This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dubai First , the consumer services platform under First Abu Dhabi Bank (FAB), has become the first issuer in the region to leverage Mastercard Token Connect to push customers’ tokenized card details from its mobile app to Click to Pay and digital wallets.

As PYMNTS found in a recent consumer study, 40 percent of individuals are doing more of their daily retail and transactions online, partly because, well, there’s no other way to do it. Merchants, he said, “need to make sure they not only accept credit cards but also contactless payments.”. As Good noted, four in 10 U.S.

This shift is especially visible in the adoption of network tokenisationa model introduced by major card networks like Visa and Mastercard, where card details are replaced with dynamic, network-managed tokens. The necessity of tokenisation in digital payments The traditional view of tokenisation as a fraud mitigation tool is outdated.

Community banks and credit unions are feeling the pressure to boost their digital card services or risk losing customers to megabanks and digital challengers, Ondot Systems ’ Chief Strategy Officer Todd Lesher told PYMNTS in a recent discussion. FinTech players are also grabbing deposits. Square announced $1.3

It’s a tale of a cultural shift, governments and innovators working in tandem, and millions leapfrogging traditional banking to embrace a mobile-first approach to finance. The region’s historical challenges with traditional banking access have paradoxically catalyzed innovation.

That left FIs scrambling to “rapidly figure out how to get that same emotional and engagement outcome when the possibility of face-to-face is virtually nonexistent,” Randy Piatt , head of product solutions at card technology firm Ondot Systems , told PYMNTS in a recent conversation. Simple: Start with the cards.

Community Your feed Latest expert opinions Groups Join the Community 23,315 Expert opinions 42,505 Total members 368 New members (last 30 days) 195 New opinions (last 30 days) 29,090 Total comments Join Sign in Open Banking Won’t Work Without Trust. Here’s How We Enable That. Here’s How We Enable That. Here’s How We Enable That.

The great digital shift is transforming credit cards into money management tools. Consumers want cards, and they want them quickly, and they want those cards [delivered] in a digital way," said Turner. The company said that through the expansion of its Digital-First Card Program, which was announced last Wednesday (Sept.

But in the digital age of commerce wrought by the pandemic, they’re becoming a key point of friction between consumers, merchants and issuers. And then, after the transaction is made, there’s the task of understanding the byzantine codes and data that are tied to online statements. from an issuer side on costs or chargebacks and fraud?’

As businesses and consumers become more comfortable using credit cardsonline, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Stripe really did come about because we were really appalled by how hard it was to charge for things online.” — John Collison.

Indigenous Banking (Shroffs and Mahajans): Long before modern banks, India had a thriving indigenous banking system. These banks introduced formal ledger-based accounting and cheque payments. This expanded the reach of formal banking to rural areas. This introduced standardization and divisibility.

ICBA Bancard, the payments services subsidiary of the Independent Community Bankers of America (ICBA), announced a new partnership with MK Decision (MK) for its online loan-origination system. Our mission — to stimulate local borrowing and local lending — is well aligned with ICBA Bancard and its community bank clients.

The commerce life of a consumer is becoming more digital by the day, given the proliferation of mobile wallets, eCommerce destinations and the emerging plethora of IoT-ready devices now capable of enabling commerce for them. They include: Who they pay. Where they pay. How they can pay. Solutions exist currently, of course.

Mobile will likely get lot of quiet thanks during the next few day — and the holiday season in general, if for no other reason than it helps the season of peace remain, well, peaceful. Customers already have a payment form they likes — plastic cards — and they’ve spent a shopping lifetime developing habits around those cads.

With the recent launch of the Apple Card , Apple has sent a signal that they seek to offer a better user experience than banks. In fact, their slogan for the card is “Created by Apple, Not a Bank?.” And the card is no longer just a payment instrument; it’s more than the card itself.”.

