This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Project Mandala was carried out in collaboration with the Reserve Bank of Australia, the Bank of Korea, Bank Negara Malaysia, and the Monetary Authority of Singapore.

Once a customer has disputed a charge, a your acquiring bank will begin going through a specific procedure to resolve the issue. Visa Chargeback Reason Codes In 2018, Visa consolidated its list of reason codes into 4 categories: fraud, authorization, processing errors, and consumer disputes. Declined Authorization 11.3:

This was conducted as part of the Monetary Authority of Singapore’s (MAS) Project Guardian , a global initiative involving industry leaders and policymakers to enhance liquidity and market efficiency through asset tokenisation.

Businesses must proactively assess fraud risks, implement adequate procedures, leverage technology for fraud detection, and foster a culture of compliance to avoid regulatory penalties. Compliance requires proactive fraud risk assessment, the implementation of preventive procedures, and a culture of accountability. What’s next?

This routing allows the processor to request authorization for the transaction from the issuing bank, which then approves or denies it based on factors like available funds and fraud checks. Routing : The payment processor routes the transaction request to the appropriate issuing bank for authorization.

A data breach occurs when cybercriminals infiltrate your systems and access sensitive information without authorization. And painful account recovery procedures await all users who must reset passwords across potentially dozens of breached websites. What Is A Data Breach?

We will explore these changes in detail, helping you understand the processes and mechanisms for restricting physical access to cardholder data, how physical access controls manage entry into facilities and systems containing cardholder data, and how physical access for personnel and visitors is authorized and managed. PCI DSS v4.0

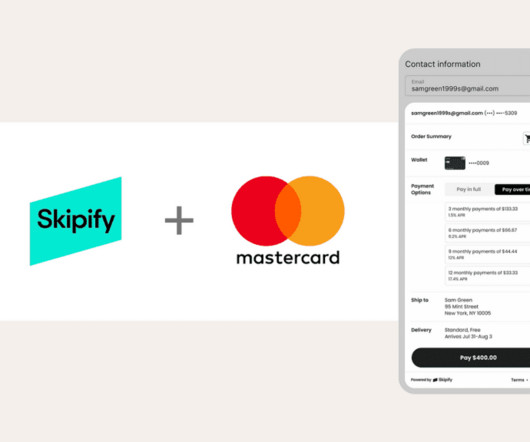

Skipify will work behind the scenes with Mastercard to ensure the entire process is fast and secure, positively impacting authorization and conversion rates. Merchants face expensive, complex setups, juggling multiple provider contracts and navigating inconsistent operational procedures.

The European Securities and Markets Authority (ESMA), the EUs financial markets regulator and supervisor, is launching the first selection procedure for the Consolidated Tape Provider (CTP) for bonds.

For full details on the report, click the link below: [link] FCA Offering Pre-Application Support Service (“PASS”) The Financial Conduct Authority (FCA) is now offering Pre-Application Support Service (PASS) to cryptoasset, payments, and wholesale firms considering applying for registration or authorisation in the UK.

Establish protocols for communicating with external parties, such as law enforcement, in multiple languages: Knowing how to quickly share info with authorities in various countries can speed up response times. Train employees regularly on these policies and procedures Make training available in all relevant languages.

TL;DR An ISO (Independent Sales Organization) is a third-party company authorized to manage merchant accounts and provide payment processing services on behalf of acquiring banks. Simply speaking, an ISO—or Independent Sales Organization—is a third-party payment processing company that is authorized to handle merchant accounts for businesses.

Regulatory reviews from the Bank of Italy, UIF, and the European Banking Authority (EBA) have identified key shortcomings in the management of vIBANs. Regulatory oversight intensifies Authorities such as the EBA, UIF, and national regulators are raising concerns about vIBAN compliance.

On 25 September 2024, the UK Financial Conduct Authority (FCA) published its long-awaited Consultation Paper (CP24/20) setting out proposed changes to the safeguarding rules applicable to electronic money institutions (EMIs) and payment institutions (PIs) (together, payments firms). What does this mean for Payments firms?

In addition, the report recommends deepening the collaboration between banks and authorities through platforms like COSMIC —a digital system enabling financial institutions to share customer risk information securely. The IMC’s recommendations aim to adapt Singapore’s AML framework to counter increasingly sophisticated criminal methods.

Antoms card processing volume grew over 10 times from that of previous year, while delivering top notch authorization rates to its global enterprise merchants. Antom continues to strengthen its payment processing capabilities across all payment channels.

There are also risk holds—a routine procedure that most companies experience within the first few weeks of processing with a new merchant services account. In this context, they accept the funds from the sale once a card is authorized and deposit them into the business’ bank account. Step 3: The card is authorized.

Below, we present a meticulously curated list that highlights the transformations in requirements and test procedures from PCI DSS v3.2.1 Defined Approach Requirements and Testing Procedures 1.1.1 by reviewing documented procedures. by reviewing documented procedures. to PCI DSS v4.0: PCI DSS v3.2.1 PCI DSS v4.0

Safeguarding customer funds The Financial Conduct Authority (FCA) has proposed significant changes to the safeguarding regime for payments and e-money firms. Employees should be well-versed in the safeguarding procedures and understand their role in protecting customer funds. Engaging external auditors may provide additional assurance.

The European Banking Authority (EBA) published a No Action letter advising the EU Commission, EU Council and EU Parliament to ensure that, in the long term, EU law needs to avoid a dual authorisation under two pieces of EU law for the activity of transacting electronic money tokens (EMTs).

