This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Together the two companies will help banks and other financial institutions provide a more seamless onboarding and underwriting experience for their smallbusiness borrowers. Combined, the two solutions provide an underwriting solution that automates workflows, boosts performance, and enhances risk-adjusted returns.

But after years of finding SMBs too unprofitable to finance, lenders have to play catch-up to develop better underwriting processes for greater accuracy and efficiency. This presents a gap in the market and an opportunity for FinTechs to fill it with automated underwriting technologies, like an automated smallbusiness credit score.

Despite a surge in sales, smallbusinesses selling online can struggle to manage working capital, particularly as many rely on third-party marketplaces like Amazon that don't facilitate instant access to revenues. But most people forget that we're still talking about smallbusinesses with a limited number of resources.".

has abruptly cut off credit to smallbusiness customers. Georgia-based Kabbage claims it has provided smallbusiness borrowers with over $9 billion in loans as of its 2009 establishment. Kabbage is now said to aim to be an intermediary connecting people with SmallBusiness Administration ( SBA ) loans.

As service providers in the business of disasters and disruptions, insurance companies have had a front-row seat to the ways the pandemic has affected their smallbusiness policyholders. But as Pogreb highlighted, smallbusinesses also have an opportunity to change the way they interact with their insurance providers, too.

Imagine a suite of AdviceRobo agents: One analyzing psychometric data, Another adjusting for behavioral shifts, A third scanning macroeconomic risks. In insurance , our agents help underwrite policies using behavioral data, making coverage more accessible for underserved or high-risk segments. And with response times as fast as 0.03

Use of alternative finance (AltFin) sources among smallbusiness (SMB) owners is on the rise, but still has a long way to go before it poses a legitimate threat to traditional banks’ market dominance. Mercator Advisory Group data released earlier this year found that 27 percent of smallbusinesses in the U.S.

To give you some clarity, here’s a practical guide that answers the most common questions smallbusiness owners have about credit card processing. In fact, ResearchAndMarkets.com forecasts the global credit card payment market to grow to $762.16 billion by 2027exhibiting a 7.8% Learn More What is Credit Card Payment Processing?

With the coronavirus forcing small- to medium-sized business (SMB) owners to digitize, adjustbusiness models, close their doors or furlough staff, entrepreneurs are quickly recognizing that the old ways of operating no longer cut it in today’s volatile, remote world.

In the latest quarter, adjusted earnings of a dime per share was up two pennies from last year, and revenues of $110.2 Management said on the call that underwriting standards would tighten, which, as CEO Noah Breslow said in remarks on the conference call with analysts, reflects the current stage of the lending cycle.

Most business still looked to banks, despite the fact that in the wake of the financial crisis and subsequent credit crunch, lending from banks more or less ground to a halt where SMBs were concerned. But as SMBs nationwide continued to need access to credit, a half-decade ago was a great time to start a smallbusiness lending firm.

I think this is going to impact us for quite a while and [the PPP funds] buy us time to adjust some of our expenses if we need to. Broadly speaking, the fullness of all of those loans/grants should all be reimbursed to the financial institutions (FIs) that started the underwriting process.

In an interview with PYMNTS, Sebastian Rymarz, CBO at Fundbox , said credit decisions can be rendered in minutes, with revolving lines of business credit accessible for up to $100,000. In addition, funding can be available as soon as the next business day. Per Fundbox, the value of unpaid smallbusiness invoices stands at $825 billion.

One such example is Ithaca, New York-based Alternatives Federal Credit Union , which teamed up with local government entities and other agencies in its county to pool forgivable loans of up to $4,000 apiece for Ithaca’s smallbusinesses. Thinking Outside The Lending Box. Innovating Credit Products.

Fear is holding back smallbusinesses from trading internationally, according to a report from HSBC late last year. Specifically, a lack of international business knowledge and experience has small suppliers reluctant to step onto the global stage. Data is critical to linking smallbusinesses with new funding.

For Q1, OnDeck forecast an adjusted net income of $5 million to $9 million, on the high side of analysts’ forecasts of $8.5 The last year has been an active one for OnDeck, a lending platform that underwritessmallbusinesses online and then resells the loans to institutional investors. smallbusinesses this year.

smallbusiness lender, to White Oak Global Advisors, noted Financial Times. There is also worry over looser underwriting, which has seen lenders stretch out terms for borrowers while pushing up loan-to-value ratios and debt-to-income ratios — an echo of the subprime mortgage crisis. It recently sold LDF , a U.K. trillion U.S.

I talked about eBay and Etsy, but theres also SaaS businesses for which embedded payments became incredibly important as a revenue source. Today, theres research showing that just about a third of smallbusiness owners will rely on a platform for services, banking services, but that will grow to three quarters over the next five to ten years.

