This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is embeddedfinance at work, and it’s quietly transforming the way we interact with money – without most of us even realising it. Wait, What’s EmbeddedFinance? If you’ve never heard of embeddedfinance , don’t worry. Why Is EmbeddedFinance Such A Big Deal?

Embeddedfinance is rapidly changing the way consumers and businesses alike interact with financial services. As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms.

Emerging trends such as cross-border payment systems and open banking initiatives are breaking down traditional barriers, fostering greater connectivity and efficiency in Asias financial landscape. EmbeddedFinance Hailed as the Future of Fintech The embedded payments market is expected to reach a global transaction value of US$2.5

What are some embeddedfinance trends were seeing in Brazil, and how do they differ from Mexico and Guatemala? Embeddedfinance is rapidly expanding in Brazil. Mexico and Guatemala are also embracing this global trend of integrating financial services into non-financial platforms.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

Embeddedfinance is transforming industries by incorporating financial services directly into non-financial platforms. This integration allows businesses to offer banking-like services, enhancing customer experience and simplifying transactions. This shift is redefining traditional banking structures.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

Amid the ongoing digital revolution and shifting customer preferences, embeddedfinance is reshaping the financial industry. Banking has transcended its traditional confines, forging innovative partnerships that prioritise convenience and accessibility. Customer loyalty is the bedrock of any business.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

FIS unveiled its embeddedfinance platform, Atelio by FIS, this week. Atelio by FIS , launched this week , is one of the first banking-as-a-service offerings from a major core provider. FIS’ latest offering comes at a time when growth in embeddedfinance is expected to soar.

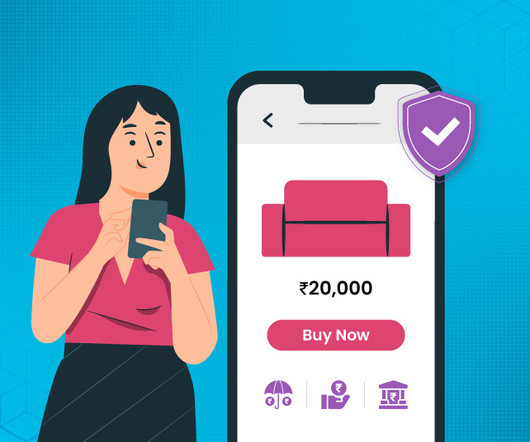

The traditional banking setup has seen a complete overhaul with increasing technological advancements. All this has been made possible by embeddedfinance, which allows the integration of financial services into non-financial services. It may seem like a new world, from loans in 59 minutes to digital wallets.

In this Marqeta review , we explore how the company operates, the problems it solves, its role in embeddedfinance , and the challenges ahead. This mission continues to expand, as embeddedfinance reshapes expectations around how companies integrate financial services into daily operations.

These trends include ecosystem banking, generative artificial intelligence (GenAI), and embeddedfinance, a new report by PwC India and ASSOCHAM says. Generative AI driving banking and fintech trends in India Generative is one of India’s biggest fintech trends highlighted in the report.

Canopy Servicing , the leading commercial loan servicing platform, and Moov Financial , a leading provider of modern payment processing infrastructure, have joined forces to launch Canopy Repay, an integrated solution streamlining loan repayment operations for banks, non-bank lenders, and credit unions.

Modern finance teams rely heavily on embeddedfinance, SaaS fintech software, finance APIs, and cloud-based platforms to run everything from payments to compliance to cash management. Banking-as-a-Service & EmbeddedBanking APIs Let’s start the top 100 fintech tools and platforms with embeddedfinance.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

In simple terms, embeddedfinance is financial/banking services by a non-financial/banking services provider. For many banks, the rise of these offerings represents a threat and perhaps brings an urge to re-evaluate their products, modernize their services, and invest more in customer loyalty.

In simple terms, embeddedfinance is financial/banking services by a non-financial/banking services provider. For many banks, the rise of these offerings represents a threat and perhaps brings an urge to re-evaluate their products, modernize their services, and invest more in customer loyalty.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

Through Lili Connect, corporate formation services partners can now offer their customers streamlined banking, accounting, and tax preparation solutions. small businesses founded by non-residents contribute significantly to the national economy, supporting over five million jobs and more than $1 trillion in output. Non-resident U.S.

UK consumers are leading the charge on digital financial services adoption amid rising demand for more innovation and convenience in payments and banking, according to a study from Marqeta (NASDAQ: MQ), the global modern card issuing platform powering some of today’s most innovative embeddedfinance solutions.

Embedded insurance in Australia is poised for strong growth, driven by various factors related to customer preferences, technological advancements, and industry collaborations. Embedded insurance refers to the integration of insurance products into non-insurance platforms or experiences, such as e-commerce, travel or healthcare.

