This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This market includes a range of services and technologies that facilitate the acceptance, authorization, and settlement of payments across various channels, including online, in-store, and mobile. They require secure systems like point-of-sale (POS) terminals , online checkout gateways, or mobile payment solutions to process payments.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactless payments continues to grow. In fact, ResearchAndMarkets.com forecasts the global credit card payment market to grow to $762.16

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) Heres everything you need to know about internet card payment processing and how it can help your business grow.

According to the US Federal Reserve in 2022, general-purpose card payments reached $153.3 On top of that, 69% of Americans online in 2023 said they used digital payment methods to make a purchase. Customer – The person or business paying for goods or services using a credit card, debitcard, or digital wallet.

Some banks have chosen to develop their own in-house payment processing systems, delivering end-to-end services directly to their customers. Other banks have formed strategic partnerships with third-party providers. From internal solutions to partnerships, we’ll provide an overview of each bank’s approach.

Credit and debitcards, digital wallets , ACH transfers , and other digital payments have become the norm. TL;DR Choose a payment gateway compatible with your business model, whether for eCommerce, subscriptions, or omnichannel sales. Its a digital evolution of the conventional point-of-sale (POS) terminal.

Thats why weve compiled this guide to help you understand how POS systems work, the key features to look for, and how to choose and implement the right software for your retail store. TL;DR A point-of-sale (POS) system is a combination of software and hardware used by businesses to facilitate in-store sales.

The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobilePOS payments, and BNPL services. Looking to 2025, mobile payments and digital commerce are projected to exceed 10 trillion, with open banking and real-time payments leading growth.

Credit card merchant services are the systems, tools, and agreements that allow businesses to accept payments via credit and debitcards. Merchant services are essential to any business that wants to accept credit cards or debit cardsand theyre the backbone of modern commerce.

Whether you are starting a new online store or looking to grow your existing brick-and-mortar small business, you must make provisions for accepting credit card payments. The customer can make the credit payment physically by swipe, dip, or tap, depending on your point-of-sale (POS) system , which will capture the credit card details.

US consumers are increasingly turning to debitcards for their everyday transactions, driving a significant surge in the number of transactions and overall spending. The 2024 PULSE Debit Issuer Study reveals that in 2023, the total number of debitcards, transactions and annual spending per active card all saw substantial increases.

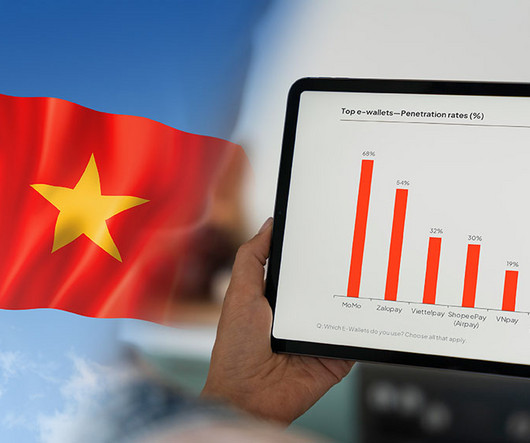

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

A merchant account is a business bank account that allows companies to accept payments, such as debit and credit card transactions, electronic funds transfers (EFTs), and Automated Clearing House (ACH) payments. This data is verified for accuracy and then forwarded to the cardholder’s issuing bank.

Heres what companies need to know about credit card integrations and how they can handle payments. TL;DR Online payments rely on API or hosted gateways with encryption and fraud detection, while in-store transactions require POS hardware with EMV chip technology and NFC capabilities. The more options, the better.

Fast forward to now where much has changed, and research anticipates contactless mobile payments to exceed one billion users globally by 2024. Customers can pay with their watch or phone just by tapping it on a card reader, and businesses can host an entire POS system on a mobile phone.

Fraudsters have grown adept at finding debitcards’ weak points, and merchants are struggling to keep up. Cybercriminals have more opportunities than ever to swipe debitcard numbers and PINs from online consumers, and false websites, large-scale data breaches and skimming tools can compromise account information.

A new report by Reputa, an online reputation monitoring system provided by Viettel, Vietnam’s state-owned telecommunications giant, offers an analysis of the country’s fintech sector and provides rankings of the most reputable fintech companies in Vietnam based on their online reputation and reach.

Debitcards have become an indispensable part of our financial lives, with the majority of American adults, spanning all demographics, now possessing at least one debitcard. Every merchant should prioritize taking the time to understand debitcard processing to streamline operations and enhance customer satisfaction.

That left FIs scrambling to “rapidly figure out how to get that same emotional and engagement outcome when the possibility of face-to-face is virtually nonexistent,” Randy Piatt , head of product solutions at card technology firm Ondot Systems , told PYMNTS in a recent conversation. Simple: Start with the cards.

A merchant services provider helps businesses process payments like debit and credit cards, Automated Clearing House (ACH)/eChecks, and other online transactions. These providers act as intermediaries between merchants, banks, and payment networks, ensuring transactions are processed securely and efficiently.

