This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Technical Defense Strategies Email authentication forms the foundation of BEC defense. Sandboxing suspicious attachments prevents malware that could enable accounttakeovers. Multi-factor authentication protects against credential compromise but must extend beyond employee accounts.

Key changes could include embedding platform-wide risk analytics, adopting real-time authentication, aligning their fraud strategies along business goals, and embracing transparency through AI. Consequently, the cost of fraud prevention now reaches $4.61 Static, manual-heavy models are no longer viable.

Emphasis on Cybersecurity and Data Privacy Digital lending faces rising threats: data breaches from hacking, fraud via synthetic identities, accounttakeovers exploiting weak security , ransomware disrupting operations, and insider threats. over the forecast period of 2024 to 2032. Protecting sensitive data is paramount.

Shoppers may be quick to take their business elsewhere if these demands are not met, with 66 percent of respondents saying they had at least once given up opening accounts due to poor experiences. Consumers expect their merchants to keep them safe and are likely to defect if retailers cannot fulfill this demand.

If people can accept long lines at the TSA and the occasional sore arm at the Minute Clinic, why can’t they accept an extra layer of authentication when using their credit cards online or the need to update their passwords more frequently? They’re using weak passwords – oftentimes, the same weak password for all of their online accounts.

Users need to complete the authentication process once to enjoy this new top-up method. To ensure user security, YouTrip has implemented safeguards such as top-up limits and restrictions on withdrawals to the registered PayNow account. These measures aim to prevent fraudulent transfers in the event of accounttakeover attempts.

They predict that social engineering attacks will surpass ransomware in 2024 due to increased sophistication, AI tools and emerging techniques, leading organisations to bolster cybersecurity defences with AI, scenario testing and multi-factor authentication. Cybercriminals use that information to impersonate people in positions of authority.

The rise in digital-first, digital-only providers has introduced competition and fundamentally transformed customer expectations.The demand for seamless, secure, and personalised financial experiences is fierce. Orchestrate customer journeys The digital age demands customer journeys that are secure, seamless and intuitive.

Today we hear insights from payments experts, including the adoption of tap-to-pay technology, the role of blockchain and AI in payments, flexible payment terms, security in authentication methods, PSD3 implementation, vertical-specific solutions, and the rise of digital wallets.

It’s a situation demanding action. This new vigilance is the result of rampant cybertheft throughout the pandemic, from brazenly diverting government Paycheck Protection Program loans to the bad businesses of credential theft and accounttakeovers. Quick And Seamless Security. It’s on banks to deter them.

Advanced Features and Capabilities Key features include support for SWIFT, SEPA, and ISO20022 payment formats, device fingerprinting, biometric authentication, real-time monitoring, and AML screening. ComplyTek’s integrated solutions ensure that organizations stay ahead of regulatory demands and financial crime risks.

Those questions also speak to the seemingly impossible tension in the world of payments and new card accounts: how to onboard and authenticate consumers as quickly and seamlessly as possible, while also protecting them and the institution from fraud. (Hint: The criminals know the difference.) Baseline Advantage.

Fraudsters know that higher transaction volumes and a demand for fast processing times leave merchants vulnerable to attacks. Fraudsters know that higher transaction volumes and a demand for fast processing times leave merchants vulnerable to attacks. Behavioral Biometrics Ensure You Are You .

The software was reportedly built using information stolen from the NSA and demanded payment from users, rendering their computers and networks inoperable without a ransom payment. The problems with these authentication methods, McDowell said, is that even the most stringent security systems can be beaten easily if left up to human error.

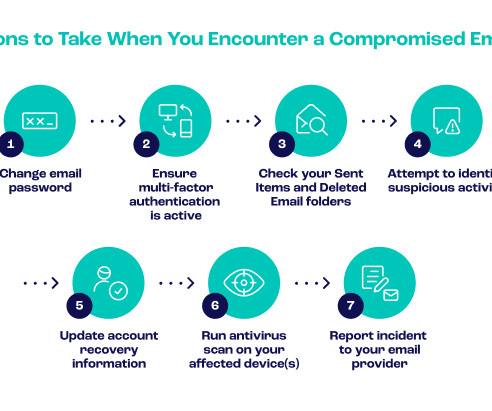

A BEC attack is when a fraudster gains unauthorized access to a business’s account. The most damaging form of BEC is accounttakeover (ATO) attacks. Let’s look at what business email compromise attacks are and explore some of the many ways you can combat them. What Is a Business Email Compromise Attack?

Whether it’s safeguarding sensitive personal and financial information from attacks like WannaCry or authenticating travelers at an airport, security is top of everyone’s mind these days. CLEAR, a security line-busting authentication system, recently received a $15 million investment from asset management firm T.

But the ease and speed that consumers demand when transacting online comes with risk, as merchants need to establish identity — in other words, being certain that customers are who they say they are — in a world where buyers and sellers may be continents apart. PSD2 is here, of course, changing the way consumers and companies access data.

The company prompts first-time site visitors to create accounts before they are able to browse specific items, which enables the eTailer to start learning which kinds of products interest each shopper, Akkineni said. Consumers also demand interesting and convenient shopping. Fighting fraud . Making shopping sticky .