Visa , the credit cardissuer, announced Thursday (May 4) that it will help its financial institution partners create customized digital card management services for their customers. These capabilities will be available for issuing partners to provide to their cardholders through their online and mobilebanking channels.

With ambitious goals to open up banking and decimate fraud, PSD2 has taken a long time to deliver, and we’re not quite there yet. Rather it is the issuer, known as the Account Servicing Payment Service Provider (ASPSP), that must administer it. Banks and their customers, it seems, are on the same page about this.

In a mutual commitment to accelerating the adoption of an open digital wallet, global card networks Mastercard and Visa announce their agreement to allow each network to request tokenized credentials from the other when consumers are transacting across any digital medium — in app, online and in store. Tokens Get Turbocharged.

Fondeadora , the financial service provider in Mexico, has reaffirmed its commitment to delivering secure digital payment services in the region as it partners with MeaWallet , the digital payments enabler specialising in card tokenisation. Push provisioning streamlines the card issuance process to digital wallets.

The COVID-19 pandemic has accelerated the need for FIs to quickly scale and roll out faster payment experiences , whether that means offering businesses instant access to loans or enabling access to consumers’ stimulus funds without any wait, says Bryce Elliott , CIO at Truist Bank. It’s the end of another week and the end of a busy month.

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. In aggregate, these product development and investment decisions reveal that Amazon isn’t building a traditional bank that serves everyone.

Long before American Express was a credit cardissuer and a closed loop payments network, it was in the business of moving mail (and other things) quickly from one coast to the other. And it’s that push toward forward evolution that leads to this week’s big news — American Express has acquired InAuth, Inc.

Linking buyers and sellers across online platforms? Card-not-present (CNP) transactions are increasingly eyed by fraudsters. Consumer Bank, told Karen Webster that the two firms are working together to deliver a consistent and streamlined experience at checkout through Click to Pay. Citi now becomes the first issuer in the U.S.

There’s more to consumer life than purchase history — and more to card acquisition, too. Consumers want engagement and experiences, and issuers that can provide that can not only gain new customers, but keep tighter and more profitable holds on their cardholders. That is not going to change overnight. Cigar Experience.

These solutions span the gamut of B2B payments ’ needs — virtual cards, accounts payable automation and data analytics, to name but a few. That, he said, is done by creating an ecosystem of technology providers whose solutions are vetted by Visa and can be made available through Visa’s 14,000 issuers to the businesses that want and need them.

With ambitious goals to open up banking and decimate fraud, PSD2 has taken a long time to deliver, and we’re not quite there yet. Rather it is the issuer, known as the Account Servicing Payment Service Provider (ASPSP), that must administer it. Banks and their customers, it seems, are on the same page about this.

Yesterday, PYMNTS detailed what happened during Day 1 of Mobile World Congress in Barcelona. And then there was Facebook’s Telecom Infra Project and its virtual reality push. PayPal also broke news with a series of third-party partnerships announcements aimed at growing its global mobile money footprint.

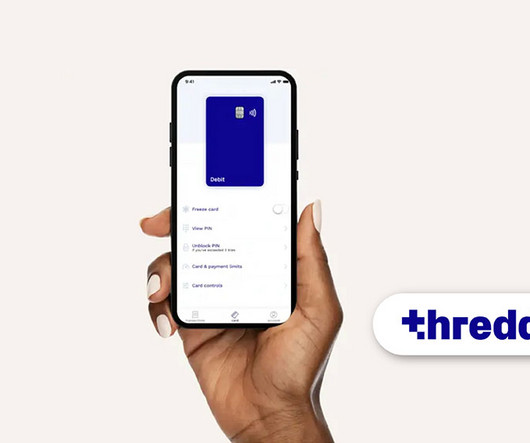

It’s also the inspiration for Ondot’s work with banks to build a better bank-branded app that gives customers access to a wider array of card controls and a real-time stream of actionable data. That, according to VB, depends very much on the use cases issuers want to build into the app. “We

Today at the annual Visa Payments Forum for Central and Eastern Europe, Middle East and Africa, Visa unveiled a suite of new products and services that will revolutionize the card and address the future needs of consumers, merchants and the financial institutions that serve them across the region.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

Increasingly, fraudsters are striking at the very beginning of customers’ relationships with banks and credit unions (CUs), focusing their efforts on account takeovers and new account fraud. In the battle against fraudsters, financial institutions (FIs) must start at the beginning – literally. There are new data privacy concerns, too.”.

