This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Singapore authorities and banks are ramping up efforts to tackle a growing scam where fraudsters steal card details through phishing and trick victims into providing an OTP. This allows scammers to fraudulently provision stolen card credentials onto their mobile wallets for unauthorised contactless transactions.

In recent years, businesses have seen this massive shift from desktop to mobile devices which has forced them to develop apps with built-in integrated payment gateways. But when it comes to payments, mobile apps have to contend with a few unique challenges. Why Would Companies or Developers Want a Mobile App Payment Gateway?

This shift is especially visible in the adoption of network tokenisationa model introduced by major card networks like Visa and Mastercard, where card details are replaced with dynamic, network-managed tokens. In short, payment credentials are being redefined, with tokens moving to the forefront of secure, seamless transactions.

This market includes a range of services and technologies that facilitate the acceptance, authorization, and settlement of payments across various channels, including online, in-store, and mobile. They require secure systems like point-of-sale (POS) terminals , online checkout gateways, or mobile payment solutions to process payments.

We examine both quantitative gains— such as higher customer satisfaction scores, rising self-service usage and digital adoption rates—and qualitative developments, including more personalized services, smarter virtual assistants and greater accessibility in digital banking. IDC estimates the banking industry will invest about $31.3

Your provider may ask you to download a package and run an installer or set up onlinecredentials, so following their instructions is essential. Common options include credit and debit cards (Visa, Mastercard, American Express, etc.) and ACH/eChecks for direct bank transfers. Digital wallets (Apple Pay, PayPal, etc.)

In a mutual commitment to accelerating the adoption of an open digital wallet, global card networks Mastercard and Visa announce their agreement to allow each network to request tokenized credentials from the other when consumers are transacting across any digital medium — in app, online and in store.

Those processors will in turn work with issuing banks to offer near-instant issuance of cards. The end result: Cardholders gain the ability to make online and in-app purchases – and at the point of sale, through digital wallets – almost immediately after issuer approval. Omnichannel – and Even Plastic, Too.

Dubai First , the consumer services platform under First Abu Dhabi Bank (FAB), has become the first issuer in the region to leverage Mastercard Token Connect to push customers’ tokenized card details from its mobile app to Click to Pay and digital wallets.

Mastercard announced today (Oct. 24) a host of new strategic partnerships to bring online payments capabilities to digital wallets users in the U.S. The agreements will allow Mastercard cardholders to use the mobile wallets to shop online at the hundreds of thousands of merchants around the world where Masterpass is accepted.

So much of our industry is tied to Visa and Mastercard to support consumer payments. While I don’t blame Visa or Mastercard for putting controls in place, as they also suffer from supporting our industry. An answer to our pain has been developing over the past few years through paying with bank payments or transactions.

We can hail a ride from a mobile app, and our transactions for all sorts of goods and services can be easily paid for from our phones. There are a wide variety of digital payment types, such as mobile POS systems, contactless payments, and digital wallets. All you need to use a digital wallet is a smartphone.

Payments giant Mastercard has launched its new ‘Open Banking for Account Opening’ programme for select US debit and prepaid products, hoping to streamline and secure account opening. In a recent study, Insider Intelligence found that Gen Z mobilebanking adoption continues to rise by 12.4 million by 2026.

Today Mastercard announced the Open Banking for Account Opening program, providing a foundational set of open banking products as a core benefit to Mastercard consumer and small business debit issuers as well as consumer prepaid issuers in the U.S. year over year, from 20.7 million in 2020 to hit 47.8 million by 2026.

But while merchants have now had more than a year to adjust to the new technology, retailers still lag behind when it comes to chip card adoption, causing frustration and confusion for consumers, even with chip-based cards decreasing counterfeit fraud by 60 percent, according to Mastercard. Mobile security on the move.

Mastercard has announced the integration of Deposit Switch and Bill Pay Switch with Mastercard’s Open Banking platform, enabling consumers to automatically switch their direct deposits and update their recurring bill payments, both when opening a digital account or when updating information on an existing account.

