This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If youre a software provider looking to boost revenue, streamline operations, and deliver more value to your users, ISV integratedpayments can be a game-changer. Embedding payments directly into your platform can unlock tremendous benefits both for you and your users. The best part?

No longer is open banking solely for consolidating financial information into a single platform for one enduser. Integrated into its ERP solution, the new feature links electronic banking fees to corporate card spend, allowing for automated receipt creation. ClearBank Dives Into Multicurrency Accounts Via API.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. Eli Shoshani Eli Shoshani is Head of APAC at Bottomline , a leader in global business payments with extensive expertise in the region.

Offline settlements with a digital pound: Lessons from the BoE’s report 16 June 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? A Bank of England experiment proving that offline payments with a digital pound are technically feasible, but complex. Why is it important? What’s next?

From an acronym known mostly by programmers in the early 2000s to something thousands of innovators have embraced to ignite numerous innovative solutions, it’s been an electric journey for the application program interface (API). The API hype cycle has all but ignored what it takes to useAPIs,” David Koch noted.

Swift drives global interoperability and innovation, aligning with the UK’s National Payments Vision to enhance seamless, secure payments. The UKs payments landscape is at an inflexion point.

With open banking technologies making their way beyond the world of consumer finance and into the business banking market, new usecases are emerging from the legislation that opens up bank account data and offers FinTechs opportunities for new functionalities via deeper data integrations. Emerging UseCases.

Companies that fail to integrate financial services into their ecosystems risk falling behind. Embedded consumer payments have already proven the transformative power of embedded finance, streamlining transactions, boosting conversions, and fueling revenue growth. This isn’t a peripheral add-on; it’s the future of commerce.

marked its third anniversary of adopting its open banking framework, making it the leading market to drive the concept of unlocking customers’ bank account data for integration with third-party solution providers. The partnership, which will see the bank adopting its B2B payments platform to finance trade of its corporate customers.

Increasingly, consumer and corporate endusers of various platforms are seeking a more seamless experience, and the owners of those platforms are finding a big opportunity to integrate a range of financial products and services, from payments to financing. But across usecases, Bloh said two key themes are emerging.

In the journey to improve the payments experience, sometimes the best user experience (UX) is an unnoticeable one. Key to achieving this goal is data integration, yet in markets where open banking frameworks aren't as advanced as jurisdictions like the U.K., A Better Payments Experience. Making Payments Invisible.

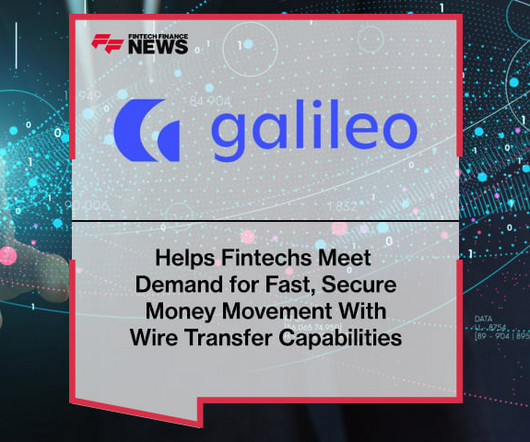

Through its wire transfer API, Galileo connects fintechs partnering with Community Federal Savings Bank (“CFSB”) with Fedwire via sponsor bank CFSB. This service is in high demand for businesses and consumers that need immediate and secure transactions, for example, large transactions such as a home sale, tuition payments or vendor payments.

Visa introduced a platform on Monday morning (April 22), complete with beta application programming interfaces (APIs), that will allow issuers and issuer processors to build and test new products. The initial beta APIs on offer will help those within the Visa ecosystem to create digital cards on demand and add digital services.

Small businesses and corporate end-users have emerged as powerful drivers of exploring new use-cases for open banking and PSD2 regulations. Connecting Accounting to Payments. But it’s not the only use-case for open banking.

FinTech still exists as a fragmented market, where businesses striving to offer payment services to endusers pick and choose among providers, integrate with those providers, and must often navigate across complex technological and regulatory hurdles as they expand into new markets. The Transition In Payments, Too.

As these ecosystems evolve, ISV partnerships have become essential for companies looking to scale, reach new markets, and offer integrated ISV solutions. AWS, Microsoft, Salesforce) to integrate, co-market, and grow together. AWS, Microsoft, Salesforce) to integrate, co-market, and grow together. What is an ISV Partner?

Fast forward to today, and technology has helped play a role in helping Coinstar embrace new offerings and usecases, spanning paper vouchers for cash, or eGift cards for Amazon and Starbucks, among others; and in terms of mechanics, Gaherity said, in the case of eGift cards it is the product partner, not the end-user, who pays the fee.

ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. ISV software products are tailored to meet the specific needs of industries and users. Customer Support In-house support teams maintain direct relationships with end-users for assistance.

It may be an open road for open banking as, three years after the rollout of the second Payment Services Directive (PSD2), bank-FinTech collaborations and new initiatives unlocking bank account data continue to flourish. But it may not always be smooth sailing ahead. ThinCats Links Up With Open Banking FinTech Salt Edge. In the U.K.,

SaaS services are also used in customer relationship management (CRM), human resources management, analytics, and communication. In this article, we’ll explore the many benefits of SaaS and how to implement SaaS payments. Because of their many benefits, businesses have realized the need for implementing SaaS payments as well.

