This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

LSEG Risk Intelligence has launched its Global Account Verification (GAV) service in Asia-Pacific and Europe, the Middle East, and Africa, expanding efforts to enhance security in cross-border payments. This helps businesses confirm supplier and customer payments and detect potential fraud risks.

Evolving money laundering risks for EMIs: Insights from the upcoming NRA 18 July 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The UK 2025 National Risk Assessment’s decision to reclassify e-money institutions (EMIs) as high risk for money laundering and terrorist financing.

European financial institutions face rising fraud, regulatory pressure, and compliance fatigue—modernisation is now essential for resilience and risk reduction. What’s clear is that this isn’t just an issue of administrative burden, but rather one of risk exposure. It’s a business risk. These losses aren’t just line items.

The platform risk paradox: Managing digital commerce fraud at scale 12 June 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? How digital commerce platforms manage escalating fraud risks while scaling operations. Why is it important? Consumer fraud losses reached $12.5

Diversify across industries to spread risk and stabilize income, balancing high-risk and low-risk clients for a robust mix. Embrace technology and data analytics to enhance service offerings, streamline processes, and improve risk management.

Carrington Labs, a Sydney-based provider of customised cash flow underwriting models and credit risk analytics, has formed a partnership with Taktile, a New York-based decision platform, to assist consumer and SME lenders in refining their credit risk strategies. That’s why I’m excited about our partnership with Carrington Labs.

As the Financial Conduct Authority (FCA) prepares to take over full responsibility for regulating UK payments, new research from Equals Money reveals that combating fraud and tackling widespread delays are top priorities for higher-risk players in the industry. ” says Campbell. ” says Campbell.

AI risk classification platform EverC revealed today that it is joining forces with G2 Risk Solutions (G2RS). Moving forward, the two will leverage EverC’s AI capabilities and bring G2RS’s risk and compliance capabilities to the payments risk ecosystem.

Checkout.com , a leading global digital payments provider, today announced an extension to its partnership with the Merchant Risk Council (MRC), reinforcing a shared commitment to helping its members navigate the growing complexities of digital fraud and payment risk.

Many application teams leave embedded analytics to languish until something—an unhappy customer, plummeting revenue, a spike in customer churn—demands change. But by then, it may be too late. In this White Paper, Logi Analytics has identified 5 tell-tale signs your project is moving from “nice to have” to “needed yesterday.".

While the solution removes the need for cards, payment terminals, and outdated checkout flows, it needs support to ensure there is an adequate risk management process in place, as well as end-to-end onboarding: cue iDenfy. We needed a compliance partner that could scale with us while maintaining user trust.

EBANX also says that network tokenisation stands out as another prime example, as it replaces sensitive card data with encrypted identifiers for each transaction, reducing fraud risk without compromising approval rates. The technology lowers fraud-related declines and enhances the overall quality of transactions.

The latest updates deliver capabilities far beyond those of the legacy system, creating new opportunities to revolutionise services, reduce risk, expand market reach, and drive innovation. These position the UK payments sector for continued evolution in a rapidly changing global financial landscape.

As we saw during the kickoff to the holiday shopping season, Visa continues to thwart more attempts at fraud from these bad actors, continuing our mission to be the safest way to pay and be paid for everyone, everywhere. said Paul Fabara, Chief Risk and Client Services Officer at Visa. And thats paying off.

The dual impact of generative AI on payment security, highlighting its potential to enhance fraud detection while posing significant data privacy risks. Firms must adopt transparent AI practices, enhance regulatory frameworks, and continuously train models to navigate the evolving landscape of AI-driven threats. Why is it important?

The investment will help AKUVO expand its cloud-native collections and credit risk solutions, enhancing efficiency and customer experience for banks, credit unions, and fintechs. Digital collections and credit risk platform AKUVO landed a new round of funding today. .

In practical terms, this means there are fewer PCI requirements you need to comply with within your self-administered systems, reducing cost and risk. Both offer enhanced security for storing and utilizing payment data, reducing overall fraud and risk levels. They can be validated and identified without risking exploitation.

The Most Widespread Payment Frauds in Singapore Singapores consumers are relatively more aware of fraud risks compared to other regions, leading fraudsters to refine their methods. Phishing continues to be one of the most prevalent scams affecting both consumers and businesses. Below are the most common types of fraud found now.

Banks clinging to outdated systems risk security breaches, regulatory headaches, and lost market sharemodernisation isnt just an upgrade, its a survival strategy. For years, banks have been reluctant to modernise their legacy infrastructure, believing that change outweighs the risks of staying put.

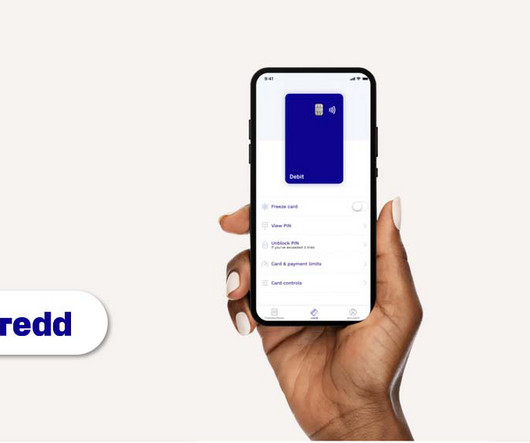

Patricia Haynes joins as Senior Vice President of Platform, bringing her expertise in technology operations and risk management from roles at Zopa and LexisNexis Risk Solutions. This move is part of Thredd ‘s efforts to strengthen its platform, products, and regional support for fintech firms and programme managers worldwide.

