This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Central bank digital currencies (CBDCs) have rapidly evolved from theoretical concepts into live pilots and national deployments. From Asia to the Caribbean and Europe, central banks are grappling with how to digitise public money while preserving trust, utility, and sovereignty.

From digital payments to decentralised finance (DeFi), these companies are solving real-world challenges like financialinclusion and cross-border transactions, while setting new global standards for innovation. Coda aims to make digital transactions simple, inclusive, and accessible to everyone. Coda Valuation: $2.5

Tokenisation is now a core enabler of secure, interoperable digital paymentspowering embedded finance, asset tokenisation, and evolving identity flows. Once a system for masking sensitive data, tokenisation has evolved into a foundational technology for enabling secure, interoperable, and scalable digital payments.

These companies span every segment of the market, from long-established remittances players and banks to neobanks, business-to-business (B2B) platforms, stablecoin providers and regional specialists, and are powering global trade. It is one of the Big Three local banks in Singapore, and among the largest banks in Southeast Asia.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? CEO Linda Yaccarino framed the move as a leap forward, but the real story is bigger: tech giants are no longer just facilitating payments, theyre actively reshaping the financial industry.

Payments providers will need to prioritise interoperability and compliance to unlock growth while addressing security and volatility concerns. Decentralisation, through DeFi and CBDCs, is driving financial innovation, addressing challenges like financial crime and cybersecurity, and meeting growing demand for secure, efficient solutions.

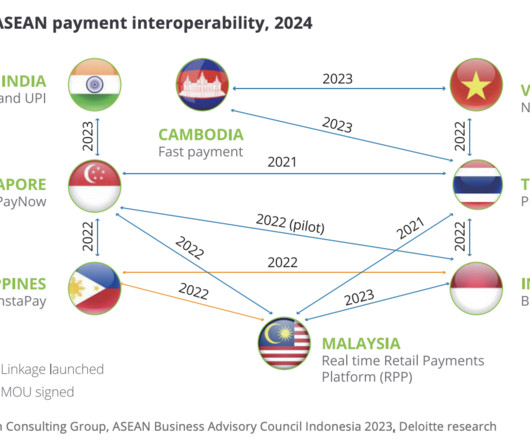

Asia Pacific point-of-sale payment methods – Select markets, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Payment interoperability The growth of digital payment innovations in APAC has emphasized the need for connectivity and interoperability in both online and offline transactions.

PYMNTS’ November 2020 Disbursements Tracker® , done in collaboration with Ingo Money , states that “FIs that support digital and mobile payment tools could help these consumers access financial solutions without using traditional accounts, but many FIs must address age-old challenges before they can roll out such tools.”

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financialinclusion and helping people develop healthy financial habits.

Women, refugees, the poor and the young had historically had low inclusion in Jordan’s banking system because there’s no good onboarding process for them – but mobile-phone penetration runs deep across Jordanian society, even among critically underbanked segments. Building Better Payments And Banking Services .

The customer-merchant Payment Service Provider (PSP) takes charge of the approval process through National Payments Corporation of India (NPCI), swiftly debiting the money from the issuer bank and crediting it to the merchant’s acquiring bank in under 60 seconds. Fortunately, there’s a light at the end of this tunnel!

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobile payments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan. Why Uzbekistan?

Ralf Germer, CEO and co-founder, PagBrasil Pix has been a giant windfall for Brazil and is now responsible for 90 per cent of bank transactions in Brazil. Through this collaboration, Bancard will offer this service to banks in Paraguay, enhancing convenience and financial accessibility for Paraguayan travellers.

The context and challenges of each impact the means, not the end, because the result of this digital revolution is very similar in all these regions: economic development, financialinclusion, and innovation,” says Juliana Etcheverry , Director of Country Growth – Latin America at EBANX.

Having established what regulatory challenges banks and fintechs should be aware of when leveraging banking-as-a-service (BaaS), and how the technology is advancing financialinclusion across the globe, we now turn our attention to emerging trends and if they are region-dependent.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. million to support SMEs in Chile.

These awards highlight companies and individuals whose fintech initiatives have contributed to advancing financial technology, promoting financialinclusion, and improving service delivery. Integrated with bank accounts and digital wallets in Pakistan, Hakeem provides customers with easy disbursement options.

“India has recently achieved unprecedented levels of financialinclusion and is actively promoting the adoption and growth of the online sector,” explains Rashmi Satpute , country director of India at EBANX. Including mobile money, APMs will represent around 63 per cent of African digital commerce by 2025.

Aadhaar-enabled Payment Service (AePS) AePS, in India, enables individuals to conduct basic banking transactions like d eposits, withdrawals, balance inquiries, bill payments, etc. without requiring a traditional bank account or debit card. Unlike physical cash or bank deposits, CBDCs are purely electronic.

Identity is key, fostering both financialinclusion — to the tune of 270 million new bank accounts as of March 2017 — and security for the transactions themselves. Mobile reigns here. Paytm has had its own competitive moat set in place, at least a bit, with its payments bank.

The idea is to “promote global interoperability across EMV QR Code payments,” the standards group said in a statement. The QR Payment Mark will not only tell consumers that a particular merchant employs the digital payments tool, but serve as an application indicator on a consumer’s mobile device. The Future of QR Code Payments.

In an interview with Karen Webster, Trulioo CEO Stephen Ufford said the roadblocks on the path to real financialinclusion and a network that truly spans the globe can be boiled down to one key challenge: crossing the Rubicon from analog to digital. The Bank Validation. The Business Side: Unlocking the Analog.

Titled, Explore China Your Way with UnionPay: China UnionPay Payment Service Optimization – Project Excellence 2024 , the ceremony was attended by Zhang Qingsong , member of the CPC People’s Bank of China (PBOC) Committee and deputy governor of the PBOC , and Xie Dong , Vice Mayor of Shanghai.

The Federal Reserve Bank is currently developing a new instant payment service called “FedNow” that will allow financial institutions to make instant payments. Features of FedNow Instant Payments With the FedNow payment system, financial institutions will be able to send and receive instant payments.

These services can include payments, lending, investing, insurance, and banking. The term fintech is short for financial technology, and it represents a shift in how money is managed, accessed, and moved in the digital age. These companies build digital-first experiences , often focused on mobile, automation, and user interface design.

CAN WE MAKE THE OFFLINE WORLD AS EFFICIENT AS THE ONLINE WORLD? The ability for busy people to shop 24/7/365 via a mobile device trumps the serendipity that everyone says is one of the great benefits of shopping in a physical store. So what would physical retail look like if it were run like the best online etailers ?

The fintech sector now represents 5% of total revenues generated by all banking, financial services, and insurance (BFSI) companies in India. It has since enabled seamless bank transfers, mobile recharges, bill payments, and digital insurance services. The company is now valued at USD 12.6 billion over 16 rounds.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content