This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Speaking on behalf of DPI , Adefolarin Ogunsanya praised the company for its “combination of innovative technology, fast growth, and positive impact on the continent.” In the years since then, Moniepoint has grown into an all-in-one financial ecosystem that serves 10 million businesses and individuals.

The future of payments is digital, inclusive, and transformativedriving financial access, innovation, and global economic empowerment. The global financial landscape is undergoing a profound transformation. trillion business opportunity by 2025. trillion business opportunity by 2025.

The processes included converting reserve account balances into digital Rupiah and vice versa, ensuring seamless interoperability with Bank Indonesias Real-Time Gross Settlement (BI-RTGS) system. Addressing interoperability, scalability, and security challenges, Indonesia sets a global example for nations exploring similar initiatives.

Over 350 million adults in Africa live on a cash-only basis ( [link] ), without access to financial accounts, credit cards, or lending facilities. Digital currency systems could prove to be key in improving financialinclusion and opening up new opportunities to large underbanked communities in many African countries.

The report highlights key milestones, insights, and the organizations transition into an independent foundation, further strengthening its ability to drive financialinclusion across the continent. Key achievements included: Expanding access to IIPS in Cabo Verde, Mauritania, Rwanda, South Sudan, and the CEMAC region.

Payments innovation in Indonesia holds significant promise for contributing to the nation’s economy and helping bring about a more inclusive, accessible, and equitable financial system. The total number of QRIS users stood at 43.44 million, BI also reported.

In doing so, they risk missing the core innovation that digital money promises: the ability to transfer value directly, securely, and potentially without the need for intermediaries. By leaning heavily on custodial models and surveillance-driven frameworks, many central banks are limiting the utility and inclusiveness of CBDCs.

The fintech, which serves as an industry utility with over 30 years of experience, spearheads the creation of innovative digital platforms that support the integration of open banking and finance, crucial for modernising the financial ecosystem.

Fraud involving faster payments is a growing challenge that requires vigilance and innovation, said Lee Kyriacou, Chair of the FPC Fraud Work Group. stakeholders to adopt innovative approaches that protect consumers, businesses, and financial institutions. Collaboration and innovation are essential in combating fraud.

With a strong focus on financialinclusion, Fuse aims to bridge the gap between traditional and decentralized finance, empowering small businesses and emerging markets. Fuse is committed to driving financialinclusion and creating a decentralized future where everyone has the tools and opportunities to succeed.

Designed for speed, interoperability, and user-friendliness, UPI has become the backbone of India’s payment ecosystem. Its key advantages include instant transactions, interoperability across banks and payment apps, low-cost processing, and enhanced security features.

This solution demonstrates our commitment to help our Business Banking and NEO BIZ clients improve their cashflows through innovative banking solutions. Rajeev Chalisgaonkar, Head of Business Banking and NEO BIZ at Mashreq, said: “We are proud to be the first bank in UAE to offer Aani Instant Payments to SMEs.

These experts covered some of the industry’s hottest trends and most urging issues, including artificial intelligence (AI), quantum computing, digital assets, next-generation transactions, and financialinclusion. However, challenges remain, particularly regarding interoperability.

SEAs young, tech-savvy population, a growing consumer base, reliance on informal financial systems, and supportive government initiatives aimed at financialinclusion serve as robust drivers for long-term growth. This demand is expected to fuel fintech innovations even in the face of current economic hurdles.

Championed by the Central Bank of Somalia (CBS), the initiative marks a major step in modernising Somalia’s payment infrastructure, promoting financialinclusion and enhancing economic stability. This innovation brings speed and security to daily transactions, empowering businesses and individuals to embrace a cashless economy.

This proactive approach, driven by the Monetary Authority of Singapore (MAS), seeks to enhance the nation’s financial infrastructure. The goal is to attract investment and innovation, maintain Singapore’s competitive edge in the global arena, and expand financialinclusion.

From digital payments to decentralised finance (DeFi), these companies are solving real-world challenges like financialinclusion and cross-border transactions, while setting new global standards for innovation. Atome Financial specialises in consumer financing, ADVANCE.AI bolttech Valuation: $2.1

Blockchain and a bank charter might do much to boost financialinclusion. He stated that the Figure Pay account will be interoperable with other accounts and payment methods (bypassing some of the vagaries of “closed” systems like MCX, now long-defunct). And herein lies the great irony in financial services.

In its new manifesto, ‘ Creating the Conditions to Support Growth and Innovation in Payments ‘, The Payments Association describes the 66 policies recommended by the 216 payments professionals working across financial crime, regulation, open banking, ESG, cross-border payments, digital currencies and financialinclusion.

Open banking is transforming the financial landscape by fostering innovation , competition, and improved customer experiences. It involves sharing financial data through secure application programming interfaces (APIs). This connectivity drives a more dynamic and responsive financial ecosystem.

Championed by the Central Bank of Somalia (CBS), the initiative marks a major step in modernising Somalia’s payment infrastructure, promoting financialinclusion and enhancing economic stability. This innovation brings speed and security to daily transactions, empowering businesses and individuals to embrace a cashless economy.

One of them is that too many people in the world are denied access to banking and financial services of any kind. That this lack of financialinclusion excludes them from participating in most of the payments and commerce activities that most of those reading this take for granted. The second?

Lighthub Asset and WeLab’s venture (the consortium) will improve financialinclusion in Thailand. Its features will be tailored to solopreneurs and micro, small and medium enterprises (MSMEs) facing unstable income and limited financial access. This starts with access to credit and advanced-AI planning tools.

