This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Tokenisation is now a core enabler of secure, interoperable digital paymentspowering embedded finance, asset tokenisation, and evolving identity flows. Once a system for masking sensitive data, tokenisation has evolved into a foundational technology for enabling secure, interoperable, and scalable digital payments.

Legacy systems are increasingly unreliable, expensive to maintain, and resistant to modern payment innovations. Integration headaches: Open Banking, APIs, and AI-driven automation often require costly, unreliable workarounds. But as the financial landscape evolves, that mindset is in danger of proving very costly.

As more firms look to enter the blockchain and decentralised space, easy integrations and the ability to develop applications are an absolute must. Ensuring this is possible on the XRP Ledger (XRPL), Ripple , the crypto solutions provider, has partnered with Axelar Foundation , the nonprofit decentralised interoperability network.

Swift drives global interoperability and innovation, aligning with the UK’s National Payments Vision to enhance seamless, secure payments. The UKs payments landscape is at an inflexion point.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. Eli Shoshani Eli Shoshani is Head of APAC at Bottomline , a leader in global business payments with extensive expertise in the region.

Unifying global fiat and stablecoin payments, stablecoin payments infrastructure provider BVNK has announced a new embedded wallet. They have existed in today’s market for some time but have had limited capabilities to manage stablecoin, crypto and fiat payments in one place. Embedded wallets are not a novelty.

Our goal was clear: overcome the fragmentation that plagued international merchants, who had to maintain different payment solutions for each country, leading to operational complexity and significant costs.

The payments outlook 2025: Strategic priorities from industry leaders May 2 2025 by Payments Intelligence LinkedIn Email X WhatsApp Whats the article about? The strategic priorities for the payments industry in 2025, as discussed by senior payments leaders who attended a Payments Labs roundtable.

The creators envision the UK RLN as a unified ‘innovation platform,’ integrating various currency forms like current commercial bank deposits and a shared ledger for tokenized commercial bank deposits. This strategic choice highlights their complementary methods in achieving interoperability as well as seamless integration.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? Open finance is transforming financial services by enabling broader data-sharing, fostering competition, and driving innovation in payments and financial products.

Whether you are a B2B founder building a global marketplace, a CFO steering a SaaS scale-up, or a finance team tasked with managing complex payments, finding the best fintech tools is critical. This guide covers the top 100 fintech tools across key categories including banking APIs, billing, KYC/AML, FX, crypto tools, and open banking.

Rain provides backend infrastructure – APIs, compliance layers and settlement logic – that enables fintechs and wallets to build and launch stablecoin-linked card programs. As demand for real time, global payments grow, Rain is seeing strong momentum from partners looking to issue and use onchain cards and settle in stablecoins.

Today there is no doubt that Georgia has become an integral part of East-West exchanges,” the Prime Minister continued. Within all our projects – which range from central bank digital currencies (CBDCs) to Know-Your Customer (KYC) APIs – we aim to lower entry barriers for new entrants into the ecosystem.

It was a contactless payment on POS using a card issued by Eurasian Bank JSC on the Way4 digital payments software system. Today, just six months later, plastic cards in the Digital Tenge currency are used for both in-store and ecommerce purchases – and are accepted globally through the Mastercard and Visa networks.

Temenos (SIX: TEMN), the banking software company, today announced a collaboration with Visa , a world leader in digital payments, to integrate Visa Direct, a Visa money movement solution, with Temenos Payments Hub and make available to banks via Temenos Exchange, the Temenos ecosystem of partner solutions.

Completing online payments via manual card entry can be time-consuming and off-putting for customers. This article will cover everything you need to know about Click to Pay, including its history, how it works, and how you can implement the payment method in your business. Learn More What is Click to Pay?

The agreement brings together OpenPayd’s API-based payment and banking services with Circle’s infrastructure for USDC, a dollar-denominated stablecoin issued by regulated affiliates of Circle. The primary goal of this partnership is to support cross-border transactions and digital asset operations for enterprise clients.

Visa introduced the Visa+ service in April last year to bridge the gap among various apps in the peer-to-peer (P2P) payments space, allowing for real-time payouts to participating digital wallets. At the time, Visa+ outlined plans to make the service widely available to Venmo and PayPal users in the US by mid-2024.

policymakers have sketched out the first federal framework for payment stablecoins. It classifies payment stablecoin issuers as regulated financial institutions, pulling them firmly under anti-money laundering and consumer protection rules. For the US government, the play here is pretty simple: reaffirm the U.S.

Why Is Middleware Important in the Payments Industry? Types of Middleware What Are APIs and Middleware, and How Do They Differ? UseCases for APIs vs Middleware Key Takeaways Middleware acts as a bridge between applications, platforms, and databases, helping systems communicate and share data.

Finalists in the corporate categories were evaluated based on impact, sustainability, practicality, interoperability, and creativity, while individual submissions were assessed on contributions to the Singapore fintech sector. The company replaces traditional B2B payment methods (e.g. Four finalists were shortlisted in each category.

