This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The dual impact of generative AI on payment security, highlighting its potential to enhance fraud detection while posing significant data privacy risks. It underscores the need for payment firms to balance AI innovation with robust privacy and regulatory compliance to protect sensitive consumer data. Why is it important?

Overview of International Payment Processing At its core, international payment processing involves handling transactions across borders , where factors like currency conversion, payment method preferences, and local regulations come into play. As global online shopping grows rapidly, consumers expect seamless payment experiences.

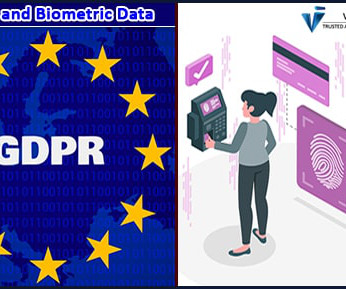

The rise of data privacy concerns has led to a surge in global regulations, such as the EU General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), which are drafted to protect peoples individual data protection rights. Africa and Asia show different levels of adoption with resp.

As technology advances and the use of biometric data becomes more prevalent, it is crucial to address the privacy concerns and regulatory compliance associated with this sensitive data. By addressing these issues, organizations can strike a balance between reaping the benefits of biometric technology and protecting individuals’ privacy.

As fraudsters are continuously finding new ways to strike, we’re continuously finding new ways to prevent them with controls such as encryption, multi-factor authentication, fraud detection software, etc. The TPM can securely store and generate cryptographic keys, passwords, certificates, and encryption keys. However, manufacturers DO.

The further we’ve delved into the world of regulation and compliance, the clearer it has become that there are a whole host of challenges for financial institutions to contend with. When it comes to cybersecurity, the topic of data protection and privacy is arguably one of the most important.

Regulatory challenges Regulators are in a race against time. The rapid adoption of digital wallets has introduced a complex web of regulatory considerations, ranging from data privacy and cybersecurity to anti-money laundering (AML) compliance and cross-border transaction governance.

Companies that excel in data protection comply with stringent regulations and gain a competitive edge by building solid relationships with their customers. Always provide clear, easily understandable privacy policies, and obtain explicit consent before collecting personal information.

In the financial sector, it includes fraud detection, threat intelligence, data encryption, biometric verification, and risk monitoring. Regulation and Compliance Cybertech is not only about protecting infrastructure, it is also about meeting legal and regulatory expectations. Emerging Trends in Cybertech Cybertech is evolving quickly.

As fraudsters are continuously finding new ways to strike, we’re continuously finding new ways to prevent them with controls such as encryption, multi-factor authentication, fraud detection software, etc. The TPM can securely store and generate cryptographic keys, passwords, certificates, and encryption keys. However, manufacturers DO.

To rethink the assumptions behind CBDC proposals and push for more privacy-oriented innovative solutions Many central banks and financial authorities worldwide are experimenting with central bank digital currency (CBDC), including the European Central Bank, the US Federal Reserve, and the Bank of England, among others. What’s next?

” The central bank says all laptops, tablets and mobile phones are encrypted and that any lost or stolen devices are also be blocked from further communication with the bank. Please read our Privacy Policy. Sponsored [New Impact Study] Reimagining Customer Journeys: How can Banks Upscale Experience and Boost Retention?

Encrypting messages and choosing secure ways to talk online are keys to keeping secrets safe in any language. Use encryption and strong passwords to protect messages. Think about the various regulations around the world. The EU has GDPR , while the US sticks to HIPAA for health data and CCPA in California for consumer privacy.

Merchants in high-risk categories, such as online gaming, travel, and adult services, benefit from BIN data as it helps processors manage risk levels and ensure compliance with industry regulations. Payment processors must meet both local regulations and the specific compliance requirements of each card network and their sponsoring bank.

Businesses deploy proxy servers to monitor and regulate their employees’ internet usage, ensuring data security and blocking access to harmful sites. Moreover, proxies can encrypt your data, adding an extra layer of security that shields sensitive information from hackers and eavesdroppers.

Data Privacy and Security Concerns As fintechs handle sensitive financial data, data privacy and security are critical. Fintech companies must prioritise data protection through encryption, authentication, and compliance with local regulations to build trust with SME users.

With WollettePay, each transaction is protected by biometric verification, tokenisation, and advanced encryption, providing merchants and consumers with complete confidence in a seamless, secure experience. Please read our Privacy Policy. No cards Merchants avoid card fees and reduce fraud. Omnichannel Works online and in-person.

Privacy-Friendly Cryptographic Security in Compliance with the Law Resistance to traditional ID-based age verification is growing. While user ID-based methods remain effective and compliant, they are often seen as invasive and raise privacy concerns. These solutions aim to balance security, user-friendliness, and privacy protection.

Facebook said it is going to enhance encryption capabilities on its Messenger communication platform, despite requests from lawmakers and regulators not to do so because of the potential result that pedophiles and criminals will be harder to track.

It highlights the urgent need for payments firms to address AI-driven fraud to protect financial security, maintain customer trust, and comply with regulations. The growing threat of AI-related fraud puts financial institutions at risk of significant financial losses and jeopardises consumer trust and compliance with regulations.

The issuance of the proposed regulations follows a series of industry surveys and discussions with its regulated entities over the course of several years that provided insights on their cybersecurity programs, related costs and future plans. Data encryption.

Age verification systems are essential tools for ensuring compliance with regulations designed to prevent minors from accessing inappropriate content or services. Age verification tools are developed to follow minimum age regulations to ensure that minors do not gain access to age-restricted content, services, or products.

