This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Zelle Says P2P Payments Top One Billion Transactions. Everlink, FINTAINIUM Team up to Offer Real-Time B2B, B2C Payments. Everlink Payment Services is collaborating with workflow solutions firm FINTAINIUM to provide B2B and B2C payments in real time, harnessing the ISO 20022 worldwide standard.

Remittances As Global P2P On Ramps. That includes using technology to take the notion of simply moving money from one country to another to a new level, including sowing the seeds for the ignition of a real-time global, mobile P2P network that offers senders and receivers optionality, convenience and security.

Will this be the year that real-time payments — and, especially, peer-to-peer (P2P) — reach critical mass in the United States? He noted that P2P is the first application of real-time payments to gain traction, and said the arrival of that payments functionality is “long overdue.”. Streamlining the Onboarding Process. Building Trust .

The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. to fully embrace real-time payments for both B2B and B2C activity.”. Where We Stand In The US.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. Through this alliance, Thunes and MBANK will facilitate seamless money movement to and from the country.

If you look outside B2B or B2C, or consumer P2P, they are needed just about anywhere,” he said of APIs. However, according to Justin Goldsmith, senior consulting architect at Red Hat , in a discussion on the “State Of” APIs with Karen Webster, the impetus is there for U.S. financial services firms to cross the Open Banking Rubicon. “If

Peer-to-peer (P2P) payments are blazing a hotter path in the digital economy as the second half of 2019 gets underway – and there is fresh evidence that the payment method is not only growing, but helping to influence related endeavors. Venmo, of course, is not the only major P2P player in the game. Larger P2P World.

These individuals also expect faster payments in their day-to-day lives thanks to their interactions with peer-to-peer (P2P) payment apps. Millennials are among the top financial app users: 94 percent of surveyed millennials use P2P apps like Venmo and Zelle. Mobile disbursements are becoming critical for both B2B and B2C companies.

Visa introduced the Visa+ service in April last year to bridge the gap among various apps in the peer-to-peer (P2P) payments space, allowing for real-time payouts to participating digital wallets. This enables users to then utilize various P2P digital payment apps for further transactions.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-time payments when transacting with each other. Deep Dive: How P2P Payment App Providers Are Fending Off Fraudsters.

Such disruption and transformation can transcend use cases, said the executive, across B2B, B2C and P2P transactions. And to extend the discussion to P2P, Webster noted that there is much innovation within this space. Could, Webster asked, P2P be a font of disruption — but also an opportunity for banks?

The outmoded B2B payments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-time payments are becoming the norm. It works both ways as traditionally B2C sellers dip their toes into lucrative B2B waters. Keeping B2B Payments Honest.

MO offers various products catering to both business-to-business (B2B) and business-to-consumer (B2C) markets. MoMoney, the B2C product, offers loyalty programs, QR code payments, mobile top-up, cash withdrawal, and bill payments. These products include MoBiz, MoBills, MoPayments, and MoMoney.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. Stepping back from the granularities of B2C and B2B payments, though, the executive said the groundswell of faster payments is inexorable. Why B2B Lags. The Larger Picture.

The evolution of payments in Brazil has primarily been B2C and P2P, but despite these new products, the highest number of transactions remain in the B2B market. What are some other payment trends we’re seeing in the region? There is a lot of space for innovation in the B2B sector.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). So, from the beginning, start with the individual consumer. The Low-Hanging Fruit.

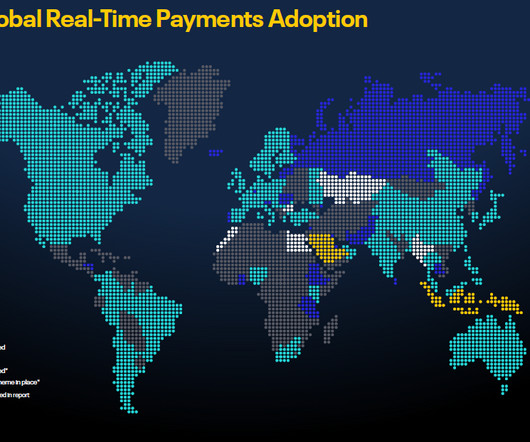

RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions. Current status of RTP adoptions around the world How RTP is used?

billion Cgtz is a B2C debt investment platform offering a diverse range of investment products tailored for individuals and small to medium-sized enterprises (SMEs). It serves clients in industries such as P2P lending, microfinance, banking, insurance, payments, e-commerce, gaming, social media, and more. CGTZ Valuation: $2.41

By contrast, related fields like business-to-customer (B2C) and peer-to-peer (P2P) have become familiar with quicker, more accelerated solutions like instant, real-time payments. These days, more companies utilize functions like Credit-as-a-Service (CaaS), which streamline and offer more channels for B2B providers.

Fiserv comes to the conversation with 30 years of insider industry knowledge, and on the heels of a year in which it moved more than $75 trillion across 30 billion digital payments in peer-to-peer (P2P), consumer-to-business (C2B) and business-to-consumer (B2C) transactions. In other words, it’s seen some stuff. Alphabet Soup.

That means the remaining were B2C and P2P transactions, representing a major gap — and opportunity — for B2B FinTech, payment and API companies to step in and expand use of the faster payment service. They range from financial giants like Mastercard and PayPal to smaller firms like Payment Rails, Figo and Dwolla.

