This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This routing allows the processor to request authorization for the transaction from the issuing bank, which then approves or denies it based on factors like available funds and fraud checks. Routing : The payment processor routes the transaction request to the appropriate issuing bank for authorization.

A data breach occurs when cybercriminals infiltrate your systems and access sensitive information without authorization. And painful account recovery procedures await all users who must reset passwords across potentially dozens of breached websites. Conduct audits periodically post-partnership. What Is A Data Breach?

Businesses must proactively assess fraud risks, implement adequate procedures, leverage technology for fraud detection, and foster a culture of compliance to avoid regulatory penalties. Compliance requires proactive fraud risk assessment, the implementation of preventive procedures, and a culture of accountability. What’s next?

Safeguarding customer funds The Financial Conduct Authority (FCA) has proposed significant changes to the safeguarding regime for payments and e-money firms. Regular audits and compliance checks : Firms will face enhanced monitoring and reporting under the proposed policy. Engaging external auditors may provide additional assurance.

Regulatory reviews from the Bank of Italy, UIF, and the European Banking Authority (EBA) have identified key shortcomings in the management of vIBANs. Partnering with regional providers, leveraging AI for fraud detection, and conducting regular audits will ensure compliance, transparency, and operational excellence.

Establish protocols for communicating with external parties, such as law enforcement, in multiple languages: Knowing how to quickly share info with authorities in various countries can speed up response times. Train employees regularly on these policies and procedures Make training available in all relevant languages.

On 25 September 2024, the UK Financial Conduct Authority (FCA) published its long-awaited Consultation Paper (CP24/20) setting out proposed changes to the safeguarding rules applicable to electronic money institutions (EMIs) and payment institutions (PIs) (together, payments firms). What does this mean for Payments firms?

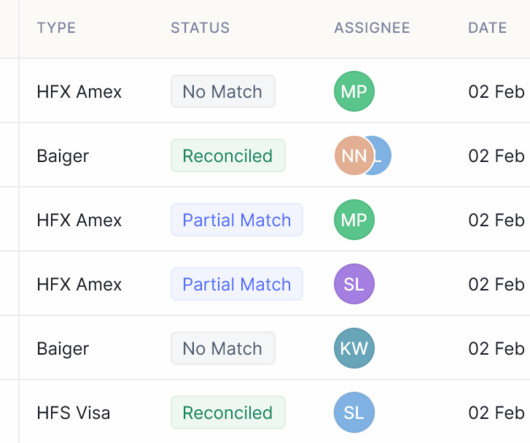

Audit Bank Reconciliation Guide Both internal and external accounting audits are essential parts of financial management as well as organizational risk management. A bank reconciliation audit is one such process that helps in identifying financial gaps or discrepancies. Looking out for a Reconciliation Software?

If not, it may be time to rework your current accounting policies to implement audit trails. Despite what many business owners believe, audit trails aren’t reserved only for companies that receive an audit. Audit trails can prevent fraud, aid in disaster recovery, and ensure compliance with regulatory agencies.

Requirement and Testing Procedures 3.2.a Requirement and Testing Procedures 3.2.a Requirement and Testing Procedures 3.1 Minimize cardholder data storage by implementing policies, procedures, and processes for data retention and disposal. Protect sensitive authentication data before authorization. PCI DSS v3.2.1

The Financial Conduct Authority (FCA) continues its commitment to guiding firms on embedding the Consumer Duty by publishing two insightful reports. Robust processes: Established procedures for report production, involving relevant business areas and governance bodies.

In this blog, we'll delve into what invoice audits entail and why they are crucial for the financial integrity of businesses. What is an Accounts Payable Audit? An Account Payable Audit is a process by which the financial records of the accounts payable department are examined by an auditor.

This follows a 2022 penalty of 70,000 for delayed accounts and after previous attention of the UK’s Financial Conduct Authority in 2019 on AML compliance. How Neopay can help At Neopay, we’re experts at helping regulated businesses build, audit, and enhance their compliance frameworksbefore the regulators come knocking.

