This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

New moves from automakers and credit card companies are pushing vehicle commerce — or v-commerce — forward with new data showing it could reach critical mass by the end of the decade. Ptolemus expects the v-commerce market to be dominated by fuel and parking payments.

The UK governments decision to scrap the Payment Systems Regulator (PSR) and merge its functions into the Financial Conduct Authority (FCA) has divided opinion across the financial sector. He welcomed the move as a clear signal of intent to industry that the Government wants to restrike the balance when it comes to payments regulation.

In a mutual commitment to accelerating the adoption of an open digital wallet, global card networks Mastercard and Visa announce their agreement to allow each network to request tokenized credentials from the other when consumers are transacting across any digital medium — in app, online and in store. Tokens Get Turbocharged.

Part of this is because these agencies are not used to managing multiple payment types, said Linda Jun , senior policy counsel for consumer financial advocacy group Americans for Financial Reform. We need to push the government to do more to reach those places where neither of those is an option.”. The Digital And Paper-Based Balance.

The PYMNTS Merchants Guide To Navigating Global Payments Regulations, done in collaboration with Ekata , examines rapidly changing developments in digital payments at a time when cybercrime — and identity scams particularly — are going hard on legitimate businesses. especially when it comes to enabling seamless payment experiences.”.

In today’s global economy in 2024, the financial transactions has evolved into a dynamic ecosystem, where a multitude of players work together to facilitate fast and secure payment processing. The payment processing ecosystem is vast and multifaceted, with a staggering array of statistics underscoring its significance.

Payments are changing so rapidly that they can sometimes be hard to keep up, and that certainly holds true for QSRs. discussed the emergingpayments coming to the QSR world, and what’s on tap for the coming year and new decade. You can get rid of the loyalty card. If you are already a member, we link you with a new pass.

Customers are shopping online more often and are more frequently opting for contactless payment methods in stores, for example. They are also seeking out merchants that can swiftly and seamlessly offer them the payments and shopping experiences they crave. Sephora: The Key To Omnichannel Commerce Is Options, Options, Options.

These digital marketplaces can only do this work if the payments experiences they offer are also compelling and convenient to teachers and students, however. This is likely to result in high demand for receiving funds quickly and conveniently via person-to-person (P2P) payment apps.

When Mastercard launched Send in 2015, the focus was on making it easy to move money quickly between businesses and people using the debit card as the proxy. Send doesn’t just work with Mastercard branded cards, either, Jess Turner, executive vice president of digital payments at Mastercard, told PYMNTS in a recent conversation.

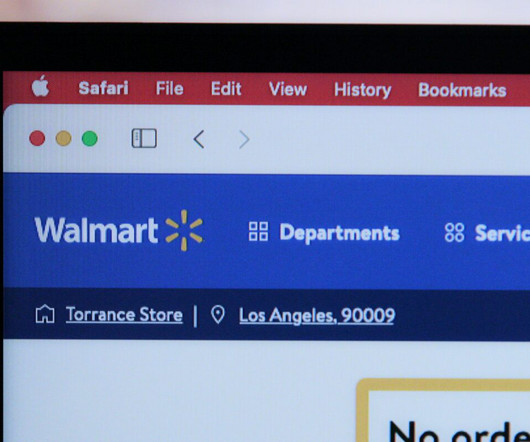

Walmart is partnering with Fiserv to enable pay-by-bank payments for online purchases starting in 2025. Benefits to Walmart include lower transaction costs, faster settlement, reduced fraud, and fewer payment declines, while customers can avoid stacked pending transactions. FedNow and RTP, they don’t necessarily talk to one another.

A new year has begun, but the pandemic continues to throw financial and operational curveballs at banks, businesses and their consumers regarding how they conduct daily tasks or routine payments. This includes shifts in which consumers are shopping and paying, and in the payment tools or methods they are using to finalize their transactions.

Corporate payments innovation has cast a wide net to tackle the many pain points businesses experience today, with accounts payable (AP) one of the most popular targets for disruptors. But supplier payments are far from the only scenario in which businesses face friction when initiating a transaction. From Gig Workers to Rebates.