11), that public pilot officially came to an end, as Penn Station was added to the New York list of MTA stations that enables open payments using network-branded contactless cards. Penn Station is going online, and [the MTA] will enable another 50 stations this month. Yesterday (Dec. The MTA’s Greater-Than-Expected Success .

Since the first plastic credit card was issued by American Express in 1959 , payment tech progress has been growing exponentially. EMV chip card technology had a good two decades or so, beginning in the mid-’90s. Most modern card readers and payment terminals are NFC-equipped.

But despite the COVID pandemic having effected massive changes in the ways consumers transact, credit card fraud is still a “thing,” and a big, ever-changing thing at that. Exactly how big credit card fraud is depends on where you look. Credit card fraud was the FTC’s second most-reported fraud type in 2019.

Citi has just provided its members an in-app window into the status of their replacement cards. 29), Citi credit card members in the U.S. will be able to track the progress of their replacement card delivery in real time. Customers will also be able to activate their card through the tracker. Starting today (Nov.

The deadline is looming for merchants and payments providers to comply with new requirements for authenticating online payments in Europe. Firms must soon put more stringent fraud decisioning processes in place, and strong customer authentication (SCA) protocols must be built into checkout flows for online transactions that begin in Europe.

Now, however, new details have surfaced as to why China’s banks were finally ready to jump on the Apple Pay bandwagon. According to a report in the Chinese news site Caixin , Apple cut a deal with Chinese banks to charge them less fees than what it charges banks in the U.S. banks fork over to Apple per transaction.

As a corollary to this speed, we have vested outsized amounts of trust in most or all of the companies we do business with online. As a corollary to this speed, we have vested outsized amounts of trust in most or all of the companies we do business with online. How Fraud Could Happen to You. The Scams You Don’t Hear About.

Online retailers are unsure which version of 3D Secure (3DS) they are supposed to use or how to authenticate consumers who do not have mobile phones, given that 2FA is now a requirement. Robinson stated that large merchants focused on SCA’s exceptions when the European Banking Authority (EBA) first outlined the rule.

For those charged with managing the consumer’s trust and safety when transacting online, and in the midst of increasingly clever cybercrooks, being comfortable going against the status quo flow has become much more important than ever before, he said. I joked that I’d be a shoo-in for the job. Amazon Takes Its Bite Out of the Big Apple.

Banks $88 Billion Bad Debt Concern . The delinquent credit rate is ticking up, and banks are reacting by dialing back new account approvals. Credit card debt made it over the $1 trillion mark in 2017, making it the third non-mortgage lending category to have surpassed the ten-digit mark in measuring consumer debt. In fact, at 3.4

This week in PYMNTS and commerce, we had plenty of players pushing in the spirit of said ancient wisdom, to greater and lesser effect. Amazon is also offering discounts to merchants who use its online payments service. According to Bloomberg, online merchants using Amazon’s service have paid about 2.9 Visa fell 0.9

For the most part, Venmo is well regarded by consumers and merchants alike, earning a reputation as one of the leading mobile payment services around. Essentially, before processing the payment, Venmo verifies that the account holder’s balance or linked bank account has enough funds to cover the transaction.

“It will push everyone to think differently about the value that electronic payments needs to deliver to all stakeholders, including Visa.” “Competition is better for everyone.” – Visa CEO Charlie Scharf. A statement that sounds like exactly what you’d expect to hear from the leader of the largest payments network in the world.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content