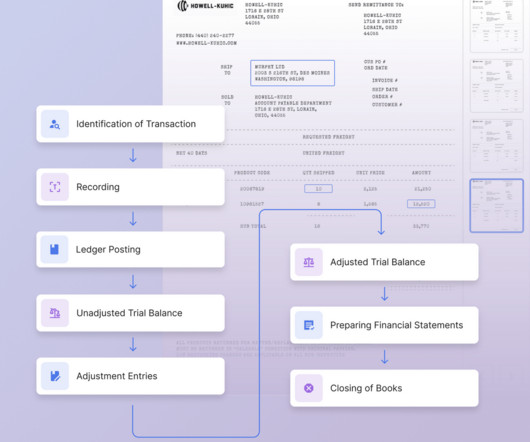

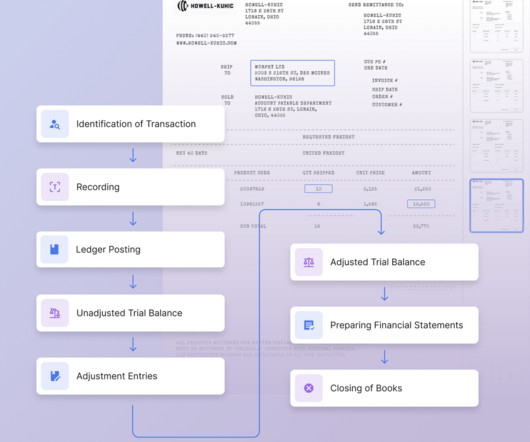

They have to be adjusted as shown in the next steps. Step 3: Adjust bank balance The discrepancy in the two balances has to be identified and checked on an individual transaction basis. Bank statements must be adjusted by adding pending deposits (deposit-in-transit) and deducting pending outgoing checks (outstanding checks).

They have to be adjusted as shown in the next steps. Step 3: Adjust bank balance The discrepancy in the two balances has to be identified and checked on an individual transaction basis. Bank statements must be adjusted by adding pending deposits (deposit-in-transit) and deducting pending outgoing checks (outstanding checks).

Use-cases for real-time payment capabilities continue to grow for consumers, smallbusinesses and corporates, while the open banking business model is proliferating beyond the ability for FinTechs to loop into their customers’ bank account data, and into new opportunities like enhanced smallbusiness loan underwriting and automated accounting.

In an interview with Karen Webster, Qwil CEO Johnny Reinsch shone a spotlight on the ways that quickened payments can benefit smallbusinesses, gig workers and their client firms alike. Qwil makes it possible for businesses to pay their contingent workforces instantly, through what is known as Liquidity as a Service.

Most business still looked to banks – despite the fact that in the wake of the Financial Crisis and subsequent credit crunch lending from banks more or less ground to a halt where SMBs were concerned. A few years ago we saw a lot of small firms experimenting in this space – and there was a ton of money poured into the segment.”.

Businesses that are unable to receive funds from these programs are thus looking to external sources, including alternative and traditional lenders. Receiving funding quickly is critical for SMBs, with PYMNTS research showing that the COVID-19 pandemic has negatively affected 90 percent of smallbusinesses in some way.

By the numbers, First Data reported adjusted earnings per share of $0.28 The CEO called out “better salesforce and merchant retention” tied to its North American Global Business Solutions segment, which saw revenues of $971 million, a 3 percent increase on an adjusted basis. Welcome to the U.S., Chinese consumers.

That’s adjusted for inflation. We all know that lax underwriting standards came home to roost in this sector. First things first. Some things have barely budged. The median household income in the U.S. is up about 5 percent, as noted by the Census Bureau and cited by The Wall Street Journal. Mortgages ?

Instead of individually setting up a merchant account with banks or other financial institutions, which can be a lengthy and complex process, businesses can quickly onboard through PayFac. Here’s how it works: Sign-up: Businesses can easily sign up with a PayFac provider who becomes the master merchant.

Smallbusiness funding platform Kabbage was founded in 2009 with a mission to use big data to help underwritesmallbusiness loans. The 75,000 smallbusiness customers on Kabbage’s platform hail from all 50 U.S.

Amazon could also look to integrate this tech into its Whole Foods stores or rumored independent grocery business in the future. Prime Day: Amazon’s plan to adjust payment habits. Today, Amazon has expanded its business lending to the US and UK. In consumer, Amazon offers lending in the US in the form of partner cards.

Yellen made an announcement that was eagerly welcomed by an often neglected sector of smallbusinesses across the country: The U.S. The fight for smallbusiness survival is tougher than ever before, especially for minority- and female-owned businesses.

Yellen made an announcement that was eagerly welcomed by an often neglected sector of smallbusinesses across the country: The U.S. The support program comes at a pivotal moment both for CDFIs and the smallbusinesses in the communities they serve. The state of minority-owned smallbusinesses.

The smallbusiness sector has also seen an increase in adoption of contactless options. While 40% of smallbusinesses remained nonoperational due to the pandemic, 27% of those that continued to accept on-premise payments reported an increase in contactless payments made through smartphones and contactless cards.

I really have to give kudos to the federal government for recognizing the need certainly for smallbusiness, for citizens and for larger enterprise firms. The reality is once these companies can come back to work and can start their businesses back up from where they left off, they will start paying rent again.”.

While smallbusinesses are scrambling to obtain emergency funding, the COVID-19 crisis has exposed some of the shortcomings of the big bank system. This is the story and timeline of a small banker’s experience with PPP loans. Smallbusinesses are losing money fast and worried about being able to pay their employees.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content