Numeral , a Mambu company, a leading payment technology provider for financial institutions, today announces the launch of its fully managed Verification of Payee (VOP) solution, empowering financial institutions to comply with the European Unions VOP regulation by the October 9, 2025 deadline.

Shortly after, January 2018 saw the revised Payment Services Directive ( PSD2 ) requiring all banks and financial institutions in the EU to do the same. The moves also hoped to significantly enhance the security of payments, as well as the protection of consumer data.

The Fall Member Meeting will bring together FPC members for two days filled with presentations on the most pressing issues in faster payments, panel discussions with industry experts, roundtables on timely topics, and engaging networking opportunities. Foundry Ballroom) Payment networks need volume to scale and keep costs low.

Bridging the worlds of fiat currencies and blockchain, Visa , the digital payments firm, has launched its new Visa Tokenized Asset Platform (VTAP). We’re excited to leverage our experience with tokenisation to help banks integrate blockchain technologies into their operations.”

Users can log in to the platform using their preferred web browser without purchasing and installing any application. Examples of popular SaaS apps include Shopify, an eCommerce platform, Dropbox, a cloud storage service, and Stax Bill, an automated payment processing system. Such integrations enhance the overall customer experience.

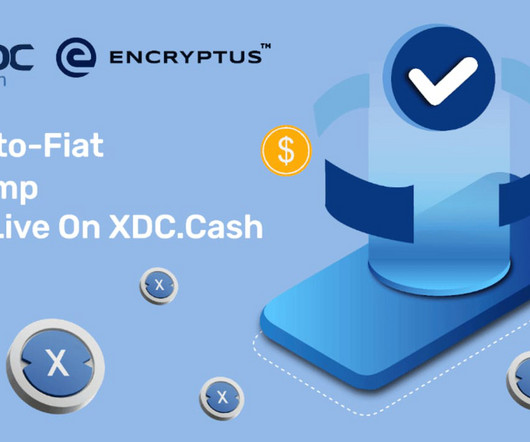

Dubai, UAE, April 10th, 2025, FinanceWire XDC Network continues to strengthen its ecosystem with the launch of XDC.Cash, a Next-Generation Crypto Payment Solution powered by Encryptus. This integration ensures competitive, near-interbank ratesespecially in frontier markets where traditional financial services often fall short.

Managing invoices efficiently is integral for businesses to maintain smooth cash flows and accurate financial records. Some prominent usecases for OCR for invoices include: Retail : Retailers deal with a high volume of invoices from suppliers for products, services, and operational expenses.

Faster payments schemes across the globe are placing new definitions on what it means to be fast, especially as more initiatives heard towards real-time transacting. In the three years since FIS began this annual report, the number of real-time payments programs more than doubled, researchers noted.

It’s not hard to understand why the medium, small and micro-business owners of Canada would appreciate Interac e-Transfer , which enables them to send or receive funds instantly, directly from or to their bank account, as well as request payments from customers — minus the awkward face-to-face element of asking someone for money.

The rise of new technology has dramatically altered the traditional nature of payments, allowing gig workers and full-time workers faster access to their earnings while enabling businesses and banks to move funds more quickly across international borders. Around the Smarter Payments World.

The whole point of startups is to do things differently than mainstream players, and that is exactly what these companies are doing with automation, interoperability and digital currency initiatives. Modo Payments. As payments change states, both systems can follow along, each in its own language. Chargehound.

Apart from the challenges covered above, the main reason that many organisations still handle PDF data extraction manually is that: Conventional PDF data extractors typically extract everything in one go from a PDF and not just the specific data or key value pairs that are important for a particular business usecase.

to use gMobile to authenticate a customer, and it extends across retail or electronic wallet, where a seller may be setting up a loyalty program tied to method of payment. All of this is being done without the use of JavaScript or device ID tags. The usecase dictates how it is used.

This is more conceivable thanks to the proliferation of FHIR (Fast Healthcare Interoperability Resources) technology, which looks to increase interoperability among hospitals, physicians, and other relevant parties. are enabling new machine vision usecases.

At the moment, many banks have limited Open Banking capabilities because they are constrained by their core banking systems, which are often far removed from any API gateways, he says. By contrast, when using Engine, banks can replace their legacy systems and plug APIs directly into their core system.

Payments regulation roadmap: Q2 2025 14 April 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is the roadmap about? It provides a structured view of the regulatory developments set to shape the payments sector from Q2 2025 onwardsacross the UK, EU, and international markets. Why is it important?

Thunes raised $150 million in Series D funding from Apis Partners and Vitruvian Partners. Thunes plans to use the funding to fuel US growth, drive AI innovation, and expand interoperability with the digital asset ecosystem, positioning itself against competitors like Wise and Airwallex.

In this blog we describe what stablecoins are, explore the current state of the stablecoin landscape, focus on key regulatory developments, the adoption by traditional financial institution, the various real-world usecases, the potential and challenges and the various solutions to these challenges. What are stablecoins?

Better real-time payouts in Canada By collaborating with the Canadian pay-by-bank provider, TerraPay’s network of money transfer operations can facilitate improved real-time payments to recipients in Canada.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content