The European Banking Authority (EBA) has issued a No Action Letter to EU policymakers, advising against dual authorisation requirements for crypto-asset service providers (CASPs) transacting in electronic money tokens (EMTs) under both the Payment Services Directive (PSD2) and the Markets in Crypto-Assets Regulation (MiCA).

Requirement and Testing Procedures 3.2.a Requirement and Testing Procedures 3.2.a Requirement and Testing Procedures 3.1 Minimize cardholder data storage by implementing policies, procedures, and processes for data retention and disposal. Protect sensitive authentication data before authorization. PCI DSS v3.2.1

A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. It authorizes or declines payments based on available funds and fraud checks. Ideally, you want instant or same-day fund settlement.

Under these conditions, the banks must then test their response and recovery measures, including activating emergency procedures and contingency plans and restoring normal operations. Instead, in the stress test scenario, a cyberattack succeeds in disrupting a bank’s daily business operations.

The requirement mandates that software development procedures must be documented and examined to ensure that all security considerations are integrated into every stage of the development process. It required code changes to be reviewed by others than the author, following secure coding practices. is now 6.2.2. PCI DSS v3.2.1

Banks are expected to apply the follow guidance in connection with their digital asset custodial services: Governance and risk management : Prior to launching digital asset custodial services, banks are expected to undertake a comprehensive risk assessment and to implement appropriate policies and procedures to mitigate identified risks.

Given the cross-border nature of financial crime, the new authority will boost the efficiency of the anti-money laundering and countering the financing of terrorism (AML/CFT) framework, by creating an integrated mechanism with national supervisors to ensure obliged entities comply with AML/CFT-related obligations in the financial sector.

What Ukrainian Banks Should Do Now Dont wait - start adapting processes to European standards now Invest in compliance - AML/KYC procedures will become critically important Prepare teams - specialists in European regulation will be needed Develop automated currency control systems for SEPA operations This is an important step, but not a revolution.

This follows a 2022 penalty of 70,000 for delayed accounts and after previous attention of the UK’s Financial Conduct Authority in 2019 on AML compliance. The fine of 3.5 The cumulative record paints a picture of a company that is still developing its control environment in spite of its fast growth and global footprint.

Cybercriminals are constantly one step ahead of government regulators, developing new and inventive schemes faster than the authorities can quash them. BitGo On Strengthening Cryptocurrency Exchanges’ AML/KYC Procedures. percent of the global gross domestic product (GDP). billion by 2024. billion in 2019, including $2.8

A payment gateway solution is a service that authorizes credit card payments and processes them on behalf of the merchant. A Payment Gateway for a mobile app is a service that authorizes credit card payments and processes them on behalf of merchants. It should also be easy for you to track conversions and manage your payments.

GSR, a global cryptocurrency trading firm and liquidity provider, has been granted a Major Payment Institution (MPI) license by the Monetary Authority of Singapore (MAS). This license allows its subsidiary, GSR Markets Pte. located in Singapore, to provide digital payment token services.

This is to ensure that critical data is only accessible by authorized personnel, thereby enhancing the security posture of organizations handling sensitive payment information. They were documented and had to be approved by authorized parties (7.1.4). Required privileges must be approved by authorized personnel.

But in practice, many MCA funders either ignore reconciliation requests altogether or use procedural hurdles to render the right meaningless. “MCA funders will claim the right exists, but then impose layers of opaque documentation requirements and tight procedural deadlines. For secured lenders, this matters.

Establish protocols for communicating with external parties, such as law enforcement, in multiple languages: Knowing how to quickly share info with authorities in various countries can speed up response times. Train employees regularly on these policies and procedures Make training available in all relevant languages.

This project is a joint effort with the Hong Kong Monetary Authority (HKMA) and is part of ongoing research into the development of CBDC systems, considering privacy concerns. Project Aurum , also from the Hong Kong Centre, has entered a new phase focused on the privacy aspects of retail CBDCs.

The outcome of this procedure will be published on the ECB’s website when it has been finalised in 2025. In January 2024, the ECB put out a call for potential providers of digital euro components and related services. It has now concluded this call and invited selected bidders to tender.

While deregulatory measures such as revisiting the Open Banking Rule may gain momentum, their implementation faces procedural and legal challenges. With its record of bipartisan enforcement actions and new authority to regulate big tech, the agency may adapt rather than disappear.

In addition to streamlining business procedures, this also frees up their time to work on more strategic initiatives and increase client satisfaction. For instance, software that automates regulatory compliance tasks can , free up time for employees while lowering errors that can be quite expensive.

The organization said that “the aim is to explore the potentialities offered by this technology, and to identify concrete cases integrating Central Bank Digital Currencies [CBDC] in innovative procedures for the clearing and settlement of tokenized financial assets.”

For instance, the new legal and regulatory framework means businesses dealing in crypto must review their policies and procedures and prepare for increased disclosure, transparency, and compliance with tighter regulations. Additionally, the MiCA regulation could create new challenges.

Different types of payment reversals exist, each with distinct procedures and implications. The most common types include chargebacks, refunds, and authorization reversals. Authorization Issues : Transactions that are not properly authorized can be subject to reversal. What is an Authorization Reversal?

The Financial Conduct Authority (FCA) continues its commitment to guiding firms on embedding the Consumer Duty by publishing two insightful reports. Robust processes: Established procedures for report production, involving relevant business areas and governance bodies.

regulators, including the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA). The FCA has expanded oversight of the crypto industry due to anti-money laundering (AML) and counter-terror financing (CTF) procedures. Thus far, the regulators have not raised any red flags.”.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content