This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Customers in this age of instant gratification always expect a smooth and seamless online payments experience. As a business owner, you must have a clear understanding of how online payments processing works to be able to create a hassle-free checkout process that will keep buyers coming back to your eCommerce store.

With so many payment options available from credit cards to mobile wallets it can be hard to know which methods are the best fit for you and your customers. Credit and DebitCards The majority of businesses we spoke with accept both credit and debitcards. The Most Popular Payment Methods 1.

In recent years, businesses have seen this massive shift from desktop to mobile devices which has forced them to develop apps with built-in integrated payment gateways. But when it comes to payments, mobile apps have to contend with a few unique challenges. Why Would Companies or Developers Want a Mobile App Payment Gateway?

In keeping with its constant dedication to providing cutting-edge services to its customers, National Bank of Kuwait (NBK) announced introducing a new service that allows customers to confirm payment transactions online through the NBK MobileBanking App, making itself as the first provider of this service in Kuwait.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactless payments continues to grow. In fact, ResearchAndMarkets.com forecasts the global credit card payment market to grow to $762.16

The future of commerce in Asia Pacific is on display at the Visa Asia Pacific Media Showcase, where the company announced a suite of product innovations and strategic partnerships to enable a new era of commerce for the region. Over the past 25 years, Visa’s global network has handled 3.3 trillion transactions.

Customers now prefer to skip the slow, fraud-prone process of swiping or inserting magnetic stripe cards. They simply tap their credit card , mobile device, or smartwatch to pay. Use case: Placing NFC tags on products allows customers to tap their phone to the tag and quickly pay for an item. Card emulation.

According to the US Federal Reserve in 2022, general-purpose card payments reached $153.3 On top of that, 69% of Americans online in 2023 said they used digital payment methods to make a purchase. Customer – The person or business paying for goods or services using a credit card, debitcard, or digital wallet.

Like most business owners, your instincts tell you to hop on the bandwagon and launch an online store for your business. From different types of online payment gateways and key features to look for, to tips to help you choose the right payment solution for your business and implement it. This is expected to grow to 22.6%

Sometimes, the cashier entered the product and quantity manually. Its the central hub for businesses to complete purchases, whether in-store or online. The hardware includes devices such as card readers, cash registers, touchscreen displays, barcode scanners, and receipt printers. Today, POS systems have evolved.

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) To accept online payments, you need a payment processor and payment gateway.

Credit and debitcards, digital wallets , ACH transfers , and other digital payments have become the norm. Opt for gateways that support diverse payment options like credit/debitcards, digital wallets, and international payments to accommodate customer preferences. According to Forrester, 69% of adults in the U.S.

We can hail a ride from a mobile app, and our transactions for all sorts of goods and services can be easily paid for from our phones. There are a wide variety of digital payment types, such as mobile POS systems, contactless payments, and digital wallets. All you need to use a digital wallet is a smartphone.

One of the biggest trends in fintech today is the rise of digital bankingproducts like mobile checking accounts and new debitcards. From Square to Paypal, a host of fintechs are creating products that let consumers spend money directly out of digital accounts using a physical card.

Accepting payments always comes with processes and fees, particularly when it comes to online or digital payments. TL;DR A payment link enables you to request and accept online payments without having to build a website or checkout page. Payment links are ideal if you don’t process a lot of online sales.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. They let buyers initiate payments by placing their mobile phone near a compatible payment terminal.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

Some banks have chosen to develop their own in-house payment processing systems, delivering end-to-end services directly to their customers. Other banks have formed strategic partnerships with third-party providers. From internal solutions to partnerships, we’ll provide an overview of each bank’s approach.

The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services. Looking to 2025, mobile payments and digital commerce are projected to exceed 10 trillion, with open banking and real-time payments leading growth.

Here are the inside details about what defines a payment solutions provider, how processing works, the credit card processing fees , risks, and more. TL;DR There are several parties involved in credit card processing. They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor.

They enable secure, efficient in-store and online payment processing and offer flexible payment options that customers demand today. Merchant services are comprehensive solutionstools, systems, and supportthat allow businesses to process in-person and online payments. custom software for a particular industry or market).

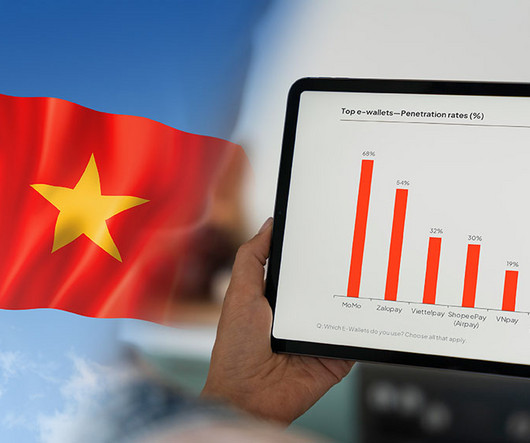

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

Armenia Population: +2,967,000 Capital, financial hub and largest city: Yerevan Gross domestic product (GDP) per capita: +$8,500 Access to a formal financial account (adults): 52.3 per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. per cent holding a credit card.

