpayments make the push into full acceptance by consumers and corporates? In envisioning just what the concept of “push” payments means, Edwards said one need only think about how pull payments work. They trust the payments ecosystem to manage and complete the actual transaction behind the scenes.

For example, Bank of America (US) announced its clients reached 26 billion digital interactions in 2024 (a 12% year-over-year increase), including 676 million interactions with its AI virtual assistant “Erica.” Another survey of AI-savvy firms found that industries that underwent early digital disruption (e.g. At the same time, a J.D.

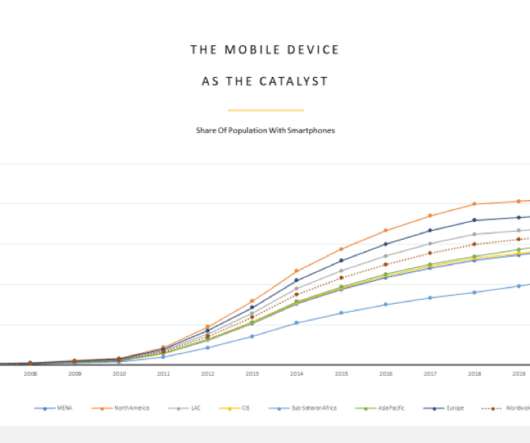

Driven by faster phones, ingenious apps and sheer market force, the move to instant is pushing the boundaries of what’s possible with payments, opening up new worlds of risk and reward. Inspecting the “up-and-to-the-right” growth curve of instant payments , it’s no shock how many players want in. Making Money Fast.

Apple and Goldman Sachs Group are in the midst of bringing a joint Apple Pay-designated credit card to market. Could that warm feeling could come courtesy of the new plastic card? Plastic cards are ubiquitous and the default payment method at checkout. percent at launch, to 2.6 percent in March 2015, to 3.0

I couldn’t think of a more relevant metaphor for the tectonic shifts that have influenced the direction of the payments, commerce and retail ecosystems over the last several years. That change came courtesy of a shift in the Earth’s tectonic plates — a shift centuries in the making and unbeknownst to anyone — until it was much too late.

In turn, restaurants are fast embracing mobile payments as they look to deliver on the speed and convenience their customers have come to expect. As restaurants and QSR chains upgrade their payment systems to accept mobile and other forms of digitalpayments, they are also adopting instant payments for wages and tips paid to their workers.

The QR Code has been enjoying some love and attention over the past few weeks, though the prospects for the digitalpayment tool remain relatively limited outside of Asia, at least according to one report. The idea is to “promote global interoperability across EMV QR Code payments,” the standards group said in a statement.

Contactless payments market has been growing quickly. As digital infrastructure continues to advance, the ease and speed of contactless transactions are becoming increasingly attractive to consumers and businesses. What are Contactless Payments? Here’s a breakdown of each type and its growing significance: 1.

Here, Ray Merceron , general manager of sales, LAC region at i2c , the global payment processor, breaks down how Latin America’s payment market is evolving, its challenges, as well as i2c’s plans in the region. Latin America’s payment technology landscape is evolving rapidly.

For starters, five billion digital identities. In an interview with Karen Webster, Trulioo CEO Stephen Ufford said the roadblocks on the path to real financial inclusion and a network that truly spans the globe can be boiled down to one key challenge: crossing the Rubicon from analog to digital.

Take faster payments. The company that commercialized the idea and consolidated the market to establish the first global faster payments network was Western Union in 1851. Innovative ideas are inspired by smart people who see problems and have the conviction, capital and courage to come up with new ways to solve for them.

McCarthy told Karen Webster for the latest edition of The Week In Payments, merchants are experiencing sales and cash flow challenges as reticent consumers proceed with caution – and the added capacity constraints are heightening their concerns. Finding the Opportunity In Fixing Net Terms Payments. Most every state in the U.S.