A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. It authorizes or declines payments based on available funds and fraud checks. Ideally, you want instant or same-day fund settlement.

So, in a world where regulatory scrutiny is increasing, especially in sectors like finance and healthcare, SaaS companies must align with PCI DSS to meet regulatory requirements to authorize transactions and avoid penalties, fees, or, in severe cases, a ban on processing credit cards by major payment brands (e.g. Visa, MasterCard, etc.)

So, in a world where regulatory scrutiny is increasing, especially in sectors like finance and healthcare, SaaS companies must align with PCI DSS to meet regulatory requirements to authorize transactions and avoid penalties, fees, or, in severe cases, a ban on processing credit cards by major payment brands (e.g. Visa, MasterCard, etc.)

According to Bloomberg , EY is accused of failing to notify authorities when it discovered red flags related to the Danske Bank money laundering case. And KPMG said it “reacted and drew attention to, among other things, procedural failures in connection with the area of money laundering, both to the management and the board.

Establish protocols for communicating with external parties, such as law enforcement, in multiple languages: Knowing how to quickly share info with authorities in various countries can speed up response times. Train employees regularly on these policies and procedures Make training available in all relevant languages.

The requirement mandates that software development procedures must be documented and examined to ensure that all security considerations are integrated into every stage of the development process. It required code changes to be reviewed by others than the author, following secure coding practices. is now 6.2.2. PCI DSS v3.2.1

Banks are expected to apply the follow guidance in connection with their digital asset custodial services: Governance and risk management : Prior to launching digital asset custodial services, banks are expected to undertake a comprehensive risk assessment and to implement appropriate policies and procedures to mitigate identified risks.

TL;DR An anti-money laundering (AML) program is a set of laws and procedures that seek to uncover attempts to disguise illicit money as legitimate. An anti-money laundering (AML) program is a set of laws and procedures that seek to uncover attempts to disguise illicit money as legitimate. Let’s get started.

A 2024 joint survey by the Bank of England (BoE) and the Financial Conduct Authority (FCA) found that 72% of UK-regulated firms are actively using or piloting AI and machine learning toolsan increase from 67% in 2022. Assign ownership, implement approval processes, and establish escalation procedures.

The Bank of England, Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) have already completed much of the work on operational resilience guidelines. This should include policies, procedures, protocols, and tools needed to protect your organisation’s assets.

Financial controls are the procedures, policies, and means by which an organization monitors and manages its revenues, costs, budgets, cash flow, and other financial aspects. Setting up regular financial audits Regular financial audits are essential for ensuring that the financial controls in place are working as intended.

Safeguarding of client funds continues to be a high priority for the Financial Conduct Authority (FCA) in the payments and e-money markets. This includes proposals on firms’ systems and controls and improving FCA oversight through improved reporting and independent audit of firms safeguarding arrangements.

Role-based access and user authentication: A Sage 100 integration enhances security by enabling role-based access controls for payment data, ensuring only authorized users can process transactions or view sensitive information. These measures help detect suspicious activity, prevent unauthorized transactions, and reduce chargeback risks.

Effective safeguarding training covers the policies, procedures, and regulations that must be adhered to in order to minimise risks and maintain compliance with regulatory standards. Detailed records of all safeguarding training should be maintained for audit purposes.

Specific Requirement - New: Rules for limited shared account use (duration, documentation, approval, auditability). Changes Core Focus Limiting database access to programmatic methods (apps, stored procedures) and database administrators. Apps access data in line with their user roles (authorization levels). a (v3.2.1) -> 8.2.2.a

The Financial Conduct Authority’s (FCA) proposed reforms to strengthen consumer fund safeguarding in the payments and e-money sectors. Firms must prepare for these changes by improving their internal processes, conducting audits, and adapting to new compliance requirements to ensure seamless implementation of the FCA’s reforms.