Flix Flix enables financial platforms to offer seamless cross-border payments via WhatsApp, combining embeddedfinance with a fast, familiar, and conversational user experience. Banks, credit unions, community banks, wallets, and digital banks. Banks, credit unions, community banks, wallets, and digital banks.

Embeddedfinance is rapidly changing the way consumers and businesses alike interact with financial services. As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms.

Marqeta (NASDAQ: MQ), the global modern card issuing platform that enables embeddedfinance solutions for the world’s innovators, today announced it has signed a five-year deal with Varo Bank , N.A., Varo is the first bank to receive a de novo national bank charter as a consumer techbank in the U.S.

Embeddedfinance has been a game-changer for SMEs who previously struggled to obtain funding from traditional banks. However, fintech companies with embeddedfinance solutions have a responsibility to become regulation savvy even if they aren’t regulated. One area to consider carefully is data privacy.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

In a recent study conducted by Forrester on behalf of Fabrick titled, “Embrace EmbeddedFinance for Seamless Payment Success: A Spotlight on Europe,” valuable insights were obtained regarding the state of EmbeddedFinance across Europe.

In 2021, e-money accounts surpassed bank accounts as the most commonly held financial accounts in the country. By contrast, the growth of traditional bank accounts was more modest, rising from 12% to 23% during the same period. Convenience (56%) and speed (46%) are the main drivers of interest.

” Here is how the AI responded: Predicting the exact trends for 2024 is speculative, but here are potential emerging trends in fintech: EmbeddedFinance : Further integration of financial services into non-financial platforms like e-commerce, SaaS, and marketplaces. Embeddedfinance ChatGPT was spot on.

Clip Money , a Canada-based company operating a multi-bank, self-service deposit network for North American businesses, is expanding its over-the-counter deposit service for businesses in partnership with fintech platform and bank holding company Green Dot.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

Post-COVID-19, webinars continue to thrive, owing to their versatility, accessibility, affordability and effectiveness in engaging and educating audiences in an increasingly digital world. The session will be moderated by Urs Bolt, a Fintech and Banking Expert. Similarly, research by GoodFirms found a notable uptick, with 46.5%

From breakthroughs in digital banking to advancements in blockchain technology, we explore the cutting-edge developments that are not only revolutionising the way financial services are delivered in Singapore but also setting benchmarks for the global fintech landscape. billion in 2024 to US$63.18

Appointments Sibstar, the UK debit card and app for people living with dementia, has appointed GoHenry co-founder and CEO, Louise Hill, as a non-executive director. Ortec Finance has expanded its board with the appointment of two new members. Ortec Finance is a provider of technology and solutions for risk and return management.

OKX, a cryptocurrency exchange and global onchain technology company, has teamed up with Standard Chartered, appointing the international cross-border bank as its third-party crypto custodian for its global institutional business. ZA Bank, a digital bank in Hong Kong, has commenced the sandbox trial of its virtual asset trading service.

In an era dominated by digital innovation, the banking sector is evolving rapidly to meet the modern consumer’s demands for seamless and integrated financial services. As banks strive to align with the digital-first preferences of today’s consumers, the modernisation of core banking systems becomes a strategic necessity.

Paymentology , the global issuer-processor, has joined forces with Diamond Trust Bank , a tier-one East African commercial bank, in a move hoping to help drive financial inclusion in Kenya through the embedding of financial services, and deployment of Cards-as-a-Service (CaaS).

The Rise of EmbeddedFinanceEmbeddedfinance is revolutionising the way businesses interact with financial services. By integrating payment solutions directly into non-financial platforms, companies can offer seamless user experiences. In payments, open banking facilitates account-to-account (A2A) transfers.

Marqeta (NASDAQ: MQ), the global modern card issuing platform that enables embeddedfinance solutions for the world’s innovators, today announced a new customer, Swiss4 , providing real-time and personalised digital payment services for their customers.

This April, The Fintech Times is focusing on all things embeddedfinance, the integration of financial services into non-financial products and services. As the space rapidly develops, we look to highlight the latest developments, initiatives and challenges embeddedfinance has to offer and overcome across the globe.

The year 2023 marked a pivotal moment for the fintech industry, with the prevailing global funding trends encapsulating a period of introspection and recalibration amidst a backdrop of economic fluctuations, including notable bank failures and precipitous cryptocurrency downturns. appeared first on Fintech Singapore.

An industry survey conducted for the report found that 67% of fintech founders in India prefer VD, neck-and-neck with bank loans, with 80% stating that VD constitutes more than 11% of their raised debt capital. Essentially, the fintech startup places a deposit with the bank, which acts as a safety net to absorb initial borrower defaults.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content