As an independent software vendor (ISV) or eCommerce platform, these statistics mean that you should focus on function when developing products for your clients. One way to do this is by offering credit card integrations. Heres what companies need to know about credit card integrations and how they can handle payments.

General Terms Merchant A business that accepts credit or debitcard payments. Transaction A payment made using a card or digital wallet. Authorization An authorization is a request to the cardholders bank to approve a charge. Acquirer (Acquiring Bank) The bank or processor that works with the merchant.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

Emerging markets have their own challenges when it comes to banking, where big, traditional financial institutions (FIs) are anything but efficient. Consider the fact that in Mexico it can take four to six months to open a business account — and as much as a year to get access to a debitcard. Widening Debit’s Acceptance.

Sweden’s Riksbank is assessing e-krona, a new form of digital currency that hopes to take the country a step closer to the creation of the world’s first central bank digital currency (CBDC), according to reports on Thursday (Feb. CBDCs are a digital form of traditional money issued and governed by a country’s central bank.

Debitcards are pivotal to a bank’s digital payment mix. In India, the number of debitcards in circulation is projected to witness a steady increase of 84.6 million cards by 2028. The total number of debitcards is anticipated to reach an impressive 1 billion*.

Fast forward to now where much has changed, and research anticipates contactless mobile payments to exceed one billion users globally by 2024. Customers can pay with their watch or phone just by tapping it on a card reader, and businesses can host an entire POS system on a mobile phone.

The COVID-19 pandemic has prompted traditional banks to take fresh looks at their digital initiatives and has given digital-only banks the opportunity to learn about the advantages and hurdles of serving customers primarily through online and mobile channels. Building Trust Between Banks and Consumers Online.

To regain some of that ground, Connie Davis, senior vice president at FIS , told PYMNTS in a recent interview, FIs — particularly credit unions (CUs) and community banks — must transform the way they think about digital offerings and connected experiences. That means they can compete more effectively against digital-only competitors.

As digital payments outpace plastic, UK banks must modernise card infrastructure or risk losing relevance to faster, cloud-native challengers. billion debit-card payments and logged 9.6 Over 98% of the population held debitcards for daily payments. Debit-card payments reached 24.5

Consumers will benefit from earning rewards for transactions via Crypto.com’s Crypto.com Pay ; merchants will benefit from being able to manage payments and services via both mobile and tablet devices. Also this week, Crypto.com announced that it would expand its offering to include banking services, credit cards, and stock trading.

The rise of FinTech, the increasing globalization of finance — and even ravages of the coronavirus, which is making us all bank and transact across phones — all have pointed to one simple, urgent question: Just what is a bank, anyway? In a recent PYMNTS study , What is a Bank: What U.S. As many as 36.8

Interest rates for savings accounts have become a prominent topic in recent years, driven by changing central bank policies and increasing inflation. In Singapore, banks have adjusted their offerings to attract customers by offering more competitive interest rates. inclusive of the prevailing interest rate of 0.05% p.a.)

A new report by Reputa, an online reputation monitoring system provided by Viettel, Vietnam’s state-owned telecommunications giant, offers an analysis of the country’s fintech sector and provides rankings of the most reputable fintech companies in Vietnam based on their online reputation and reach.

In an interview with PYMNTS, Scott Young , VP of Innovation at PSCU , noted that in the changing consumer environment, digital and mobilebanking are “table stakes,” but credit unions (CUs) must be conscious of how member payment preferences are evolving. More Comfort Online . Stepping Up On Credit .

Wells Fargo is launching a new, low-cost bank account — with access as well to a new digital payments service — in its latest move to push beyond a series of scandals. bank account, the bank noted in its announcement. The bank said it will also waive the $5 fee for younger account holders ages 13 to 24.

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobile payments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan. Why Uzbekistan?

Rivals Visa and PayPal have shaken hands over a joint plan to issue debitcards in Europe. PayPal enables users to leapfrog the card network and make payments directly from their bank account. Recently, however, it has been making inroads into more traditional retail banking territory.

That left FIs scrambling to “rapidly figure out how to get that same emotional and engagement outcome when the possibility of face-to-face is virtually nonexistent,” Randy Piatt , head of product solutions at card technology firm Ondot Systems , told PYMNTS in a recent conversation. Simple: Start with the cards.

The coronavirus pandemic — which has forced all of us online — is exposing just who in financial services has embraced digitization, and who is truly digital native. We now must bank entirely online, by necessity. And many of us must transact entirely online, by necessity, to get the goods and services we need on a daily basis.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content