10) over the companies’ decision to use encryption technology, according to a report by Reuters. The lawmakers warned that both companies should allow for “backdoor” access to law enforcement or they would be forced to regulate the technology. senators went head to head with executives of Apple and Facebook on Tuesday (Dec.

Why Traditional Defences Fall Short Historically, businesses have relied on layered security controls like encryption, firewalls, and access policies to protect payment information. Businesses that wait for regulation, a major breach, or a mandate from a banking partner are already on the back foot. Please read our Privacy Policy.

10) over the companies’ decision to use encryption technology, according to a report by Reuters. The lawmakers warned that both companies should allow for “backdoor” access to law enforcement or they would be forced to regulate the technology. senators went head to head with executives of Apple and Facebook on Tuesday (Dec.

The Federal Trade Commission (FTC) has requested comment on the proposed amendments of two rules that protect the privacy and security of customer data held by financial institutions (FIs). The proposed changes are related to the Safeguards Rule and the Privacy Rule under the Gramm-Leach-Bliley Act.

Security and technology consulting company Accutive is rolling out a new solution designed to give enterprises an alternative to data encryption to protect sensitive information. Data Masking, meanwhile, lets businesses “mask” sensitive data as an alternative to encryption. In a press release on Wednesday (Feb.

Atlanta payments encryption firm Bluefin is partnering with New York mobile payments processor PAAY to advance eCommerce security. PAAY provides strong authentication at the front door and Bluefin encrypts and tokenizes the data at the point of interaction on the web. Each $1 of fraud costs retailers $3.13. .

If your business engages with these customers, it is subject to the EU’s General Data Protection Regulation (GDPR). This extensive data privacyregulation has an impact on many U.S. The GDPR has a considerable influence on data privacy globally, but what does it mean for the US? entities due to its extraterritorial reach.

It’s been a whirlwind few weeks — OK, make that months — for big tech firms as regulators look ever more closely at business tactics. Privacy and Competition. Now they should be leveraging that momentum and taking things to the next level to understand the controls — firewalls, encryption, policies, etc.

Whether we are setting up a new bank account, making a purchase online, or accessing government services, confirming who we are in the virtual space is crucial to ensuring our security, the protection of our privacy, and the improvement of our user experience. Digital identity verification helps businesses comply with these regulations.

This methodology aligns with the latest global regulations, including the EU AI Act and onshoring requirements in countries like Singapore and Australia. In 2022, the company received a patent for another piece of AI, their Secure Lockbox , which features pioneering homomorphic data encryption.

The Wall Street Journal is reporting that there are emails sent by Facebook CEO Mark Zuckerberg that possibly link him to troublesome privacy issues at the company. Facebook has been functioning under a consent decree it agreed to with the FCC in 2012, after a scandal with Cambridge Analytica regarding data privacy.

Apple has reportedly hired Sandy Parakilas, an ex-Facebook employee who became a prominent critic of the company, as part of its privacy team. According to Financial Times , Parakilas monitored privacy and policy compliance of software developers for Facebook for 18 months before he left in October of 2012.

DIMOCO, an Austrian-licensed payments firm and carrier billing company, has become the first authorised provider of carrier billing for Germany’s regulated igaming sector. The approval from national regulator GGL allows licensed operators to offer mobile payments within set player limits.

Its role is to encrypt and securely transfer your customers payment data to your payment processor. All the data transfer between the digital wallet and your payment terminal are encrypted and the system also uses tokenization to ensure iron-clad data security. However, cryptocurrencies arent without their drawbacks.

Two-factor authentication, encryption and fraud detection are minimum requirements. Security: These payment solutions come with strong security features like advanced encryption and authentication. This reduces fraud risk and addresses data privacy concerns, which, again, helps to build trust between merchants and consumers.

“From a practical perspective, it’s right that at the moment retailers and distributors seem to be unprepared for the regulations and for the need to ensure that there are Certificates of Compliance when they sell connected products, but that will hopefully improve over time. ” Where do APIs come into this?

Tokenization & Biometrics: One-time-use tokens, facial recognition, and hardware-level encryption now set the standard. Data Governance: As wallets become data-rich ecosystems, compliance with GDPR, PSD3, and future AI regulations will be mission-critical. Please read our Privacy Policy.

Some best practices to ensure robust cybersecurity include: Data Encryption: All sensitive data should be encrypted both in transit and at rest to prevent unauthorized access and ensure efficient data security measures. Authentication: Implement multi-factor authentication (MFA) to add an extra layer of security to your system.

Some best practices to ensure robust cybersecurity include: Data Encryption: All sensitive data should be encrypted both in transit and at rest to prevent unauthorized access and ensure efficient data security measures. Authentication: Implement multi-factor authentication (MFA) to add an extra layer of security to your system.

Encrypting messages and choosing secure ways to talk online are keys to keeping secrets safe in any language. Use encryption and strong passwords to protect messages. Think about the various regulations around the world. The EU has GDPR , while the US sticks to HIPAA for health data and CCPA in California for consumer privacy.

The Proposal also excludes certain types of transactions, including the following: International payments or money transfers (e.g., Under the Dodd-Frank Act, large non-bank digital consumer payment companies are subject to CFPB enforcement authority.

Secure payment systems comply with strict security standards and regulations set forth by governing bodies and industry organizations. Regulatory Compliance: Payment systems may also need to comply with specific regulations and laws related to financial transactions and data protection, depending on the region and industry.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content