The only way to predict what the emergingpayments trends are for today is to seek out the one group of people who has the power to control the entire market: consumers. The study looked at 500 consumers (18+) in each country who had at least a credit or debit card. “The pie for card issuers in Europe is significant.

In regions where open banking and other electronic payments pilots are becoming common, such as the Middle East-North Africa (MENA) region, pandemic-era payments are all about privacy, security and trust, particularly in B2B transactions. Privacy Protection In The Spotlight. under the GDPR. under the GDPR.

From the wearables hype to the in-car payments fad, the past few years have seen many payment methods rise and many fall. The success of any specific payment method is strongly affected by macroeconomic factors, consumers’ perceptions, and technology. Take debit cards.

For airlines and hotels, catering to customers from around the world means dealing with a long list of complications, including accepting payments in a host of local currencies, complying with national and international regulations, and finding ways to afford or offset the high price of processing fees.

It was in a convergence of these trends that Visa launched its real-time payments solution, Visa Direct , a technology enabling pushpayments onto recipients’ Visa cards. After all, if there aren’t users to accept payment, then payment senders will have no incentive to use the tech.

In my last post I wrote about the fraud and financial crime problems the USA is likely to encounter as real-time payments increase in both value and volume. In countries such as the UK, real-time payment schemes have been ubiquitous for many years. Don’t forget inbound payments. What Banks Can Do. Customer communications.

Insurance, much like the banking industry, routinely handles some of the largest and most sensitive payments. Both industries are also caught up in similar innovation cycles as they seek to enhance these payments, with each attempting to upgrade legacy systems to keep up with today’s global digital economy. It represented $1.6

And pointing to separate data from Legal Trends, Clio said 50 percent of legal services clients say they are more likely to hire a lawyer if they accept electronic payments — and 40 percent say they wouldn’t hire a lawyer who didn’t accept credit or debit cards. The Power of Data. ” APIs’ Opportunity.

Making B2B Payments Rails Hot. Why ride the existing rails when the B2B payments equivalent of the Hyperloop can make the trip more modern, faster and cooler, even if it costs more and only connects a few places? Rather than rip and replace, they’d like to use software to modernize the payments experience over those rails.

When we started Modo, we had a consumer-facing app that allowed people to combine their loyalty points, coupons, offers, discounts and credit cards at the point of sale. When we started Modo, we had a consumer-facing app that allowed people to combine their loyalty points, coupons, offers, discounts and credit cards at the point of sale.

As a result, European merchants have started offering five payment methods at checkout on average, although many are looking to increase this, according to new research by Aion Bank , the subscription-based, digital bank, in partnership with Vodeno , the API-based, cloud-native platform. They want a holiday or a pair of jeans, or a house.

Consumer behaviour survey: Introduction In May 2025, The Payments Association conducted a follow-up consumer survey to build on its ongoing analysis of evolving payment behaviours in the UK. This year’s data offers fresh insights into how different demographic factors correlate with the payment preferences of UK consumers.

Having spent the better part of the last 10 years managing healthcare payments, both through health plans and third-party administrators, the weakest link, Jinks said, is getting consumers on board. The New York Times wrote in April 2017 that the U.S. The disease: medication nonadherence. But getting there is harder than it should be.

And, across hundreds of blogs and opinions pieces, a single consensus emerged: QR codes’ best use is to amuse with their misuse. The consumer-presented QR code mobile payment use case allows customers to display a QR code on their mobile devices that can then be scanned by a merchant optical scanner to read the code.

New research compiled by Aion Bank and Vodeno released today, highlights that Europe’s top 50 retailers and marketplaces are prioritising new payment options to give customers greater choice at the checkout. The data also reveals the emergingpayment options not yet widely offered.

People would be pretty miserable if they couldn’t borrow money when they need it, for buying a house, a car or covering an emergency. Credit and debit cards came in fourth (11 percent) — we’ll see below that their concern isn’t the fees but just being able to get credit. Fraud and deception are all too common. It is time for a reset.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content