This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In keeping with its constant dedication to providing cutting-edge services to its customers, National Bank of Kuwait (NBK) announced introducing a new service that allows customers to confirm payment transactions online through the NBK MobileBanking App, making itself as the first provider of this service in Kuwait.

More than three-quarters of Americans now prefer to pay their bills digitally, especially Gen Z and Millennials, who show a significant inclination toward mobile payments. However, this increase in digital payments also brings about heightened risks – almost one in five consumers surveyed has fallen prey to online identity theft.

Businesses and financial institutions (FIs) are constantly examining ways to make their customers’ accounts more secure, especially as more consumers go online to make purchases and transact during the ongoing COVID-19 pandemic. Developments From The Digital Consumer Onboarding Space. It also found that just 16 percent of U.S.

European Payments Initiative (EPI), the unified digital payment service committed to offering a sovereign digital payment alternative to European consumers, has welcomed five new members in Belgium. “It fits perfectly with our digital strategy to offer smooth and accessible payments for consumers and professional customers alike.”

With smartphone theft on the rise across the UK, fintech and mobile security platform, Nuke From Orbit , is launching a nationwide campaign to combat this growing crisis. More people are using mobile phones for their money management, which means convenience and, in some cases, improved financial responsibility. million Android users.

Five big banks in Belgium have joined the European Payments Initiative (EPI) to help spread the word about its Wero digital wallet across Europe. With the Belgian banks EPI Wero collaboration, gives the initiative more energy to provide more European customers with safe and unified payment options.

Since the onset of the pandemic, banking activities like opening new accounts and applying for loans are now being done virtually to socially distance and help curb the spread of the virus. This means consumers are turning more to digital tools, but unlocking and embracing the potential benefits of these tools has not been easy.

However, Apple Pay can also be used online. Information is kept on file and when customers make a purchase online, they sign into their account and use it to pay for their purchase. This type of digital wallet allows users to pay for online purchases without providing their card details to the website from which they’re shopping.

Featuring expert insight from companies like Absa and KFC, as well as extensive merchant and consumer survey data, the report highlights the convergence of commerce – an industry-defining trend that is set to deliver customer convenience and merchant efficiency.

We can hail a ride from a mobile app, and our transactions for all sorts of goods and services can be easily paid for from our phones. In 2019, 77% of US consumers were using at least one type of digital payment system. It’s no question that the world has been digitally transformed — both in business and in life.

American consumers have fallen for mobilebanking apps, but up to now, most businesses were not seemingly showing apps the same love. With the number of mobilebanking customers now outnumbering those who bank at branches for the first time, consumers have warmly embraced banking via mobile apps.

MB Way counts half of Portuguese bank account holders as its customers and holds a 45% market share of e-commerce transactions in the country. With MB Way e-wallet, customers can make EUR payments, send or request money, and manage funds using their mobile application, without having to input card details in every transaction.

The coronavirus pandemic has left consumers staying home when possible to stop the virus’s spread. These shifts have made digital banking and debit transactions more important than ever. FIs need to adjust their offerings accordingly to suit consumers’ new needs. The Paytm cards can be used both in-store and online.

Lingering economic uncertainty and growing fraud rates in multiple markets are prompting consumers to sharpen their focus on privacy and security. Eighty-one percent of consumers in one recent study said that trusting brands was a major factor in determining whether they would interact with them, for example.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. Company Name. Phone number. Source: PwC.

Multifactor authentication (MFA) and biometric scans are quickly becoming the norm in numerous fields, including online accounts for banks and other businesses. Robust digital ID verification practices could make many fraud schemes a thing of the past, but many banks and businesses have yet to adopt them. More than 6.2

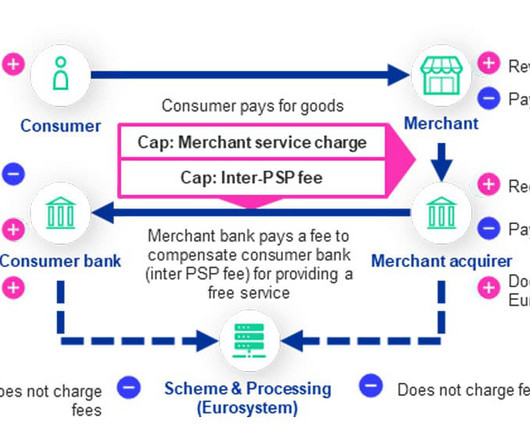

TRANSACTION FEE: A step-by-step overview of the digital euro compensation model Payment service providers will be able to charge merchants a fee for enabling them to accept digital euro transactions, the European Central Bank (ECB) has revealed, but a cap will be placed on the amount that it will be possible for them to charge.

Smartphones have become a ubiquitous part of life for consumers around the globe. They use their mobile devices for everything from checking the weather to posting on social media to pulling up real-time maps and using them to navigate to new destinations. The report surveyed 2,141 U.S.

billion) in 2022, according to Thant Mam Hein, assistant manager of sustainability at uab bank. Reports also show that approximately 50% of Myanmar’s adult population had a bank account in 2020, reflecting growth in financial inclusion and creating new opportunities for businesses and individuals. trillion (US$3.8 trillion (US$3.8

Banks have been forced to reduce or suspend in-branch activities to prevent the risk of infection at branches at least temporarily. The largest bank in the United States, J.P. Developments From Around The World Of Digital-First Bank ing. The global digital banking platform industry generated $3.95

While mint chocolate chip ice-cream might be the way to a foodie’s heart, MintChip digital currency is not the way to a millennial’s mobile wallet, apparently — at least not in Liberty Village, Toronto. Meanwhile, consumers in Asia have no such qualms, while the U.S. South Korea Is Mega Mobile. The news from the U.K.