While these reports are typically regulatory in nature, the 2025 edition reads like a warning bell for the fintech industry — especially for firms that are growing fast but neglecting the governance and risk controls needed to stay compliant. 🚧 Key Findings: A System Under Pressure 1. . 🚧 Key Findings: A System Under Pressure 1.

SMEs that modernise payments can unlock growth, improve cash flow and build trust—while those that delay risk revenue loss and reputational damage. Underpinning front-end innovations is the relentless need for security and efficiency that continues to drive new technologies at the back-end. It’s a business continuity problem.

MAS is working with banks and payment service providers to strengthen anti-scam measures, as scams involving self-initiated transfers continue to make up the largest share of reported losses. MAS is also working with banks to strengthen user authentication for higher-risk online transactions.

The shift driven by fintechs could erode banks’ dominance, forcing them to modernise or risk losing a significant share of the market. While banks still hold the majority of merchant relationships and dominate acquiring market share in most regions, they face an existential risk. This growth is expected to continue until 2028.

This upgrade aligns American payment processing with international standards, enabling greater efficiency, richer payment data, and more robust risk and fraud mitigation. trillion in daily transactions and is seen as a catalyst for continued innovation in the U.S. The migration supports over $4.7 payments landscape.

His expertise and vision will be invaluable as we continue to scale our platform and support financial institutions globally in modernizing their payments infrastructure. He will work closely with partners, banks, and corporations to deliver innovative, risk-managed solutions that meet the demands of the fast-evolving payments landscape.

It expects threat actors to continue to use advancements in AI technology to enhance financial scams, making scams more challenging for victims to identify and likely resulting in an uptick in financial losses. However, the overall number of individual ransomware and data breach incidents tracked by Visa PFD decreased by 12.3%

It is committed to driving inclusive growth through open collaboration and continuous innovation. Antom continues to strengthen its payment processing capabilities across all payment channels. Antom continues to launch tech-driven innovative solutions to provide more secure and efficient services at lower cost to its customers.

Payment leaders must focus on fraud prevention, collaboration with tech and telecom sectors, and public education to mitigate future risks. In the world of digital payments, fraud is an ever-present threat that continues to evolve, creating serious risks for both businesses and consumers.

The service continues to provide automated matching, netting, and programmable atomic PvP settlement through Baton’s distributed ledger technology, which has processed more than US$13 trillion in FX settlements to date.

As global regulations are growing more complex, staying alert and accurate has become a necessary multifaceted strategy that combines sophisticated technical design, intelligent risk scoring, and compliance automation to overcome the difficulties in network partner and wallet integration, laying the groundwork for long-term, scalable growth.

This enhanced service is designed to upgrade payment security, reduce the risk of fraud, and ensure the accuracy of transactions. CoP offers increased payment security, reduced risk of fraud, and enhanced accuracy by allowing users to verify the payee’s details before completing a transfer.

Traditional, rules-based anti-money laundering (AML) systems are increasingly seen as outdated and insufficient for detecting hidden threats, exposing institutions to regulatory, financial, and reputational risks.

Australias financial intelligence agency AUSTRAC has introduced new restrictions on crypto ATM operators and refused to renew the registration of one crypto ATM provider, Harros Empires, citing ongoing risks of criminal exploitation. The agency said it will continue to monitor the sector and adjust regulatory measures as needed.

An automated alert in the core banking system can notify the treasury team of any shortfall in real time, reducing operational risk. A risk review reveals that the bank’s credit rating has dropped. Assess & document operational risk impact of using insurance/guarantee. No expansion of eligible assets has been made.

Smart routing and optimisation: Advanced POPs leverage machine learning and real-time analytics to route transactions intelligently, considering cost efficiency, transaction success rates, geographic proximity, and risk scoring. These tokens are useless if intercepted, significantly mitigating the risk of data breaches.

As the digital economy continues to grow, so does the need for quick, seamless, and secure payments. And the risks are real. Custom systems to match specific risks Fraud isnt a one-size-fits-all issue. The risks an online retailer faces arent the same as those for a FinTech platform.

Paving the way for safer and quicker payments for everyone, this vision also unlocks a new era for physical cards by making the possibility of numberless physical cards the default, further reducing the risk of fraud should a card be lost or stolen. Additionally, the risk of fraud is minimized.

A 12-hour cooling-off period is required for the activation of digital security tokens and new device logins to e-wallets, reducing the risk of unauthorized access. This inclusion acknowledges the increased risk of significant losses from e-wallets and mandates robust consumer protection controls.

Patricia previously served as VP of Technology Operations and Delivery at Zopa, where she led risk management and process improvements, and Senior Director of Software Engineering at LexisNexis Risk Solutions, spearheading AML and compliance technology initiatives.

This mitigates the risks often associated with frontier markets. Manpreet continued: “Many global businesses have hesitated to enter emerging and frontier markets like Pakistan due to regulatory challenges, cross-border payment complexities, and unfamiliar payment preferences.

Table of Contents Voices from the industry: Insights into the 2024 payments landscape In 2024, we witnessed a convergence between consumer and B2B payments, driven by the rise of BNPL adoption, AI-powered fraud detection, and the continued digitalisation of payment platforms.

While vIBANs offer innovation in payment systems, they introduce risks like money laundering due to insufficient oversight. Payment Service Providers must strengthen due diligence, monitoring, and collaboration with regulators to address these risks. Including structured data would help PSPs monitor and mitigate financial crime risks.

Apart from keeping complex payment structures running, interchange fees compensate issuing banks for taking on cardholder credit risk, and help card companies fund rewards programs. Covers risk taken on by issuing banks Issuing banks take on financial risks while extending credit to cardholders. Even for low-risk cards (e.g.,

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content