This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The UK’s Financial Conduct Authority (FCA) has begun a public consultation on proposed plans to either significantly increase or remove altogether the current 100 (US$129.83) limit on contactless card transactions. The FCA has set out its thinking in an engagement paper on contactless payment limits.

The Monetary Authority of Singapore (MAS) and the Infocomm Media Development Authority (IMDA) will implement the Shared Responsibility Framework (SRF) for phishing scams on 16 December 2024. FIs have a six-month transition period to comply with this new duty before it becomes enforceable under the SRF.

Following discussions over the past year, the Monetary Authority of Singapore (MAS) , together with NETS Group and participating banks, is set to launch stand-in capabilities for NETS point-of-sale terminals. The feature will allow payments to go through, up to a transactionlimit, during service disruptions.

By Tom Groenfeldt Follow Author Share Save Comment Innovation Enterprise Tech Real-Time Payments Are Soaring In The U.S. Follow Author Jul 17, 2025, 03:08pm EDT Share Save Comment Close up of network data flowing on black background. By Tom Groenfeldt , Contributor. Forbes contributors publish independent expert analyses and insights.

Regulatory reviews from the Bank of Italy, UIF, and the European Banking Authority (EBA) have identified key shortcomings in the management of vIBANs. Currently, large enterprises are the primary users, while small businesses and consumers have shown limited adoptionlikely due to unclear policies on customer eligibility and risk exposure.

Legal issue/risk Next steps/action required Legal issue/risk: The FCA has the authority to take regulatory action, issue fines, or impose constraints on firms that breach impact tolerances or fail critical resilience testing. Stress test resilience against 24/7 availability standards.

Home Announcements Payments Ujjivan Small Finance Bank introduces international RuPay select debit card External This content is provided by an external author without editing by Finextra. It expresses the views and opinions of the author. It expresses the views and opinions of the author.

Deputy Prime Minister and Chairman of the Monetary Authority of Singapore (MAS) Gan Kim Yong addressed the safety of digital banking services for minors under 16 in a written parliamentary reply. Such accounts aim to instill financial management skills in children while providing a controlled environment.

The European Banking Authority (EBA) has issued a statement urging the European payments industry to increase contactless transactionlimits to EUR 50 (USD 54.97).

Deputy Prime Minister and Minister for Trade and Industry Gan Kim Yong has reiterated the Monetary Authority of Singapore’s (MAS) ongoing efforts to combat cross-border payments scams. Key among these measures are a default transaction notification threshold of S$100 or lower and a daily transactionlimit of no more than S$1,000.

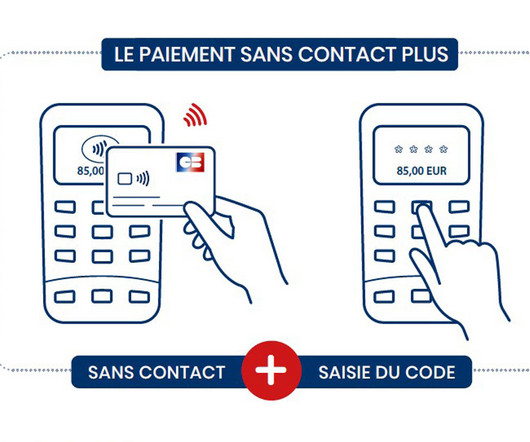

To use the service, the merchant enters the transaction amount in the usual way and the customer then taps their contactless card to the merchant’s payment terminal. To use the service, the merchant enters the transaction amount in the usual way and the customer then taps their contactless card to the merchant’s payment terminal.

The document goes on to show that “overall, our between-card analysis suggests a strong causal effect of the increased tap-and-go limit on the use but only a small effect on first-time adoption of contactless payments.” “Card schemes and card-issuing banks set rules for cashless payments between consumers and merchants.

Just last year, the Monetary Authority of Singapore (MAS) has released a proposal for a Shared Responsibility Framework (SRF) which focused on a defined scope of phishing scams. Authorities emphasise that legitimate banks, including DBS, have ceased the practice of sending clickable links via SMS or email to retail customers since early 2022.

Fighting Scams and Authorized Push Payment Fraud in the US. US regulators seem poised to update the status quo for bank liability for authorized user/authorized push payment fraud, but just how big is the potential? In multiple geographies around the world, there has been a strong focus on authorized push payment fraud.