The word is out about instant payments — a fact made largely indisputable by the numbers. When we asked in 2017 how many consumers have received an instant payment, the answer was a mere 11 percent. The numbers go beyond awareness. Instant disbursements are also picking up steam where it really counts — usage. How do they do that?

It’s the impact of the digital-first consumer on nearly every one of the 10 pillars that define our connected economy — and the efforts of companies large and small to capture their attention and their business. Source: PYMNTS.com longitudinal study of over 40,000 consumers (data from the most recent panel on Nov. consumers — 47.2

The two most powerful forces shaping the future of retail payments have nothing to do with payments at all. It’s why we’re witness to unprecedented waves of consolidation in the merchant acquiring and payments processing space – and why there will be even more to come in the short and longer term. At least at first glance.

I couldn’t think of a more relevant metaphor for the tectonic shifts that have influenced the direction of the payments, commerce and retail ecosystems over the last several years. That change came courtesy of a shift in the Earth’s tectonic plates — a shift centuries in the making and unbeknownst to anyone — until it was much too late.

These are merchants, too, he noted, who probably already had one foot in the omnichannel world; “growing up on digital channels,” as many may have first started selling on social channels as a complement to a physical stand in a farmer’s market, kiosk or pop-up shop. For merchants in the developed world – like the U.S.

But on the consumer level, between millennials and baby boomers, there’s the question of who is pushing more to get society to go cashless. As for baby boomers getting on the cashless society bandwagon, Catania said that boomers aren’t using cards for purchases under $10.

That is how the world first met the iPhone a little over ten years ago in January 2007, when Steve Jobs took to the stage to announce Apple’s latest and greatest innovation. The world stopped what it was doing to take a look. And then there was the Super Bowl. Americans may not at that point fully have known why, but they knew that they wanted it.

The year may be winding toward a close and slowing down, but this week the world of payments showed signs of neither as big players seemed to be racing down to the wire to get their big news out before the clock strikes 12 on the 31st and the calendar resets to 2020. for each share. The Consideration represents a 47.5

From investing to storing funds to making payments, the bank offered the total financial services bundle. And we came along with ubiquitous mobile remote deposit capture, so now consumers can put their checks into any account they want from a single app in minutes.”. The customer is approved and voila!

The path to faster payments in the U.S. Instead, we could do something right away — or almost right away — that would make payments between consumers and businesses faster. And a complicating factor for how to monetize “faster payments” in the U.S. We could kill the check – and the checks rails that exist to support them.

It’s why we have a Monday Conversation every week – a conversation intended to get another human being on the other end of the phone for their input into what the moving and shaking in the world of payments and commerce means to those who are at its helm. Americans stopped talking to each other. So what did we learn this year?

The last 10 years in payments and commerce have given us millions of dots to connect. Payments will power that shift. Payments will power that shift. 2020 Trendline One: Rapid Acceleration Of Cash To DigitalPayments. Ironically, cash-in and cash-out networks will play a critical role in enabling that shift.

The last 10 years in payments and commerce have given us millions of dots to connect. Payments will power that shift. Payments will power that shift. 2020 Trendline One: Rapid Acceleration Of Cash To DigitalPayments. Ironically, cash-in and cash-out networks will play a critical role in enabling that shift.

Animal metaphors aside, 2019 is a year that should inspire excitement, along with great anticipation, across the expansive payments and commerce ecosystem: It’s the bridge year between the decades of the ‘10s and the ‘20s. Welcome to the first Monday of 2019. That makes it the most important year of the last decade. Consider this.

In what has been — historically speaking — the blink of an eye, mobile phones have gone from zero to nearly ubiquitous in a remarkably short time. There are billions of devices always on the internet, creating massive clouds of data exhaust whenever they are used to … enable commerce or make a payment,” Sondhi said.

tied as they are to paper-based payments. In the latest of a continuing series on B2B payments, Melio CEO Matan Bar told Karen Webster that payments flexibility is key in helping small and medium-sized businesses (SMBs) navigate the pandemic — and flexibility leads to better cash flow, the lifeblood of companies (no matter their size).

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content