This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Faster Payments Council (FPC), in collaboration with Volante Technologies , today released results from the 2025 Faster Payments Barometer, the latest in its series of comprehensive studies analyzing the adoption, trends, and perceptions surrounding faster payments in the U.S.

No longer is open banking solely for consolidating financial information into a single platform for one enduser. Enterprise resource planning (ERP) technology provider Acumatica is embracing bank connectivity with the launch of its newest offering, Acumatica Advanced Expense Management and Electronic Bank Feeds.

Each ID-Pal Once profile is built from already-verified identity data, but critically, this information is re-validated against an organisation’s own risk rules, without requiring the enduser to repeat the submission process. This ensures ongoing compliance while minimising user friction.

” The app will use Mastercard’s virtual card and tokenisation technology – replacing a cardholder’s sensitive data with a unique card number. Businesses can now use virtual cards for point-of-sale transactions using mobile phones. This additional feature has generated new usecases.”

With open banking technologies making their way beyond the world of consumer finance and into the business banking market, new usecases are emerging from the legislation that opens up bank account data and offers FinTechs opportunities for new functionalities via deeper data integrations. Emerging UseCases.

Andrew Doukanaris Ambassador, The Payments Association While vIBANs have positive usecases, challenges exist in limited monitoring of the enduser, alignment with the PSPs risk appetite, and the lack of a consistent framework to mitigate financial crime and regulatory risks. Previous slide Next slide What are vIBANs?

Ledford explored some of those emerging usecases and offered insight into what's next for the RTP network that could add even more opportunities for financial institutions (FIs) and businesses to extract value from real-time payments. Today's Most Valuable UseCases. But certain trends are emerging.

Furthermore, more than 90% of CEOs consider leveraging new technologies a necessary part of driving efficiency and creating new revenue streams, aligning with modern businesses’ need to differentiate themselves in a crowded market. What is often overlooked is that embedded finance is not a playfield only for tech companies.

Galileo Financial Technologies , a leading financial technology company owned by SoFi Technologies, Inc. ” Enabling wire capabilities benefit endusers in several ways: Fast Transactions: Recipients receive their funds on the same day they’re sent.

Danny Russell Head of digital currency technology, Bank of England “The report on the experiment clearly highlights the challenges of supporting offline CBDC payments. To ensure success, the government must set robust standards around anti-fraud technology and prioritise efforts to raise financial and digital literacy.

. “As familiarity and understanding of NFC continues to grow, so too does demand for additional applications and usecases for the technology. NFC technology enables the creation of efficient, reliable, secure, environmentally-friendly, and smart solutions,” adds Mike McCamon, executive director of the NFC Forum.

While AI remains the hottest topic in fintech, it seems as though every single firm in the sector is currently experimenting with how they can make strides in development using the emerging technology. The technology will help automate data entry, reconciliation and financial reporting, freeing up time for strategic priorities.

He pointed to one Zoop client, Brazilian food delivery startup iFood , which recently used Zoop technology to introduce its own debit card product for restaurants on its marketplace. "No But for non-financial companies to provide a positive finance experience to end-users, making payments seamless is key.

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. ISO 20022’s path to ubiquity could serve as a model for faster payments technologies’ own adoption journeys. What Faster Payments Hasn’t Solved … Yet.

And while the concept initially set its sights on elevating the consumer banking experience, the data integration drive continues to expand into new usecases, including business banking, that open up opportunity through bank-FinTech collaboration and data integration. HashCash Brings Blockchain Tech To Unnamed Bank.

Ricky now serves as Managing Director for South Asia at TBCASoft, a global fintech driving next-generation cross-border NFC and QR person-to-merchant (P2M) payments using blockchain-based technology. What practical usecases and insights emerged from the ASEAN-5 implementation phase of Project Nexus?

WiBioCard has built a portfolio of different smart card products targeting large enterprises globally, integrating Fingerprints biometric technology. The products support secure authentication and verification, access and health care usecases.

Integrating Swift with the upgraded FPS would enable a unique reference to be embedded within each transaction, delivering end-to-end tracking across both cross-border (Swift) and domestic payment flows. Looking ahead: a new frontier for cross-border payments Payments are fundamental to achieving economic growth.

Those opportunities would likely not have been possible without the technology, or certainly wouldn’t function as efficiently. The API hype cycle has all but ignored what it takes to use APIs,” David Koch noted. That’s because people get too focused on the technology part of APIs, the “what,” according to Koch. Two To Tango.

The app will use Mastercard’s virtual card and tokenization technology – whereby a cardholder’s sensitive data is replaced by a unique card number so sensitive account details are not exposed to offer enhanced data security and spend control features, all accessible via a simple, easy to use interface.

What this ecosystem evolution means is the payments technology is ready to support global merchants’ needs to facilitate payments for consumers regardless of their location. So the user is still paying with cash,” said Kanovich, “but the whole experience changes. Traditionally, it takes 48 hours to confirm a cash payment to a merchant.

As technology evolves, payment capabilities become more deeply embedded to the point where they are practically invisible to the enduser. This concept works already in specific usecases such as Uber, but many companies envision a hands-free payment experience for all of retail.

This includes account funding and a variety of payment usecases in the United States via the Mastercard network. “We are committed to empower banks and credit unions with innovative technologies that enable them to serve at the center of their relationships with accountholders.” million endusers.

Increasingly, those value-added services are not only focusing on speed of payment, but also enhancing the data that end-users can access about their transactions, with new solutions from Bank of America and Scotiabank some of the latest to bring real-time rails to corporates. Visa Talks Payment Rail Innovation.