Mobile payments using biometrics to authenticate the user is forecasted to reach close to $2 billion in 2017, up from $600 million last year, according to new data from Juniper Research. What’s more, 90 percent said they think they would use biometrics for online payments in the future because they see it as a more secure method.

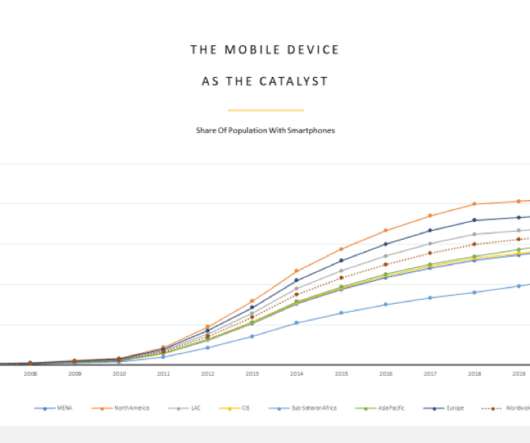

The launch of the iPhone in 2007 and the App Store in 2008 opened everyone’s eyes to the impact that mobile would have on payments and commerce. Twenty years and hundreds of millions of smartphones later, the digital payments experience is anything but consistent anywhere — online, in-store and in-app.

Yesterday, PYMNTS detailed what happened during Day 1 of Mobile World Congress in Barcelona. It also detailed a series of news announcements from MasterCard, including details about its “selfie pay” expansion plan, MasterPass expansion plans, MasterCard’s IQ Series, its partnership with Coin, and its wearable payments play.

To hasten that adoption, In two recent examples, Mastercard said earlier this week that it is piloting a new service with PNC Bank called Payment on Delivery (which replaces, and should not be confused with, cash on demand, or COD). What we’re doing with Bill Pay exchange is vastly improving onlinebank bill payments,” he told Webster.

It's an ecosystem where half of online commerce now happens. All accessed through Amazon’s digital and mobile front door. They enable payments at online merchants and via mobile apps, but are now increasingly part of a larger shopping, savings and spending ecosystem.

Jumio : A global provider of online identity verification, Jumio uses AI and biometrics to verify users by checking documents and live selfies. AVSecure : A blockchain-based age verification tool, AVSecure links a user’s verified identity to payment credentials, ensuring they meet age requirements. Users link their Verify.Me

Traditional banking products, including checking, credit, and savings accounts, are under threat from a new crop of digital-first startups. Many of these startups are launching products without a bank charter and targeting a very specific customer base. DOWNLOAD THE 61-PAGE consumer banking REPORT. savings accounts.

Taken as a group, the platform companies show that consumers are increasingly comfortable coming online to get what they need, that ad targeting is working, and that the companies that are pivoting online to reach consumers where they are — namely, on mobile devices and tablets — are embracing new ways to monetize that contact.

It is not a surprise that consumers today are making more online payments than ever before. Interestingly enough, research by PWC found that the number of consumers making mobile purchases increased from 7% to 17% from 2010-2017. Plus, it allows revenue to quickly and easily hit your business bank account. Mobile Payments.

According to a joint release by both firms, the two will teaming up to offer shoppers a faster payment option for customers shopping online. “We Merchants and Acceptance, Mastercard. With the integration, BJ’s members can pay for items in their virtual cart without having to take out a card or input their credit credentials.

The latest news on mobile payments shows that the big banks are wanting in on the mobile wallet race, but are they already too far back in the pack? Here’s the latest news on the mobile + payments + commerce front. Miami Transportation To Offer Mobile Payments. Miami Transportation To Offer Mobile Payments.

Some banks may not be able to connect to both. The panel will explore some of these initiatives including the New York Fed's CBDC pilot program with major banks, the recently concluded Boston Fed's Project Hamilton and other global CBDC projects. FedNow may not interoperate with RTP, and it doesn't seem to be a priority for either.

Consumers don’t think about technology as technology; it just is,” said mastercard Chief Innovation Officer Garry Lyons at the unveiling of mastercard’s new digital payments strategy yesterday (July 14). It is a smart digital credential — the same smart digital credential, in fact, that goes where the consumer goes.”.