That means financial functions beyond banking are taking advantage of application programming interface (API) data integrations, with productivity gains particularly large for business end-users of these products and services. Unlocking Data, Unlocking Opportunities.

Banks face a new challenge in the open banking age: How do they best use application program interfaces (APIs) to collaborate with FinTech firms and deliver new services to clients? The API economy offers traditional banks several opportunities for innovation. An API-Based Plan For The Future.

The adoption of multiple platforms is giving rise to so-called "app fatigue," and the challenge of integrating these technologies with each other is not always easily overcome. Data integration is foundational to achieving an optimal level of automation in any workflow in the enterprise. Surmounting The Data Hurdle.

Open APIs – to do all they are meant to do, they need open arms. One way to do that is to be open to open APIs. That choice is enabled with open APIs, which, of course, are publicly available to developers and allow applications to interact. Data Point One: 47 Percent. Data Point Two: 726 Billion.

The Fall Member Meeting will bring together FPC members for two days filled with presentations on the most pressing issues in faster payments, panel discussions with industry experts, roundtables on timely topics, and engaging networking opportunities. Foundry Ballroom) Payment networks need volume to scale and keep costs low.

It’s another story in the financial services community, of course, where banks and FinTech firms have accelerated their embrace of the application program interface (API) to open up data and unlock new product development opportunities for endusers — from individual consumers to multinational corporates.

As merchants look to accept payments with ease, and as software developers seek to diversify their revenue-earning strategies, the PayFac model has risen to the forefront. For businesses that choose to become payment facilitators, the benefits are tremendous. What is the PayFac Model? These technologies are often third-party solutions.

Despite an abundance of performance data, many firms still lack visibility into what really matters: how systems function at the point of use. Without insight into the end-user experience, problems often go undetected until they escalate into serious disruption. It expresses the views and opinions of the author.

Competitive forces in the payments and financial services sector have driven two key trends in the U.S.: the acceleration of payments, and the adoption of open banking frameworks. Both are key to addressing the modern demands of end-users. Looping Into Faster Payments.

By leveraging payment monetization and user experience best practices, the payment facilitator model offers a versatile approach to revenue growth — one that benefits businesses of all kinds. This strategy entails tapping into the lucrative payment market and earning a portion of payment processing fees.

Mangopay , a modular and flexible payment infrastructure provider for platforms, today announces the launch of its new Fraud Prevention solution. Platforms can connect to the solution through the Mangopay product ecosystem, meaning they can easily protect themselves against fraud without any additional integration.

FIs, in turn, must also protect the security and integrity of that data, all while giving consumers a sense of control over how and where it’s being used. I see different aggregators [that] have different strengths in different usecases,” he told Webster — thus, there will be room for several players.

It’s a delicate balance; in some ways, FinTech firms and banks are competing, but many FinTech firms rely on bank account data to provide the level of service that endusers have come to expect. Ocrolus deploys a solution with integrated machine learning and proprietary algorithms to address OCR’s shortcomings.

But open banking itself is enduring an evolution, too, as finserv players explore new usecases for data interconnectivity. based FinTech enabling SMBs to integrate their back office platforms with each other via API. Expanding UseCases. While in the U.K., However, we see this as just the beginning.”.

It’s not hard to understand why the medium, small and micro-business owners of Canada would appreciate Interac e-Transfer , which enables them to send or receive funds instantly, directly from or to their bank account, as well as request payments from customers — minus the awkward face-to-face element of asking someone for money.

Payments are arguably the face of fintech. When you think about financial technology, it is easy to think about solutions which are making payments faster, easier and more accessible. We take a retrospective look and investigate which payment technologies have shaped the industry into its current iteration.

The B2B payments market is already enjoying a solid year, thanks to some of the biggest names in payments and FinTech taking a solid stance in the space. PYMNTS takes a look back at some of the most popular B2B payments stories of the year so far. Mastercard , too, has been making deeper inroads in the commercial payments space.

For those diving into the deep end of automation, this can feel like treading water in a storm. And don’t get me started on bulk data transfers – unless you've got the patience and skill to master the art of reading and replicating API documentation for each app in your Zap, you might find yourself in a bit of a pickle.

The new generation has quickly become obsessed with payments personalisation. While personalisation has firmly established itself as a mainstream feature in Europe and the US, it still has considerable room for growth in emerging markets. Simply put, it was unstructured and could not be used by an upcoming fintech or bank.

At the upcoming FinDEVr , 60 leading fintech companies will present their developer-friendly APIs, SDKs, and other solutions to an audience of financial builders and their technical colleagues. Why it’s a must-see: It has nearly 120 APIs that will power the next generation of digital wealth management applications.

MNO authentication is offered through GlobalGateway, the electronic verification platform, which is in turn tied to 200 data sources across credit bureaus, government agencies and financial firms, accessed via API. Think of the phone as a token. After all,” he told PYMNTS, “the internet is not regional.”

Payments regulation roadmap: Q2 2025 14 April 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is the roadmap about? It provides a structured view of the regulatory developments set to shape the payments sector from Q2 2025 onwardsacross the UK, EU, and international markets. Why is it important?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content