This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Online mortgage originator Better.com is deploying AI within its internal and external operations to drive efficiencies. The New York-based company deployed its AI-driven mortgage origination tool, Tinman, in 2022, President and Chief Operating Officer Chad Smith told Bank Automation News.

Life insurance companies rely on accurate medical underwriting to determine policy pricing and risk. These calculations come from specialized underwriting firms that analyze patients' medical records in detail. One leading life settlement underwriter found their process breaking under new pressures.

Merchant underwriting is an essential component of the payment processing industry, ensuring the safety and security of electronic payments. This article will explore the mechanics of merchant underwriting, from the essential steps involved in the process to the factors influencing it. What is merchant underwriting?

Affirm underwrites every individual transaction before making a real-time credit decision and only approves consumers following an assessment that evidences their ability to repay. Affirm’s expansion to the UK adds to its presence in the US and Canada. Consumers will always know what they owe upfront.

The right features in a robust loan origination software can significantly transform the process. With a straight-through process (STP)-based Loan Origination System (LOS), lenders can not only improve the customer experience but also reduce the customer onboarding TAT significantly. What is a Loan Origination System?

Finflux by M2P Finflux by M2P is an API-first platform that offers comprehensive solutions for Loan Origination (LOS) and Loan Management System (LMS), designed to streamline lending operations across over 15 products, including personal loans, auto loans, education loans, and gold loans. Lets dive in!

PDF → Excel Convert PDF bank statements to Excel Try for Free Loan origination is the process of applying for and obtaining a loan, including all the steps and activities that are involved in evaluating, approving, and disbursing the loan. It also includes various other steps such as underwriting , documentation, and funding. The

Open data, in turn, enriches these offerings, enabling innovative credit scoring and risk assessment beyond traditional banking channels. By combining payment flows with broader financial datasuch as rental history, savings patterns, and income variabilitylenders can offer dynamic, real-time credit assessments.

The partnership enhances Capitalise’s lending origination service by removing friction from the funding process. “Open Banking sits at the core of SME credit decisioning and brings confidence to underwriting risk assessments,” Capitalise Co-Founder Ollie Maitland said. are embracing open banking technology.

The loan origination process has historically been a complex and time-consuming endeavor for both commercial lenders and borrowers. We’ll also see how Nanonets can help your business achieve loan automation and improve the loan origination process and business efficiency.

Baker Hill has spent decades providing loan origination services to its bank clients. And while loan origination and portfolio management has challenged lenders for years, Baker Hill Senior Director of Solutions Management Mike Horrocks tells PYMNTS why some of those challenges now have a modern twist.

This includes employing machine learning algorithms to automate parts of the loan application and underwriting process, as well as using digital platforms to facilitate communication between borrowers, lenders, and other relevant parties. AI is poised to revolutionize loan origination.

After OnDeck announced that it had notched better-than-expected earnings and loan volume, LendingClub followed suit with with a report that saw the firm beating Wall Street’s estimates for earnings and new originations. That growth came despite widening net losses and an environment where interest rates are beginning to climb. “We

Origination Scores Offer Targeted Insight. Origination scores add significant value above and beyond the FICO ® Score, which is based solely on the data found in a consumer’s credit bureau file. customers assessed only by their FICO ® Score). Machine Learning Enhances Origination Decisions.

Lender underwriting practices, such as underwriting borrowers with higher debt-to-income ratios, lower down payments, or lengthier repayment periods none of these practices can be identified in the traditional credit bureau file. So what are some of these factors? An Effective Rank Ordering Tool Through The Cycle.

invoice insurance provider Nimbla is teaming up with the credit risk assessment firm Wiserfunding , according to a report in Crowdfund Insider on Friday (May 29). The partnership is a result of the launch of the FinTech task force Innovate Finance , which took place in March, the report said.

From application submission to underwriting and funding, mortgage automation can simplify the steps involved in getting a loan approved. Credit Checks: Credit checks are an essential part of the mortgage application process as they help to assess the borrower's creditworthiness.

If users fail to make timely minimum payments, they will be assessed late fees. Originally, Amazon considered creating an online marketplace where lenders would compete to offer SMBs credit, CNBC was told. Originally, Amazon considered creating an online marketplace where lenders would compete to offer SMBs credit, CNBC was told.

A Brief History of Fintech The origins of fintech can be traced back to the 1960s. They use alternative credit scoring methods and automated underwriting. Big Data Analytics : Helps predict customer behaviour, optimise pricing, and assess creditworthiness in real time. Artificial intelligence will play a greater role.

Our findings tell an interesting tale: Banks have been mildly decreasing their car loan underwriting standards. As part of our study, we examined underwriting standards during the 2009-2016 timeframe by looking at FICO® Score distributions for consumers who opened new car loans in the prior six months.

Lendbuzz’s financing model, which is powered by machine learning and proprietary algorithms, allows it to better assess the creditworthiness of consumers with limited U.S. “We developed a unique underwriting platform based on alternative data points to evaluate credit risk. with 27 million being working professionals.

FICO is strengthening its position in the corporate underwriting space with a new solution for SME lenders. The company said Wednesday (April 5) that it is rolling out its Origination Manager Essentials solution for mid-market banks and credit unions. ” . ”

For me and my co-founder Gurprit, it’s about leaving the world a little better than we originally found it. While open banking has massively improved the loan underwriting process by making it genuinely personalised, the industry hasn’t actually improved outcomes for those that get declined. They join us for the mission.

12) said Trade Ledger will link its deep technology capabilities into Tradeplus24 to enhance small business (SMB) receivables finance underwriting by analyzing supply chain data , including individual invoices. According to Trade Ledger CEO and Co-Founder Martin McCann, that capability means lower small business loan origination costs. “A

A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. And financial institutions use FICO® Scores to underwrite lending to millions of people so that they can achieve their financial goals like buying a first home or starting a business.