The purpose of a PIN is to authenticate the identity of the cardholder during a transaction. In a payment scenario, the PIN helps confirm that the person using the card is authorized to do so. It protects you from unauthorized transactions that could lead to chargebacks or losses.

Criminals use real-time payment schemes to commit fraud for direct financial gain or to facilitate other crime: Authorized Push Payment Fraud. It has been named ‘authorized’ because the legitimate account holder is initiating the payment. Account Takeover Fraud.

Financial institutions can integrate Ondot’s app or API into existing services to “give consumers increased control over and visibility into their personal payment transactions.”. More Mobile Management. What does that main for the daily life of a consumer?

Global ACH is available but only for bank-to-bank networks Wire transfers have no geographic limitations. You must have the employees’ bank routing numbers, account numbers, and authorization to set up payroll via ACH transfer. Customers can also authorize ACH payments to your business accounts for goods and services provided.

The UPI Circle enables a primary UPI user to delegate transactionauthority to a trusted secondary user. Full Delegation This mode allows the primary user to assign a monthly transactionlimit of up to 15,000 to the secondary user. It enables the secondary user to transact freely within the set boundaries.

Rising frustration over online payment transactionlimits , security and data privacy have begun to crop up now that consumers and merchants are settling into the new normal, showcasing just how rapidly the banking world is changing. The problem has a simple fix, however, and regulators are able to respond with some ease.

Personal and business identification documents verify your authority to open an account on behalf of the business and confirm your business type and structure. Access to business-specific services: Many business accounts offer merchant services for processing credit card payments, invoicing tools, and integrations with accounting software.

With traditional payment methods, there are waits between when transactions are authorized and when funds are finally disbursed. Other industry recommendations include tightening authentication methods and transaction monitoring, as well as studying incoming and outgoing payments to detect unusual activities.

They encrypt card information, as well as authorize or decline a transaction. . Transfer – Your customer’s card information and transaction details are securely transferred to the acquiring bank’s merchant account. This will make it possible for your customers to use their debit and credit cards safely.

The methodologies that underpin transaction risk analysis for cards can be deployed for other payment types, with the speed and volumes needed to assess real-time payments. Authorized push payment fraud relies on customers making a payment without stopping to think. Customer communications. Mutual authentication.

Thus far, commercial payments have lagged behind P2P transactions, finding traction across use cases such as replacing cash on delivery (and where Mastercard has just introduced Pay on Delivery ), making insurance payouts to consumers or paying wages to employees and gig workers.

“A Smart Nation means people and businesses are empowered through increased access to data, more participatory through the contribution of innovative ideas and solutions, and a more anticipatory government that utilizes technology to better serve citizens’ needs,” the Infocomm Development Authority of Singapore (IDA) explained. or higher.

Here’s how EFTs work: Initiation: A party starts the EFT process by providing the necessary bank account information and authorizing funds transfer. Processing: The information then goes through a secure network, such as the ACH network, where transactions are batched and processed.

14, 2016, any bank that issues a Visa-branded card must give cardholders the option to register for alerts related to any card and card-not-present transactions, international cross-border transactions, and transaction amounts that an authorized cardholder has specified based on some transactionallimit.

This also includes small ticket transactions. Nearly seven out of ten UPI transactions are valued under Rs 500. Owing to this pattern, the Reserve Bank of India (RBI) issued a framework enhancing transactionlimits for small-value digital payments in offline mode.

TransactionAuthorization: The processor communicates with the player’s bank or payment provider to verify and approve the transaction. Real-Time Confirmation: Once authorized, the payment gateway finalizes the transaction, instantly updating the player and allowing them to continue gaming without delays.

Approval Processes : Establish who authorizes expenses and the workflow for approval. This could vary by role, department, or type of expense. It's about creating boundaries within which employees can operate autonomously. This helps in maintaining a checks and balances system.

Singaporean authorities have issued a warning about a surge in scams where individuals impersonate staff from Shopee, UnionPay, and the Monetary Authority of Singapore ( MAS ). They recommend using the ScamShield app to block scam calls and messages, setting transactionlimits, and activating the Money Lock feature in bank accounts.

Payment Controls – located within the DBS/POSB digibank app – allows customers to self-manage their card transactionlimits in real-time. Customers can use these controls to protect themselves from unauthorised transactions when their card is misplaced, stolen or misused.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content