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobile payments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan. Why Uzbekistan?

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

Debit networks need to ensure that customers feel safe using the payment method, and that means imposing robust security measures and quickly cracking down on any instances of fraud that do slip through. The March Next-Gen Debt Tracker ® examines how debitcards are advancing into new areas to serve cryptocurrency holders and even children.

Thankfully, with mobile payments from Stax , you can quickly accept and process payments from your customers. Learn all about mobile payments and why you may want to consider joining the Stax family to streamline payments and boost your small business’ productivity. Mobile payments are much more secure than cash and checks.

Whether you run a small online store or a major brand, accepting electronic payments is a must for all businesses. According to Onbe, 73% of consumers prefer using digital payments like cards and payment apps. In order to receive card-based payments, businesses need to have a merchant account.

A payment gateway is a must-have for online stores. And the best way for online businesses to start accepting payments is with a payment gateway. TL;DR A payment gateway is a solution that securely reads and transfers a customer’s payment information to a merchant’s bank account—both for online and in-person transactions.

Accepting credit card transactions is no longer a decision of whether to but rather how to. With cashless now BEING king, credit and debitcards are the primary method for your customers to make payments. of consumer payments came through card payments. Card Network (e.g., Card Network (e.g.,

TD, America’s Most Convenient Bank® , today announced the launch of Tap to Pay on iPhone, enabling small and micro business owners across the U.S. to use their mobile phone for a seamless and secure point-of-sale (POS) experience.

The proliferation of ewallet platforms and mobile payment systems over the past decade has also revolutionized the way consumers interact with financial services. billion mobile wallet users globally , highlighting the rapid adoption of these convenient and secure payment options. As of 2023, there were over 4.5 With over 7.2

These trends included double-digit gross payment volume (GPV) growth, as measured year on year, double-digit transaction gains and traction in newer technology offerings — such as point-of-sale (POS) financing to help sellers log their own top-line growth. per share missed the Street estimate of $0.11.

The Emergence of Card Payments The introduction of credit cards in the mid-20th century marked a pivotal moment. Debitcards soon followed, enabling consumers to spend only what they had in their accounts. Over time, card networks such as Visa and Mastercard expanded globally.

As stated on the post-earnings conference call with analysts, CEO Charles Scharf said, “if confidence does deteriorate and the shelter-in-place orders stay on for longer, which is possible, then it wouldn’t surprise me that loss estimates would have to go up from this point.”. billion, also on reduced customer spending.

Since point-of-sale (POS) card terminals were first introduced by Visa in 1979, the payment system has hardly seen much advancement. Despite this, as fewer people stick to using cash, POS terminals are increasing in importance for large and small businesses alike. No additional hardware needed.

Overall credit card spend was down 29.9 percent and debitcard spend was off 18.1 Even grocery spending growth slowed to 25 percent on credit cards and 10 percent for debitcards, which gives a nod to the fact that consumers are likely “fully stocked up.” The Shift In Payments.

Bank earnings — taken together, let’s call them a mixed bag. Thus: Some banks bested results, some didn’t. The embrace of such trends by consumers, younger ones, continues apace, and all banks that disclose such metrics reported gains in the digital, online and mobile users. million mobile active users.

PayPal has inked a deal with point-of-sale (POS) company ebizmarts to help retailers offer both POS and digital payments. According to news from Mobile Payments Today , under the partnership, PayPal’s mobilecard product will be combined with ebizmart’s mobile app Magento.

Federal Reserve asset cap on Wells Fargo will last all year instead of through the first half, said the bank’s CEO Tim Sloan on Tuesday (Jan. Wells Fargo also reported single-digit gains in credit and debitcards. The bank also reported general purpose credit cardpoint-of-sale (POS) purchase volume of $20.2

In addition, Central JD Fintech is introducing the Dolfin wallet in Asia , and AMS Public Transport Holdings Limited along with AlipayHK is launching a minibus mobile payment system also in Asia. The system integrates payment processing with a point of sale (POS) for merchants operating online and in physical stores.

Apply for a merchant account A merchant account is typically set up through a payment processor or acquiring bank. This account serves as an intermediary between the business and the payment processor or acquiring bank, facilitating the secure processing of credit and debitcard transactions, among other forms of payment.

Credit card merchant fees are split between multiple key players- merchants, credit card networks, banks, and processors. Generally, here’s a breakdown of the types of payment processing fees you can expect: Interchange fees These are fees a merchant pays directly to the credit card provider.

This process is vital for businesses, as it enables them to accept payments through various methods, including credit and debitcards, electronic bank transfers ( EFT/ACH ), and digital wallets. Card Network: The credit card network sends the transaction details to the issuing bank (the customer’s bank) for authorization.

Credit and debitcards, and later, digital wallets, like PayPal, eliminated that friction for the online shopper, kept transactions secure, and reduced the risk from the merchant that items shipped wouldn’t be paid for. of them — yet their use in making online purchases is quite low.

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. In aggregate, these product development and investment decisions reveal that Amazon isn’t building a traditional bank that serves everyone.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content