.” The impact of chargeback fraud and other transaction-related fraud — like accounttakeovers or payments fraud — on the bottom line is clear. While Sift initially launched as a chargeback fraud specialist, Lee recently told PYMNTS that market conditions have led customers to broaden their demands.

Here Tom Randklev, global head of product at payment orchestration company CellPoint Digital , explores strategies for airlines to safeguard their revenue and combat fraud amid increasing travel demand. per cent of total global airline revenue – and accounting for 46 per cent of all online fraudulent transactions. per cent.

For the consumer, online shopping has become the norm, but so too has opening accounts digitally; even if you look at financial accounts where many would say there is a higher risk of loss. Remote working doesn’t only impact the organisation in terms of how it authenticates employees. Customer experience.

Boku, through Boku Identity, authenticates consumers using a device that is an intrinsic enabler of the trust: the mobile phone. Instead, we are primarily focused on helping to fix commercial problems that get in the way of doing business — using a cleaner, mobile-first method of authentication.”. Dynamic Vs. Static Authentication .

For consumers, the biggest concerns are falling victim to accounttakeover (26%), and ID theft (26%). Both bank and card providers have moved quickly to implement additional security measures that address fraudulent activity, namely in the form of new authentication methods. The impact on consumers has been twofold. Conclusion.

PSD2 is bringing higher transaction volume for banks, and more demand from consumers for mobile payments and quicker transactions. Criminals are always on the hunt for new opportunity. How exactly fraud attacks and fraud prevention will change in the post-PSD2 world remains unclear, but change is certain, according to observers.

Call centers have been using AI to meet this demand, obtain better customer insights, while strengthening their authentication methods and fraud protection strategies. According to the study, predicted losses due to accounttakeovers at call centers are set to reach $775 million by 2020. Fraud is no small matter.

He recently spoke with PYMNTS about what it takes to keep debit cards and their associated bank accounts safe from cybercriminals. . FIs have long been aware that relying on knowledge-based authentication (KBA) goes only so far. Consumers aged 18 to 22, meanwhile, relied equally on the two methods. . Holistic Security.

Byrnes said there are three primary types of fraud: stolen credit cards, accounttakeover and friendly fraud. Even if they list the tickets on StubHub for 50 percent off, they can still make hundreds of dollars off each ticket for certain in-demand events. Accounttakeover certainly isn’t new , but it is on the rise.

In Asia, these technologies are being adopted by a rapidly growing middle class with increasing disposable income and a rising demand for financial services. Asian consumers are also becoming more aware of the efforts banks are making to protect them against crimes such as identity theft, accounttakeover and card fraud.

As Ritter noted, email accounts are the first avenues of attack for fraudsters. Gaining access to email gives bad actors an entry point for accounttakeovers. They can intercept requests for password changes, effectively freeze legitimate users out of their own accounts, and then drain funds.

Credit card fraud accounted for 34% of these statistics, indicating fraud’s pervasive and industry-agnostic nature. Cybercriminals often employ sophisticated tactics, such as synthetic identities, accounttakeovers (ATOs) and exploiting unsuspecting individuals through socially engineered schemes.

Restaurants cite high costs and lack of demand for not offering first-party ordering, and many make up for this by employing third-party services. percent year over year (YoY), accounting for 18.3 Developments From Around the Mobile Order-Ahead World. Mexican QSR Chipotle is one chain that is seeing dividends from mobile order-ahead.

These malicious scammers are growing in number and refining their strategies, employing ever more sophisticated methods, including accounttakeovers, synthetic identity fraud, and social engineering scams. In the UK alone, fraudsters syphoned off £1.2billion in 2022, with almost 80 per cent of app fraud cases starting online.

It also utilizes a Segment-of-One approach, which entails tracking transactions that occur on the company’s network and using that data to verify the authenticity of consumer identities and their transactions. After its launch in 2011, HiGear, a San Francisco, Calif.–based Then suddenly, it hit a wall.

Fraudsters can spoof numbers and social engineer the call to access sensitive medical records and other personal identifying data that they can use for accounttakeover, identity theft or synthetic identity construction. You need to be ready to receive your customer service requests across all the different channels that they demand.”.

The report found that card ID theft increased, with losses up 53 per cent to £79.1million, as many criminals reverted to stealing ID and falsely applying for new credit cards or accounttakeovers, were they not able to trick someone through APP. Furthermore, of those impacted by unauthorised fraud, 98 per cent were fully refunded.

In an unauthorized push payment fraud scenario, when the fraudster makes the payment; transactions would likely be made from a device not typically used by the legitimate account holder, and the funds would likely go to a strange beneficiary account. Phishing, Smishing, Hypnofraud and More. Push Payment Fraud Is on the Rise.

SESAMm: Raised $55M, analyzes sentiment from online data for finance, growth driven by strong demand in fintech analytics. Autobooks: Raised $98M, small-business accounting software, increasingly integrated by banks, showing strong growth. Fast-forward 17 years, and there have been 320 Best of Show trophies handed out.

Strong customer authentication (SCA), frictionless user experiences, and regulatory oversight were among the focal points as experts dissected the existing risks and potential remedies for open banking fraud. The industry must collaborate on fraud prevention, enhance data sharing, and align regulatory frameworks with innovation.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content