Finally, Newkirk explained that Visa Direct will spearhead Visa’s drive for better domestic and cross-border money movement, empowering all payment flows including P2P, B2B, G2C and B2C, and putting the power of money movement in its clients’ hands.

Visa projects a $200 trillion market for global money movement flows (inclusive of B2B, B2C, P2P and gov disbursements), and is expanding its collaboration with Thunes to enable payouts to digital wallets and bank accounts as a core part of its plan to achieve that growth.

trillion B2B, B2C and P2P payments every year. The new network will also enable the payment system operator to deliver greater efficiency, more innovation and fair and equal access to B2B, B2C and P2P payments and the infrastructure that facilitates them. The payment systems in the U.K. processes more than £6.4

It includes benefit payments, too, and in a B2C environment, it could also include payments such as from an insurance company, said Estep. This is the percentage of payments made through P2P transactions using same-day payments. But when you look at that 1.9 13 percent. That’s represented by “web ACH credit transactions,” said Estep.

As real-time payments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Part of the reason that real-time P2P is popular is that there is a communication component to it,” she told PYMNTS. roughly two years ago.

That growth is being driven by convenience, noted Sievert, as A2A activity offers yet another opportunity to take some friction out of the payments experience, with both person-to-person (P2P) and business-to-consumer (B2C) payments driving the uptick in A2A activity, he said.

In reference to Issuer Solutions, TSYS has pointed to 614 million accounts on file, with 24 billion cardholder transactions and dominant market position in North America, Ireland and China, with market share as the second largest player in Western Europe.

With the OCC consent orders against BaaS banks and bad press plaguing B2C BaaS platforms, regulators are extra scrutinising when it comes to all types of BaaS platforms, catching those in the middle that are B2B or Business to Nonprofit.

Payments are moving toward greater speed, efficiency and choice – and in P2P payments, that’s led to the rise of financial technology giants. “P2P payments has not only one, but multiple ten-thousand-pound gorillas,” said Spottiswood. “B2B payments innovation seems to fall behind B2C and P2P,” she said.

The company also helps third-party organizations across various industries integrate instant payments with traditional payment tools into their existing payment and money movement use cases including A2A, P2P, Bill Payment, B2B and B2C disbursements. Launching Payfinia will help Tyfone further build on the instant payments experience.

Coverage includes Deposit Solutions ’ rollout of business-to-consumer (B2C) open banking channel Savedo in Switzerland. Open banking platform Deposit Solutions has brought business-to-consumer (B2C) open banking channel Savedo to Switzerland, the company said in an announcement. In the U.K. ,

The 2020 State of Disbursements: APAC Outlook Report by Rapyd has revealed the existing and preferred methods for getting paid across several transaction scenarios such as& P2P, B2C, B2B, and G2C.

It was a good week for wearables and their future, as the devices continued to show indications of strong promise on the B2C and B2B fronts. On the B2C front, it looks like customer enthusiasm for wearable devices is both growing and expanding. For the sizzle of the week, wearables wins with solid B2C and B2B scores.

The assets of alternative lenders, like P2P [person-to-person], are increasing, and yet, in most cases, they aren’t competing head-on with banks. B2B finance and payments have a reputation for being slow to innovate and adopt technologies that have long been established in the business-to-consumer (B2C) world.

The reason faster payments is so important, Proto said, is because the four major quadrants of the payments industry — P2P, B2B, B2C and C2B — are all beneficially impacted when it comes to the expedited movement of money and data. When it comes to P2P payments, Proto pointed to a shifting consumer mindset and, in turn, adoption.

Low-value payments, marked by high velocity, he continued, are typically P2P remittance, B2C disbursements and payroll, where ticket sizes are $50,000 and below. “If “High-value payments are going to be the supplier management systems between big companies and middle-market companies. That’s B2B Connect,” he said.

She noted that firms such as PULSE have enabled payments functionality spanning push payments, peer-to-peer (P2P) and business-to-consumer (B2C) for the past decade and that operating rules require funds to be available in customer accounts within 30 minutes.”.

We had historically focused on the P2P and B2C market opportunities and are very pleased to demonstrate that we are able to deliver services to the B2B markets around the world as we continue to evolve into a full-suite global FinTech company.”.

Singapore’s multi-currency payments startup MoolahGo revealed this week it secured an undisclosed investment from The Lippo Group as part of its Pre-Series A round, according to a company announcement.

The rise of faster peer-to-peer (P2P) payment services has had an unintentional ripple effect for businesses, banks and merchants. As a result, firms that are lagging behind in faster payments investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market.

Business-to-consumer (B2C) industries are just beginning to see use cases for these payments and do not appear to be innovating fast enough, as 93 percent of customers recently surveyed by PYMNTS said that payment speed does not quite meet their standards. The staying power of checks and cash.

The paper also looks at specific use cases, such as distributed KYC registries and low-value P2P/B2C payments. The Euro Banking Association said the EBA’s Cryptotechnologies Working Group will continue to research the topic of international payments and will evaluate the implementation scenarios in international payments.

Kohli said person-to-person (P2P) use cases are among the first to gain ground. especially, bill payments are proving to be valued by consumers and B2C transactions, as the gig economy and insurance disbursements are a strong use case for Citi’s clients. In the U.S.,

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content