Like the giant puzzle pieces that keep the Earth’s surface in equilibrium, the ecosystems that represent how consumers pay, how they bank, how they borrow, how they shop and how they decide when, where and what to buy used to be easily defined and neatly connected. The Unbundling Of The Bank. The Commoditization Of Retail.

PayPal announced new collaborations with both Citi and FIS, while Mastercard and Visa shared a mutual commitment to accelerate digital wallet adoption. Both will enable an easy provisioning of PayPal cards via the bank’smobile app, and both will enable a co-branded experience for the banks.

In the rapidly evolving world of online gaming, having a reliable and secure payment gateway is crucial for both gamers and gaming businesses. Understanding the Basics of Gaming Payment Gateways A gaming payment gateway is a technology that facilitates online transactions between players and gaming platforms.

Because more credit card-oriented purchases take place online, security and fraud protection are top priorities. Businesses are converting to digital and online platforms to stabilize their profitability at this time. Compliance with PCI DSS is mandatory for businesses that handle credit card transactions.

Like the giant puzzle pieces that keep the Earth’s surface in equilibrium, the ecosystems that represent how consumers pay, how they bank, how they borrow, how they shop and how they decide when, where and what to buy used to be easily defined and neatly connected. The Unbundling Of The Bank. The Commoditization Of Retail.

After launching the Masterpass mobile payment app for retail stores last week, payment giant Mastercard announced today it has agreed to purchase a majority stake of U.K.-based In the all-cash deal Mastercard will pay $920 million for a 92.4% In the all-cash deal Mastercard will pay $920 million for a 92.4%

Speaking at FinovateFall 2016 in September, Daon President of the Americas Conor White asked attendees about their own experience with cart abandonment online. Daon’s technology can be deployed to provide authentication for digital banking, for payment verification, and employee credentialing, as well as cloud authentication.

In a recent digital discussion with Karen Webster, Michael Sass, VP Market Product Management, Security Solutions, Europe, Mastercard , and James Rendell, VP Product Management, Payment Security, CA Technologies , discussed the advantages as well as the obstacles that are still in the way. The updated 3D Secure 2.0 The arrival of 3D Secure 2.0

December: Introduces bank account deposits using POLi online payment service. ebankIT : demoed its omnichannel and social banking solution that maximizes interaction between FIs and their clients. May: Begins powering mobile app for Millennium Bank in Poland. September: Launches in Mandarin.

Visa and MasterCard could totally nail it. Creating certainty for the consumer when using mobile payments. The certainty that comes with creating a thick market of merchants and consumers and accounts that work across any mobile device that they happen to own, and can use at the places they routinely shop.

Smart, according to Google, because it will provide its checking accountholders with money management tips to optimize and manage the funds in those accounts – funds linked to payments and identity credentials that consumers can use to buy things, pay bills and send money to others in and outside the Google ecosystem.

Armed with new tech, mobile devices, data and the cloud, they fast-tracked the shift from a largely analog world to the app-based economy of today. billion of whom have a mobile phone. In developed markets, 4G will move to 5G with 15 percent of mobile phones connected, and to 5G five years from now. Today, there are 7.3

Armed with new tech, mobile devices, data and the cloud, they fast-tracked the shift from a largely analog world to the app-based economy of today. billion of whom have a mobile phone. In developed markets, 4G will move to 5G with 15 percent of mobile phones connected, and to 5G five years from now. Today, there are 7.3

The mobile device is the chief conduit toward staging transactions, to getting goods delivered curbside or to the house. Fast-forward to 2020, and the pandemic has shown, through the Stripes and Shopifys of the world — that the pivot to buy online/pickup/deliver has been facilitated by the innovations on the merchant side. "I

Mastercard today announced the launch of its Agentic Payments Program, Mastercard Agent Pay. Mastercard Agent Pay will deliver smarter, more secure, and more personal payments experiences to consumers, merchants, and issuers. The groundbreaking solution integrates with agentic AI to revolutionize commerce.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content