About the Author: Katie Thomas, CPA, is a content creator, 2021 & 2022 40 under 40 CPA Practice Advisor recipient, Top 50 Women in Accounting recipient, and the owner of Leaders Online, where they help accounting professionals increase their impact, influence, and income through thought leadership and digital marketing.

Following the Financial Conduct Authoritys (FCA) 2020 visit, the FCA imposed a Voluntary Requirement (VREQ) to restrict new high-risk customer onboarding while CBPL remediated its controls. MillionAML The Financial Conduct Authority fined Metro Bank 16.7 July 2024: CB Payments Limited (Coinbase UK)3.5 November: Metro Bank16.6

They are designed to ensure that purchases made by the organization are authorized, appropriate, and comply with relevant policies and regulations. The main objectives of purchases controls include: Authorization and Approval: Purchases controls ensure that all purchases are properly authorized by authorized personnel within the organization.

As a result of the alert, the FBI offered up advice for banks, including: implementing “separation of duties or dual authentication procedures for account balance, or withdrawal increases above” a certain amount; putting in place application white-listing to block malware from being executed; monitoring, auditing and limiting “administrator and business (..)

This article will explore the essential aspects of staying compliant with NACHA rules, such as risk management, data security, authorization protocols, and more, to help institutions maintain the highest standards of operational integrity and customer trust. What is NACHA?

Medical data may be transferred to healthcare authorities and government bodies when necessary. This widely accepted set of policies and procedures is designed to enhance the security of credit, debit, and cash card transactions, while also protecting cardholders from the misuse of their personal information.

The recent £29 million fine imposed on Starling Bank by the Financial Conduct Authority (FCA) for financial crime failings offers important lessons for businesses in the e-money and payments industry. Key takeaway : If your business deals with high-risk clients, it’s crucial to implement enhanced due diligence procedures.

Remember that internal controls are procedures and processes management emplace to ensure accounting integrity and financial transparency. In this case, the referee (actual control measures and checks) uses the playbook (company procedures built on accepted accounting principles) to manage the game (financial reporting).

This process has to be audit-proof. The intergovernmental agreements (IGAs) for FATCA consider a FATCA compliance check through the IRS – the audit trail is important to avoid getting the recalcitrant status. In several countries, the Competent Authority requires additional information within the report.

The Financial Conduct Authority (FCA) has issued important updates to its Financial Crime Guide, following a public consultation on proposed changes. Audit Support : Neopay provides independent audits of your financial crime systems, giving you peace of mind that your controls are robust and meet regulatory standards.

The Financial Conduct Authority (FCA) has issued two significant “Dear CEO” letters, marking the implementation of the new requirements for reimbursing victims of Authorised Push Payment (APP) fraud. This includes both the technical aspects, such as transaction monitoring, and the human elements, such as staff training and procedural reviews.

The researchers examined executive pay as a risk factor because auditing standards include executive compensation in their risk assessment and prior research. Twelve percent of companies analyzed had at least one C-level executive with prior audit experience , either as a partner or manager of a public accounting firm.

Applicable to large organisations, the offence imposes criminal liability if firms do not have adequate fraud prevention procedures in place, even if senior leadership is unaware of the misconduct. Non-compliance could lead to regulatory enforcement by national authorities, as well as reputational harm and potential exclusion from EU markets.

Compliance policies and procedures: Develop comprehensive compliance policies and procedures that address key regulatory requirements, such as anti-money laundering (AML) and Know Your Customer (KYC) obligations (see below). Staff training: Provide regular training to your staff on AML obligations, red flags, and reporting procedures.

Follow these tips to stick to federal regulations: Refer to federal regulations when drafting internal policies and procedures. Subscribe to regulatory updates or newsletters from relevant federal authorities, such as the PCI Security Standards Council (more on this later). Security audits. End-to-end encryption.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content