There were several opportunities for us to catch up with industry leaders throughout the event, to understand the overlap between the traditional financial services sector and this fast-expanding world of crypto. The key to Web3 development focuses on providing a user-friendly interface and experience for decentralised applications.

Small businesses and corporate end-users have emerged as powerful drivers of exploring new use-cases for open banking and PSD2 regulations. But it’s not the only use-case for open banking. “People were not believing in open banking so much as a big evolution. Connecting Accounting to Payments.

It’s been several months, if not years, since blockchain was the darling of tech startup investors, but this week proved the technology still has a lot to offer venture capitalists. The company plans to use the funding to ready its software for enterprise adoption and explore additional verticals into which it can expand. ClearMetal.

Essentially, he noted, providers can come to the platform to build out the end-user experiences they desire. New UseCases. Through the functionalities embedded in the APIs , Shrauger said, new usecases can take shape through which consumers can manage a range of financial activities, far-reaching in nature.

The Financial Stability Board this month issued a warning for financial institutions (FIs) that outsource key technologies and functions, warning of " systemic risk " associated with too much reliance on a third-party partner.

As the FPC looks to add even more value, Carl’s experience and judgment will be invaluable in assessing the growing need for coordination and standardization to streamline the adoption of faster payments across various usecases.”

In an interview with Karen Webster, Nils Mattisson , CEO of Minut , a startup that makes a home security device that does not rely on cameras and is connected to the Internet of Things, said advanced technologies can make sure homes are safe, in real time.

In a recent conversation with PYMNTS, Michael Brackpool, head of product at bunq , emphasized the role that flexibility plays in being able to address endusers’ needs. “We think of the user experience as critical and want to apply this philosophy on the business side.” The Back-End Strategy: Flexibility.

Part of that collaborative movement involves working with open source technology, where, generally speaking, software is made (freely and publicly) available for users to develop and modify as they see fit. There’s particular interest in using real-time payments for peer-to-peer transactions, he added. Making Old ATMs New(ish).

ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. ISV software products are tailored to meet the specific needs of industries and users. Customer Support In-house support teams maintain direct relationships with end-users for assistance.

Speakers: Elizabeth McQuerry, Glenbrook Partners; Mike Sklow, Goldman Sachs; Samson Rajan; JP Morgan; Miriam Sheril, Form3 1:30pm-2:10pmCT: Panel Session – Business End-Users Mega UseCases (City Beautiful Ballroom AB) As more capabilities become available for faster payments, business endusers are finding creative ways to use the services.

One of the latest adopters of Mastercard's Track solution is Transcard , which announced its A2A capabilities wielding Mastercard technology. The technology is designed to combat fraud for both businesses and customers as an overlay service that operates on top of a range of existing rails. Rapyd Combats Fraud Across Payment Rails.

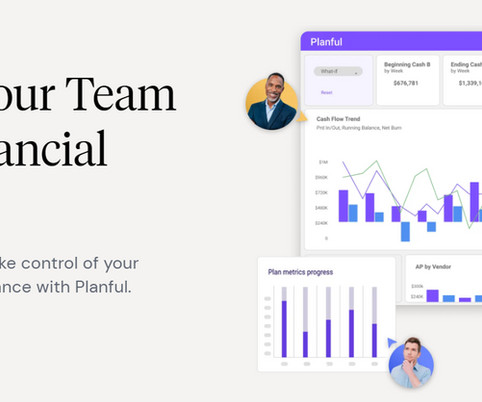

AI Integrations At Planful, their vision lies in delivering a complete, off-the-shelf AI solution for structured and dynamic planning usecases. One Size Does Not Fit All – Generic AI technology solutions often fail to meet the specific needs of finance. The application's speed sometimes lagged, especially around year-end.

The study provides a renewed understanding of consumer adoption, familiarity, and experience with NFC technology at both a global and regional level, with 55% of respondents saying they would prefer to use their smartphone or smartwatch to make a payment rather than their card. 53% confirmed they do so multiple times each week.

According to McCarthy, this is one of the biggest areas of technological innovation in today’s cross-border B2B payments space, as players look to develop the groundwork of improved global payments infrastructure by taking an ecosystem approach to disruption. Accelerating Ecosystem Innovation. So how do you accelerate that?”

Through NACHA’s Countdown to Same Day ACH podcast series, we’ve explored what Same Day ACH is all about, the myriad of usecases and applications it’s designed to deliver and if corporations and businesses are truly ready for the change. banks and credit unions the ability to better serve their customers. Where The Blockchain Fits.

The adoption of multiple platforms is giving rise to so-called "app fatigue," and the challenge of integrating these technologies with each other is not always easily overcome. Once an enterprise has overcome the data hurdle, the process of building custom apps and automated workflows can be applied to a variety of usecases.

Join the Payments-Led Growth Movement Sign up to keep up-to-date with the latest trends in payments, vertical SaaS, and technology from industry experts. Understanding ISV Integrated Payments Integrated payments let users pay for goods or services directly within your softwareno third-party redirects or handoffs. Learn more.

You can see how valuable this feature can be–you gain access to new features and capabilities, all without disrupting your experience as an end-user. It’s the culmination of two trends: Endusers looking for the convenience of accessing financial tools inside their favorite daily apps and software.

Fast forward to today, and technology has helped play a role in helping Coinstar embrace new offerings and usecases, spanning paper vouchers for cash, or eGift cards for Amazon and Starbucks, among others; and in terms of mechanics, Gaherity said, in the case of eGift cards it is the product partner, not the end-user, who pays the fee.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content