Consumers were forced to swiftly adapt to a world where their primary way to interact with businesses or banks became digital-first, with the pandemic seemingly increasing the number of consumers turning to digital tools to conduct their financial activities. Developments From Around The World of Digital-First Banking.

Global highlights: January – December 2023, Source: Confidence Amid Chaos: Managing Fraud and Scams with Data and Analytics, LexisNexis Risk Solutions In financial services, new account creation attacks increased by 12% YoY, driven by increases on the mobile channel, primarily mobile browser.

At a time when 80 percent of apps ask for (and are usually given) users’ geolocation data, the fact that most mobilebanking applications still don’t is unacceptable, GeoGuard CEO David Briggs told Karen Webster in an interview. Two-thirds of all banking apps don't ask for location at all,” Briggs said. A Rude Awakening.

In a nutshell, that’s what PayPal Chief Operating Officer Bill Ready said is both the problem with and the path forward for in-store mobile payments. Among the problems consumers face in-store, no one seemed to complain about how they paid for the things they bought when there. To name but two. Because that part works fine. Ready said.

Israel’s Bank Leumi is planning to bring its online-only bank Pepper to the United States. Launched in 2017, Pepper is a digital banking venture that is initially offering individual accounts with plans to move into securities and mortgages, as well as joint banking options. She added that the U.S.

Despite the surge in mobile payments and onlinebanking , no one is predicting the disappearance of traditional banks and their brick-and-mortar branches. . Our research suggests that traditional FIs may be underestimating consumers’ willingness to embrace new, and some say better, ways to manage and spend their cash.

More consumers are turning to the omnichannel offerings of banks and credit unions (CUs) as they follow stay-at-home mandates, and cybercriminals are eager to launch attacks that make use of these channels. To find more about these and the rest of the latest headlines, download the Playbook.

Consumer shopping behavior has changed greatly during the last decade. Let’s dive into the subtleties of the smoothest payment process and find out everything about NFC mobile payments, including what they are, how they work, and how to use them. What are NFC Mobile Payments? How Do NFC Mobile Payments Work?

Consumers’ migration to using contactless payment methods more often for their speed and convenience was only accelerated during the onset of the pandemic last year. Fagan said CUs have seen deposit balances rise, a sign that consumers have been careful about building savings, reducing debt and compiling barriers against financial shocks.

Mobile card apps went from nifty to necessary when the darkest imaginings of last March had people picturing COVID-19 on every surface, suspended in every breath. Consumers are interested in applying mobile card management tools in different ways, however,” the report states. Meet the 2021 Cardholder.

Of course, many of our clients want to know more about millennial banking habits. FICO’s latest US consumer research survey found that large numbers of millennials are using their bank’smobile application regularly. As millennials flock to peer-to-peer mobile payments, Venmo has seen explosive growth. in Q1 2016.

That is just one of five critical findings highlighted in How We Will Pay 2019 , a PYMNTS, Visa collaboration examining how consumers use a wide range of connected devices to shop and make purchases. consumers who documented their shopping and purchasing experiences over a seven-day period in mid- to late-July of 2019.

A new study from Payments Canada reveals that Canadian businesses have a higher rate of payment fraud compared to Canadian consumers at 20% versus 13%, respectively, although the types of fraud were similar for both segments. Fraudulent charges on their bank or credit cards (20%). Purchase made from stolen debit card information (18%).

And thanks to new banking solutions, consumers are gaining new insights into their spending habits and how their daily decisions can make an impact on social and environmental issues near and dear to their hearts. Building smarter, more informed consumers. consumers billions of pounds each year. In the U.K.,

But in hopes of hopping on the holiday bandwagon — and providing data-backed insight in the hottest payment trends for 2019 — allow us to offer this list of a dozen ways that consumers (and some businesses) are paying now, methods that promise to play big roles in 2019. So, how will consumers (and some businesses) pay? #1:

As more Americans reach for their mobile devices when making purchases, providers are looking for new ways to secure smartphones. According to industry research, mobile commerce now accounts for nearly a third of the U.S. economy, with sales via mobile devices contributing more than $104 billion to the economy.

Online and mobilebanking interfaces have become must-have features for financial institutions in the digital age. Fifty-five percent of Americans have a full-service banking app on their phone, and 16 percent check these apps at least once per day. Around the Digital Banking World.

When I read about people infecting their Android phones with Gugi ––a Trojan malware that steals user credentials when consumers log into mobilebanking apps––by clicking on a link in a random text message, it’s clear to me that mobile phone users are in need of some security hygiene lessons. Why mobile hygiene matters.

The information stored inside your phone could soon be used to authenticate you to banks, credit card companies and other financial service providers. According to the Brazilian financial services firm, launched in 2014, it boasts a fraud rate just one-tenth that of larger banks and financial institutions.

MercadoLibre is an eCommerce platform similar to Amazon , with its own payments infrastructure that has grown into credit, mobile payments and asset management capabilities. I would say the most relevant variables across Latin America are banking penetration and credit card penetration,” Gimenez noted. percent in YOY growth.

In search of added convenience and simplicity, banking customers are migrating to online and mobilebanking interfaces, leaving in-person visits to brick-and-mortar branches behind. Around The Digital Banking World. How Banks Are Weaponizing Data To Fight Fraud.

The move to adopt mobile payments is progressing at a slow pace, largely because lack of a steady framework across shopping channels is slowing the adoption of mobile payments technology in North American and European markets. consumers and 74.6 consumers and 74.6 Baby steps toward mobile payments. percent of U.K.

“Consumers do not want a gap or friction at any point along the way, making it critical for financial institutions to understand and define member journeys and personas in both physical and digital channels.”. Consumers want the ability to continue transacting and conducting normal banking activities. It’s that simple.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content