Looking ahead, the Monetary Authority of Singapore (MAS) has introduced the SGQR+, an innovative concept aimed at revamping Singapore’s QR payments infrastructure for the future. Building upon SGQR, SGQR+ represents the next generation of interoperable payments for merchants.,

The Manifesto , Creating the Conditions to support Growth and Innovation in Payments, describes the 66 policies recommended by the 216 payments professionals working across financial crime, regulation, open banking, ESG, cross-border payments, digital currencies and financialinclusion.

KNET utilized ACI’s Digital Central Infrastructure solution to build the central payment infrastructure of WAMD, an interoperable, countrywide scheme that enables account-to-account (A2A) payment transfers via a bank’s mobile app or internet banking service by using a phone number. billion of additional global GDP growth.

These awards highlight companies and individuals whose fintech initiatives have contributed to advancing financial technology, promoting financialinclusion, and improving service delivery. Napier AI designs and engineers technological innovation to make a measurable difference in driving down financial crime.

As charging infrastructure expands, EFT Corporation is pioneering payment innovation in South Africas electric vehicle (EV) charging space by implementing a cloud-based, open-loop payment system for EV charging stations. The country now has nearly 400 public charging stations, with further expansion planned for 2025.

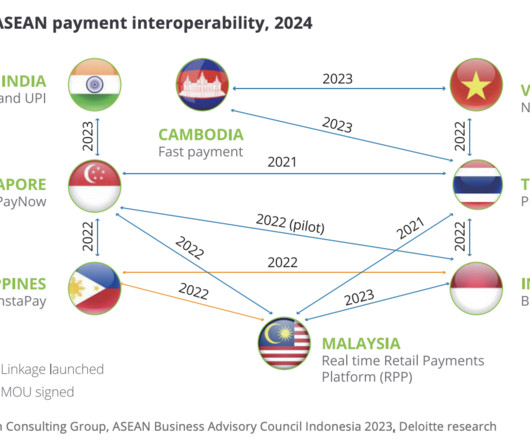

Their growing popularity has spurred continuous financialinnovation, such as the rise of buy now, pay later (BNPL). In the region, several countries have introduced cross-border QR code payment linkage, creating a unique interoperable ecosystem within ASEAN.

What does the financial services ecosystem look like in Uzbekistan? What is the level of interest in fintech innovation there? Hughes: The financial services sector is still largely dominated by major state banks, which command around 70% of the market. Are any of these major areas of innovation in Uzbekistan’s fintech scene?

With digital wallets growing in sophistication, consumers and businesses have fundamentally altered how they interact with payments, forcing banks and payment system providers (PSPs) to innovate. The decline in cash usage has also helped speed up the adoption of digital wallets. Regulatory challenges Regulators are in a race against time.

Open finance is transforming financial services by enabling broader data-sharing, fostering competition, and driving innovation in payments and financial products. Europe is driving regulatory-first frameworks, while Asia is spearheading market-led innovation. What’s next? Regional approaches are diverging.

This strategic partnership aims to empower Trinidad and Tobago to establish a reliable and efficient real-time payments platform for both person-to-person (P2P) and person-to-merchant (P2M) transactions, expanding digital payments in the country and fostering financialinclusion.

It addresses how evolving regulations shape the digital asset landscape, influencing innovation, compliance, and global competitiveness. PSPs must adapt by enhancing compliance, leveraging new frameworks for innovation, and collaborating to shape practical regulatory solutions. This could slow innovation and hike costs.

Expanded financial connectivity, empowering millions of customers to transact internationally with ease. Greater financialinclusion , enabling businesses and individuals to participate more effectively in the global digital economy. Together, we are driving a new era of digital payments.”

With in-depth data covering global market penetration, transaction values, and consumer preferences, the insights presented here will empower decision-makers to refine their strategies, enhance operational efficiency, and capitalise on the growing demand for innovative payment solutions.

The Payments Association , the most influential community in payments, has today launched The Payments Manifesto 2025: creating conditions to support growth and innovation in payments. Include strategic change programmes aligned with key priorities, including independent oversight, regulatory effectiveness, innovation, and risk management.

Gaining Traction: Empowering the Unbanked In regions with significant unbanked populations, Decentralised Finance (DeFi) platforms are offering accessible financial services through the innovative use of blockchain technology. Interoperability with traditional financial systems presents another significant hurdle.

Committed to open competition and interoperability, we’re truly ecosystem agnostic, with a strong track record of working with global leading brands like Apple, Tesla, Allianz and CK Hutchison.”

Expanded financial connectivity, empowering millions of customers to transact internationally with ease. Greater financialinclusion, enabling businesses and individuals to participate more effectively in the global digital economy. Together, we are driving a new era of digital payments.”

With the UK government continuing to support the UK’s broader fintech environment and promote open banking innovation, Open Banking in a Box will champion the UK’s world-leading open banking standards and make the case for greater cross-border interoperability that will benefit UK PLC and support financialinclusion globally.

Network inaccessibility keeps a large section of the population out of the ambit of digital payments and is a challenge to financialinclusion. This is a key step in accelerating financialinclusion and digital penetration among the masses. Fortunately, there’s a light at the end of this tunnel!

In APAC, financialinclusion has emerged as a driving force behind digital innovation. Many nations within the region have recognised the transformative potential of extending financial services to underserved populations. The absence of proper documentation and financial education presents significant hurdles.

SC Ventures, the innovation, fintech investment, and ventures arm of Standard Chartered, and Giesecke+Devrient (G+D) successfully completed a proof-of-concept (PoC) on the Universal Digital Payments Network (UDPN). Meanwhile, the the direct model is where central banks manage wallets and settlements within a centralised CBDC system.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content