Mortgage processing automation helps companies reduce the manual workload involved in mortgage origination and processing, in order to improve accuracy and efficiency. Underwriting: The lender evaluates the borrower's application and documentation to determine the level of risk associated with the loan.

In this final blog in my series, let’s explore how can lenders take advantage of advanced modeling technology to cost-effectively originate profitable, compliant decisions that protect your bottom line AND deliver an optimized customer experience to the best customers. MYTH #1: We already use a credit bureau score to assess application risk.

Morgan’s financial strength and Slope’s innovative approach to credit risk assessment and monitoring. The fact that they not only use AI for initial underwriting, but also for the ongoing risk monitoring of the portfolio, is what really attracted us to Slope. The partnership brings together J.P. By combining J.P.

Improved risk assessment for credit-ready consumers FICO® Score 10 T addresses lenders’ desire for more effective credit risk assessment for consumers with limited credit history, thin files or new to credit. The validation results for FICO Score 10 T demonstrate improved credit risk prediction for this segment of the population.

Trade Ledger operates an open banking platform for banks to assess lending risk to their corporate customers in real time. “A major problem for banks and other lenders across the globe is the cost, effort and perceived higher risk of loan origination in the SME sector in particular,” McCann said at the time. ” .

It helps lenders evaluate borrowers' creditworthiness, assess the risk of default, and ensure that only qualified applicants are approved for loans. Traditional underwriting processes may not assess creditworthiness accurately for a borrower who derives income from non-traditional sources.

According to the publication, citing reports from Beijing media group Caixin Media, banks will be required to obtain primary, original documentation from the corporate borrower and its trading partner to stronger finance underwriting. Technology, he said, is key to that endeavor. “As

This leads to ‘double counting’ in the underwriting process, which affects affordability assessments. ” Ensuring good consumer outcomes ClearScore originally developed the Clearer direct settlement technology in 2023 and worked with personal loans provider Abound on a pilot project to build out the proposition.

Finalists in the corporate categories were evaluated based on impact, sustainability, practicality, interoperability, and creativity, while individual submissions were assessed on contributions to the Singapore fintech sector. Four finalists were shortlisted in each category. The company replaces traditional B2B payment methods (e.g.

Automate as much of the underwriting process as possible. The typical merchant onboarding process has a number of different steps that need to be followed before an underwriting decision can be made, as highlighted in the table below, this is typically a 3-5 day process. 2020 McKinsey Global Payments Report).

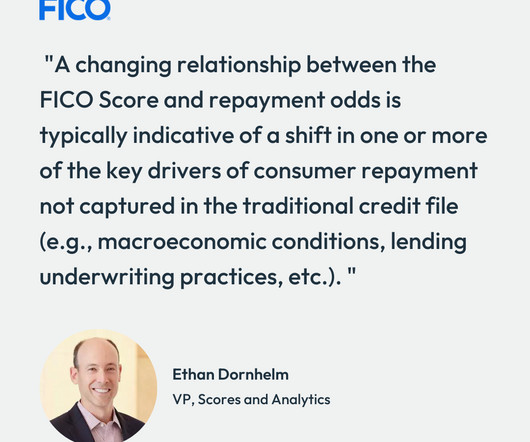

originations). macroeconomic conditions, lending underwriting practices). The upshot is this: whether it’s called “FICO drift”, “FICO inflation” (or deflation for that matter!), Figure 1 plots the odds-to-score relationship specifically on existing bankcard accounts, but we have observed similar trends across other products (e.g.,

Traditional areas like fraud prevention (65%), credit underwriting (62%) and regulatory compliance (58%) are still heavily prioritized, reflecting that these were some of the first uses of AI in banking and continue to be critical for reducing losses.

When Baraa Koshak launched Abwab AI three years ago, his aim wasnt to build another lender, it was to solve the deeper, structural problem holding back SME finance across the Middle East: inefficient underwriting. We can enable that capital to reach actually these SMEs without necessarily being the direct originators in the market.

Gold Loan Management System Gold loan management system streamlines the management of gold-backed loans, helping lenders enhance efficiency, ensure compliance, and optimize risk assessment. Core Capabilities of Finflux by M2P Advanced Appraiser Module : Ensures precise gold valuation with reliable and accurate assessments.

Credit Underwriting Credit Underwriting is the process by which a lender (such as a bank, credit union, or fintech company) assesses the creditworthiness of a borrower before granting them a loan or line of credit. They cater specifically to large corporations and high-net-worth individuals.

Loan Management System (LMS) is a digital solution designed to handle the complete loan lifecyclefrom origination and disbursement to repayment and closure. By analyzing borrower behavior, loan performance, and market trends, LMS provides insights that enhance risk assessment and optimize loan offerings.

” A study by deBanked and Bryant Park Capital in 2016 aimed to assess confidence in the merchant cash advance industry, and found that 91.7 ” A study by deBanked and Bryant Park Capital in 2016 aimed to assess confidence in the merchant cash advance industry, and found that 91.7 We come in un-collateralized.”

From origination to servicing, Finflux by M2P delivers unmatched flexibility and scalability, making it an ideal choice for NBFCs, banks, credit unions, fintech companies, microfinance institutions, and lending institutions of all sizes.

Rather than relying solely on formal credit histories, GXS taps into alternative data, such as gross merchandise value (GMV) from platform sales, to assess creditworthiness. Pei-Si believes this type of contextual underwriting is key to unlocking access for underserved users, calling it a true example of credit innovation in action.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content